Family Holdings #10 - From toxic pills in software to the AI attack on your brain

This week's topics:

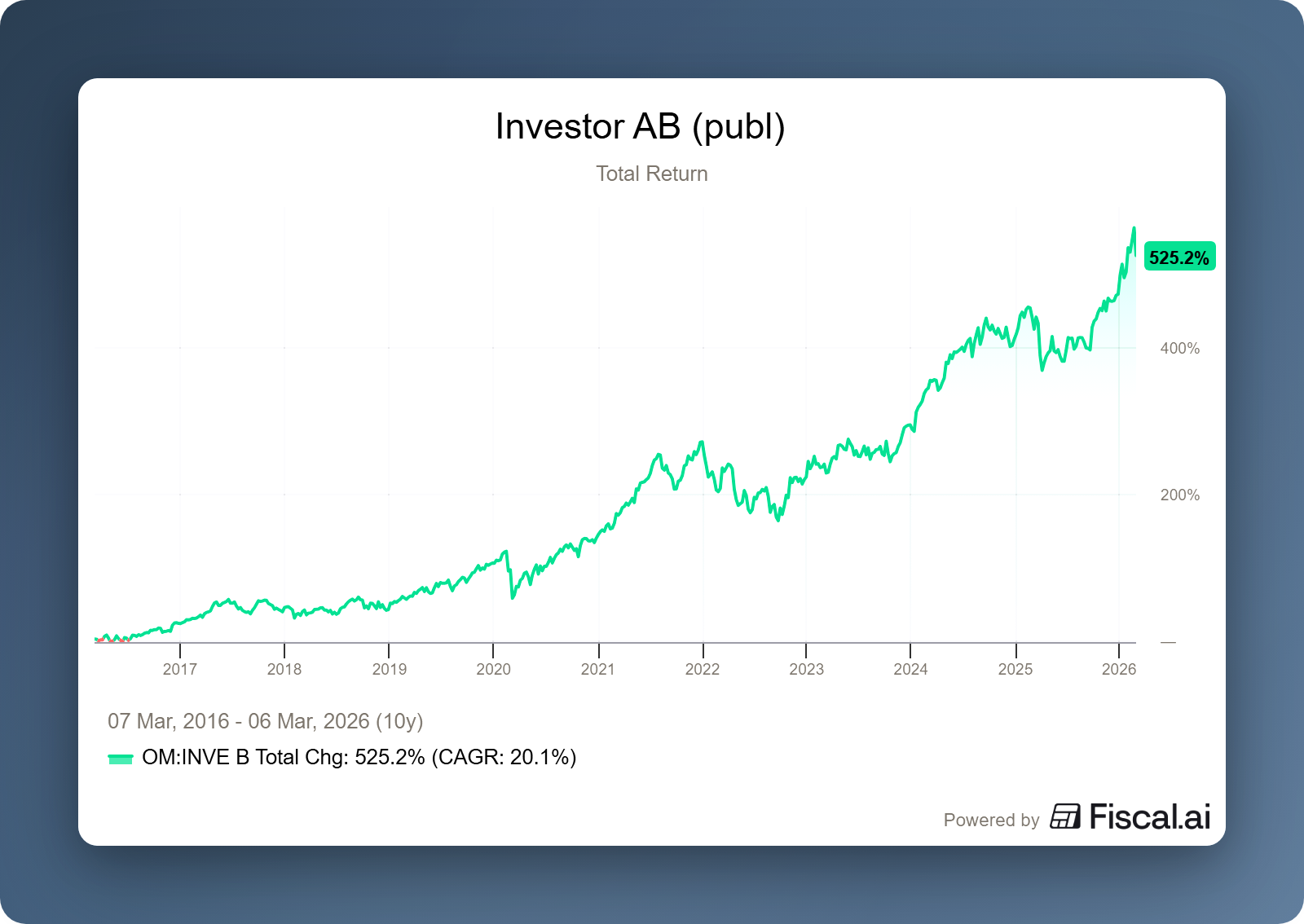

Investor AB has invested more than SEK 1 billion extra in private equity firm EQT in a short period of time, while EQT is simultaneously buying back SEK 842 million of its own shares. This double purchase underscores confidence in the company, especially now that EQT, together with BlackRock, has announced a billion-dollar acquisition of AES Corp. With this move, EQT is positioning itself directly in the energy infrastructure that is crucial for the power supply of AI data centers.

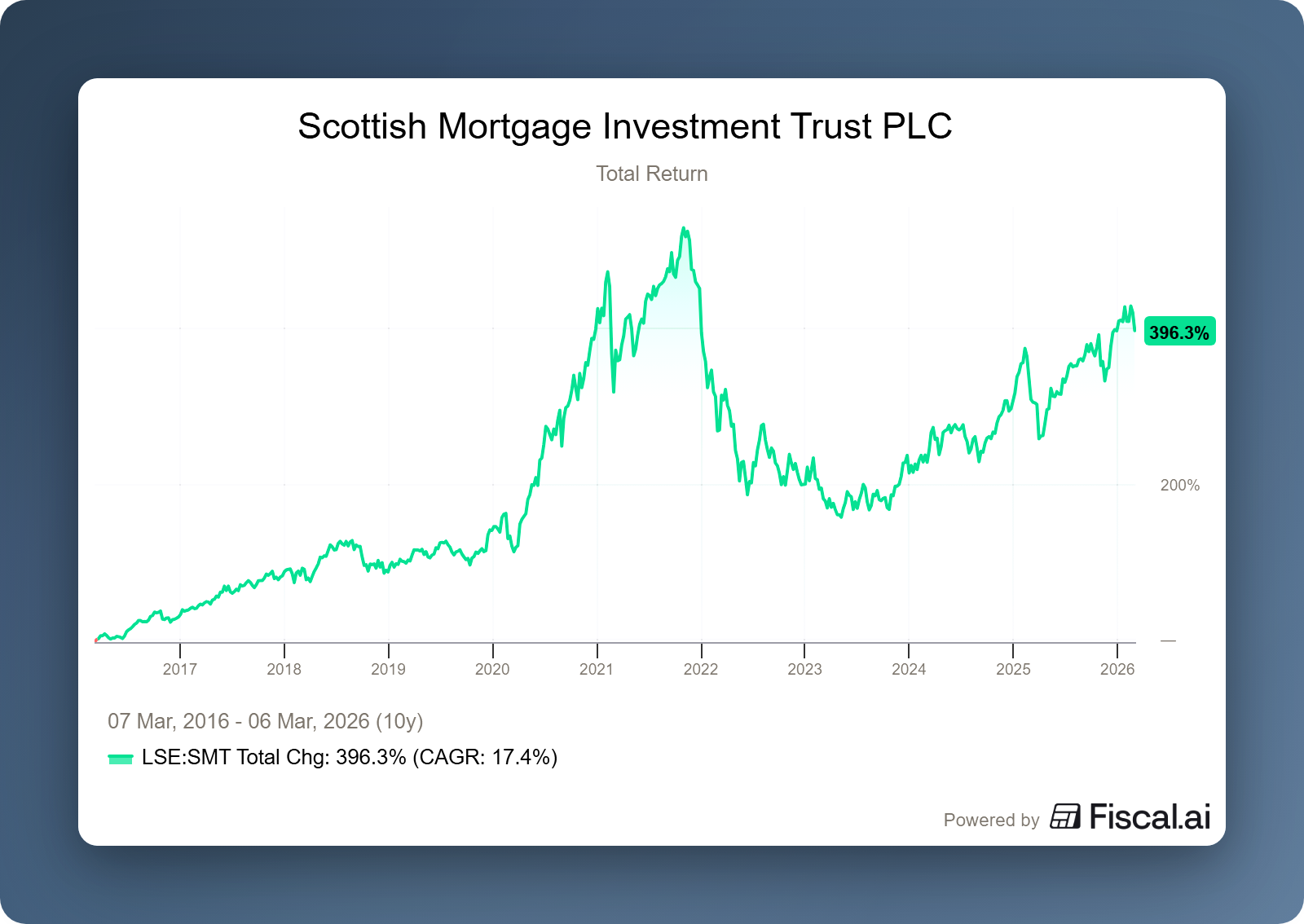

Manager Tom Slater of Scottish Mortgage Investment Trust warns that the impact of AI goes beyond economic gain; it is physically rewiring our brains and our ability to learn. While AI dramatically increases efficiency at portfolio companies such as NVIDIA and Shopify in the short term, there is a risk that "productive friction" will disappear. The Trust argues that in our drive for AI-driven optimization, we must be careful not to lose the human skills that are crucial when technology fails.

Prosus is caught in a geopolitical tug-of-war as the US White House investigates the gaming interests of crown jewel Tencent for security risks. Although a forced sale of Western gaming assets would affect Tencent's international growth, it would also free up a huge cash mountain. Meanwhile, Prosus is focusing on local growth with a new multi-million investment in flash delivery service Flink, which is now profitable in the Netherlands and Germany and is benefiting from the still low online penetration of the grocery market.

In Brief:

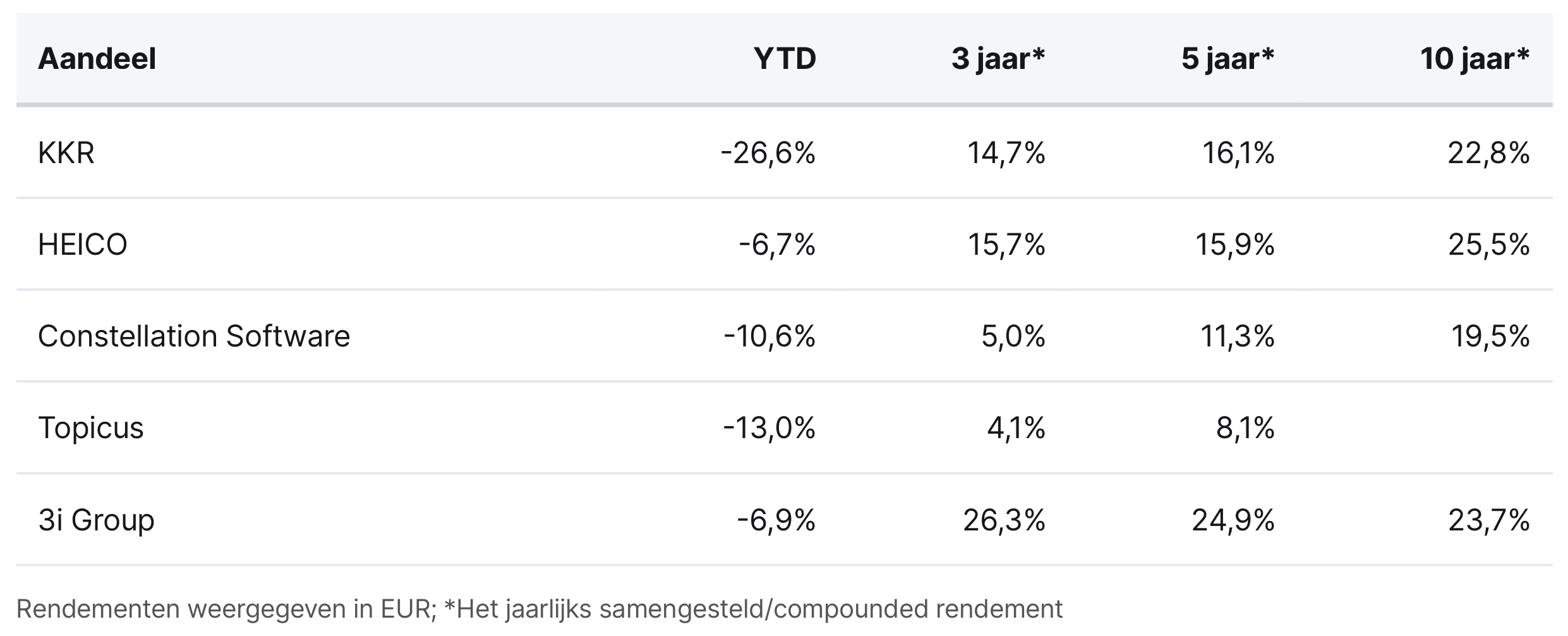

The conviction among KKR ( New York: KKR) executives that the stock is currently significantly undervalued was confirmed once again this week. The most recent transactions show that the co-CEOs and supervisory directors have again allocated millions of their own capital. Co-CEOs Joseph Bae and Scott Nuttall and several supervisory directors purchased more than 60,000 shares on the open market this week. This brings the total amount that insiders have invested in the stock out of their own pockets in recent months to more than $45 million.

HEICO ( New York: HEI.A) saw a significant show of confidence from within its own ranks this week. Nandakumar Cheruvatath, a director at a subsidiary of the company, purchased 4,082 shares on March 4 for approximately $1 million. This significantly expands the director's modest position of 64 shares to a total of 4,146 shares.

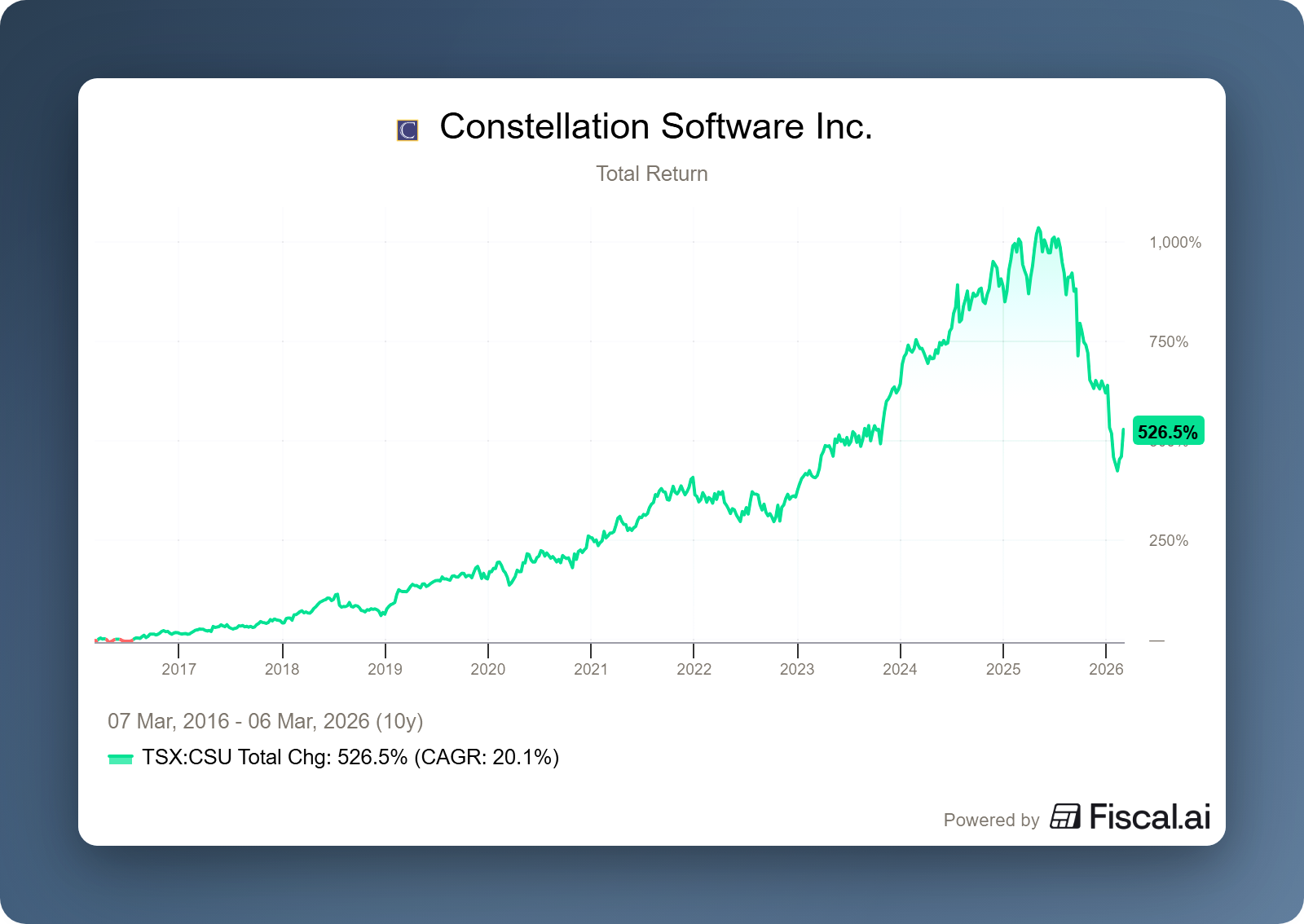

Constellation Software (Toronto: CSU) is further expanding its presence in Latin America through its subsidiary Vesta. The company has acquired Argentina-based Nodum Argentina. This acquisition follows the earlier acquisition of the Uruguayan branch in 2023. Nodum has been providing ERP and CRM solutions to hundreds of customers in the region since the 1990s. The new acquisition will merge with the Uruguayan operations to form the joint entity Nodum Global.

Topicus ( Toronto: TOI) had a particularly active week with three strategic acquisitions through its operating company Total Specific Solutions. The group acquired Dutch company Desyde, which plays a leading role in the management of parking permits for municipalities with its SaaS solution. Topicus also strengthened its position in the French aviation sector with the acquisition of Cyberjet, a specialist in flight operations and crew management systems. Finally, the education division was expanded with the addition of Rotterdam-based PortalPlus to further optimize student support, from intake to alumni management.

Finally, 3i Group (London: III) announced a successful divestment through its listed entity 3i Infrastructure. The division sold its 71% stake in Belgian airport equipment specialist TCR for €1.14 billion. This sale, which was 22% above the most recent valuation in September 2025, enables the investment company to free up capital to repay loans and finance new investments after a successful growth period of almost ten years within the TCR platform.

KKR, HEICO, Constellation Software, Topicus, and 3i Group are currently trading on the New York, Toronto, and London stock exchanges at prices of USD 91.53, USD 232.18, CAD 2902.02, CAD 108.84, and GBP 30.14 per share, respectively.

Constellation Software and Sabre's "Poison Pill"

Last week, Canadian software giant Constellation Software (Toronto: CSU) and US-listed travel technology provider Sabre Corp (New York: SABR) reached a strategic agreement after a hectic negotiation process.

During 2025, Constellation quietly built up a 9.7% economic interest in Sabre. In January 2026, the Canadian takeover machine disclosed this interest to Sabre's management, proposing a long-term partnership. Constellation's approach was to acquire a controlling interest and board seats, a model they had previously used successfully with listed companies such as Topicus and Asseco.

However, Sabre's management was not immediately open to such a controlling interest and responded defensively to the approach. To guarantee independence and block any unwanted expansion of Constellation's stake, the board activated a so-called 'poison pill' (Shareholder Rights Plan). This measure was intended to make further share purchases above 15% virtually impossible without the consent of the board.

What happened?

Although Constellation's intentions initially appeared constructive, a notable friction arose in February. According to statements by Sabre, negotiations over board seats stalled after Constellation suddenly broke off talks with the cryptic message that their plans "would become clear in time." This caused unrest among Sabre's board, who feared that Constellation would build up a controlling interest through the open market without paying the usual takeover premium.

In direct response to this, Sabre activated a Shareholder Rights Plan, better known as a 'poison pill'. This mechanism comes into effect as soon as a party owns more than 15% of the shares. At that point, all other shareholders are given the right to purchase additional shares at a substantial discount. For the "raider" (in this case Constellation), this would mean an immediate and enormous dilution of its interest, effectively making a hostile takeover impossible and forcing Constellation to return to the negotiating table.

On March 5, the final breakthrough came: Sabre and Constellation Software announced a strategic partnership in which Constellation will acquire a 12.7% stake in the company and a seat on the board of directors. Damian McKay, the current CEO of the Vela division (which includes Juniper, the central travel platform within the Constellation ecosystem), will join Sabre's board of directors on behalf of the group. Given his extensive experience in the sector, this seems a logical choice.

Investors see the group's involvement as providing the much-needed operational discipline that Sabre needs to get its balance sheet in order. Sabre's share price shot up 50% in just one week to a peak of $1.99. Although the share price has since lost some of these gains, the sharp movement illustrates the market's confidence in the company's ability to recover under the wing of the experienced software investor.

What does Sabre do and why is it financially attractive?

As one of the three dominant players in Global Distribution Systems (GDS), Sabre Corporation forms the indispensable backbone of the global travel industry. The platform facilitates the complex link between providers such as airlines and hotels on the one hand, and customers such as travel agencies and booking sites on the other.

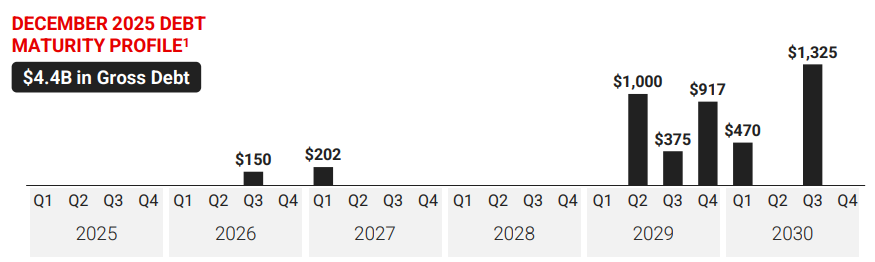

A quick glance at the figures quickly reveals that this is a special case. With a market capitalization of approximately $640 million and adjusted operating profit before interest, taxes, depreciation, and amortization (EBITDA) of $500 million, the company appears to be very attractively valued at first glance. However, there is a catch. The underlying enterprise value (calculated as: market capitalization + net debt — cash) is approximately $4.4 billion, which immediately reveals the crux of the matter: a substantial debt position that makes the picture considerably more complex than it appears at first glance.

At the end of 2025, gross debt amounted to $4.3 billion. Adjusted for cash reserves, net debt remained at $3.74 billion. Compared to adjusted operating profit of $500 million, this results in a net debt ratio of approximately 7.5x, which is significant leverage for a company operating in a sector where AI and direct distribution are challenging the traditional GDS position. In a climate of higher interest rates and uncertainty about these developments, this has pushed Sabre's share price down by more than 50% over the past year.

It is precisely this tight balance that forms the core of the investment case that many investors are currently putting forward regarding Constellation Software's involvement. Net interest expense amounted to $447.8 million in 2025. This means that almost 90% of operating cash flow is immediately swallowed up by creditors. The result of this top-heavy capital structure is that the bottom line is completely underwater; after deducting interest, taxes, and depreciation, a net loss of $255 million remained for 2025.

Nevertheless, the maturity structure of the debt provides some breathing space. More than 90% of the outstanding debt does not need to be repaid until 2029 or later. This gives the management team ample scope to optimize cash flows and gradually reduce the debt position. Any percentage improvement in the operating margin or reduction in financing costs will immediately lead to a disproportionate strengthening of net profit due to the enormous leverage effect.

In addition to the debt management case, there is a second, more long-term optionality in potential margin improvements. Constellation Software has repeatedly communicated in the past that it can lift software companies to adjusted EBITDA margins of around 30% through its proven operational blueprint. Sabre's current Adjusted EBITDA margin is 18.1%. That is not a bad starting point, but it does imply that there is theoretically another twelve percentage points of margin on the table. It is important to note that this is definitely a long way off. Constellation currently has one board seat and no operational control. Whether, and at what pace, their blueprint will actually be implemented cannot be quantified at this time. But as a second order after the primary debt reduction, it is an interesting additional option in the investment case.

conclusion For Constellation, this position acts as an option structure. With a stake of $65-85 million, they are buying asymmetric exposure: as a minority shareholder, they bear no financial responsibility for the $4.3 billion debt, but through Damian McKay's board position, they do have direct influence on capital allocation. The downside is that this option could also expire at zero, not only if debt reduction stagnates, but also if Sabre fails to move in time with AI and new direct distribution models before competitive pressure becomes unsustainable.

Constellation Software is currently trading on the Toronto Stock Exchange at a price of CAD 2,902.02 per share.

Receive weekly insights in your inbox

Exclusive analyses and updates on family holdings and global market developments.

Double purchase of EQT shares

The Swedish family holding company Investor AB (Stockholm: INVE-B) is not wasting any time when it comes to its stake in private equity firm EQT AB (Stockholm: EQT). Following a previous substantial purchase of 2.26 million shares in February (worth SEK 657 million), the holding company struck again between February 27 and March 2. According to data from the Swedish regulator, Investor purchased another 1.14 million shares for more than SEK 318 million. This brings the total amount that Investor has invested in private equity firm EQT in just a few weeks to over SEK 1 billion, or EUR 93 million.

While Investor AB is increasing its stake on the stock exchange, EQT has also launched a buyback program of more than 3 million of its own shares (approximately SEK 842 million) to optimize its capital structure.

This buying frenzy coincides with a strategic partnership by EQT. Together with BlackRock (Global Infrastructure Partners), EQT has reached an agreement to acquire the US-listed energy company AES Corp. for a total enterprise value of no less than $33.4 billion. The acquisition is a direct bet on the explosive growth of AI data centers, which consume enormous amounts of electricity. AES already supplies sustainable energy to tech giants such as Google, Microsoft, and Amazon, positioning EQT at the heart of the physical infrastructure that enables the AI revolution.

Investor AB is currently trading on the Stockholm Stock Exchange at a price of SEK 356.10 per B share.

AI isn't after your job, but your mind

The British holding company Scottish Mortgage Investment Trust ( London: SMT) has been known for decades for its unshakeable belief in disruptive technology. Director Tom Slater manages billions in companies such as NVIDIA, Amazon, and Tesla. He recently published an in-depth and very interesting analysis: "AI Isn’t Coming For Your Job. It's Coming For Your Mind." In it, the manager shifts the focus from the economic gains of AI to its biological and psychological impact on humans.

The Great Rewiring

Slater argues that AI is not just a tool, but the "next great rewiring" of the human brain. He compares this to the rise of literacy 200 years ago. When we learned to read, our brain structure physically changed; areas for facial recognition were repurposed for letter recognition.

AI is now doing the same thing, but at breakneck speed. The trust warns of three fundamental shifts:

- Variation: AI generates ideas that humans would never come up with (think of new medicines or AlphaGo's unorthodox moves).

- Transmission: We no longer learn from individual people, but from central models (such as ChatGPT) that filter the knowledge of the entire civilization.

- Selection: Algorithms determine what we see. They do not select based on truth or usefulness, but on engagement.

The essence of Scottish Mortgage's warning lies in the so-called paradox of efficiency: although AI dramatically improves performance in the short term, it systematically breaks down the underlying human capabilities that make this performance possible. When 'productive friction' (the laborious effort of working on a text or complex analysis) disappears, so does the deep anchoring in our memory. Users appear to have little memory of their own AI-generated work, simply because the neurological effort required for sustainable learning has been bypassed.

This neurological impoverishment strikes at the very heart of Tom Slater's investment vision. Why is the director of a trust that invests heavily in companies such as NVIDIA and Shopify so concerned about this? Because it affects the long-term sustainability of their portfolio. Companies such as Shopify now require teams to first prove why AI cannot perform a task before hiring new staff. Although this gives the Trust's profit margins a huge boost in the short term, Slater sees a creeping danger for the future: the disappearance of mastery.

Pilots still learn to fly manually before using autopilot. Not because autopilot is inadequate, but because on the day it fails, there must be someone who can land the plane.

For Scottish Mortgage, AI is a powerful tailwind for their portfolio companies, but they caution investors that in our drive for efficiency, we must not throw the captain overboard.

Scottish Mortgage Investment Trust is currently trading on the London Stock Exchange at a price of GBP 11.61 per share.

Receive weekly insights in your inbox

Exclusive analyses and updates on family holdings and global market developments.

Prosus: Tencent under scrutiny and a new investment

This week, it became clear that the most important value driver in Prosus' ( Amsterdam: PRX) portfolio has come under scrutiny due to the geopolitical chess game between Trump and China.

The White House is currently investigating whether Tencent's interests in major American and European gaming companies, such as Riot Games (League of Legends), Epic Games (Fortnite), and Finland's Supercell (Clash of Clans), pose a national security risk.

With a meeting between Trump and Xi Jinping looming in April, the question hanging over the market is whether Tencent will be forced to divest. Gaming accounts for about 30% of Tencent's total revenue. Although two-thirds of that gaming revenue still comes from China, these three international heavyweights are crucial to growth outside the saturated home market. A forced spin-off would mean Tencent would have to sell its most lucrative Western assets. It would significantly weaken Tencent's international arm, but at the same time free up a huge cash pile.

Closer to home, however, there is other news from our own portfolio. This week, Prosus led a new $100 million financing round for flash delivery service Flink. For most Dutch people, Flink is a familiar sight on the streets, as the delivery drivers with their striking pink backpacks have become an integral part of our city centers.

After a turbulent period of consolidation in the quick commerce market, Flink has announced that it is now profitable at EBITDA level in the Netherlands and Germany. With online grocery penetration in the Netherlands at only 6% (compared to 14% in the UK), Prosus still sees enormous growth opportunities and is further expanding its food delivery portfolio following the earlier acquisition of Just Eat Takeaway in 2025.

Prosus is currently trading on the Amsterdam stock exchange at a price of EUR 41.98 per share.

Receive weekly insights in your inbox

Exclusive analyses and updates on family holdings and global market developments.

Would you like more information about our services?

Contact usDisclaimer:

No rights can be derived from this publication. This is a publication by Tresor Capital. Reproduction of this document, or parts thereof, by third parties is only permitted with written permission and with reference to the source, Tresor Capital.

This publication has been compiled with the utmost care by Tresor Capital. The information is intended in a general sense and is not tailored to your individual situation. The information should therefore expressly not be regarded as advice, an offer or a proposal to purchase or trade investment products and/or purchase investment services, nor as investment advice. The authors, Tresor Capital and/or its employees may hold positions in the securities discussed, either for their own account or for their clients.

You should carefully consider the risks before you start investing. The value of your investments may fluctuate. Past performance is no guarantee of future results. You may lose (part of) your investment. Tresor Capital accepts no liability for any inaccuracies or omissions. This information is for indicative purposes only and is subject to change.

Read the full disclaimer at tresorcapitalnieuws.nl/disclaimer .