Family Holdings #12 - The AI hype is free, but the bill isn't

This week's topics:

The managers of the Scottish Mortgage Investment Trust describe the current AI transition as the most impactful shift ever and position the holding as a broadly diversified “insurance” across the entire value chain. A standout success story within the portfolio is SpaceX, which now accounts for 15.4% of the fund due to strong gains. To remain agile in pursuing new “moonshots” despite strict limits on private equity holdings, management is proposing a policy change that creates additional investment capacity. According to managers Slater and Burns, this gives the trust a key advantage over passive index funds: exclusive access to the crucial growth phase of private AI pioneers such as Anthropic, even before they reach the public market.

In Brief:

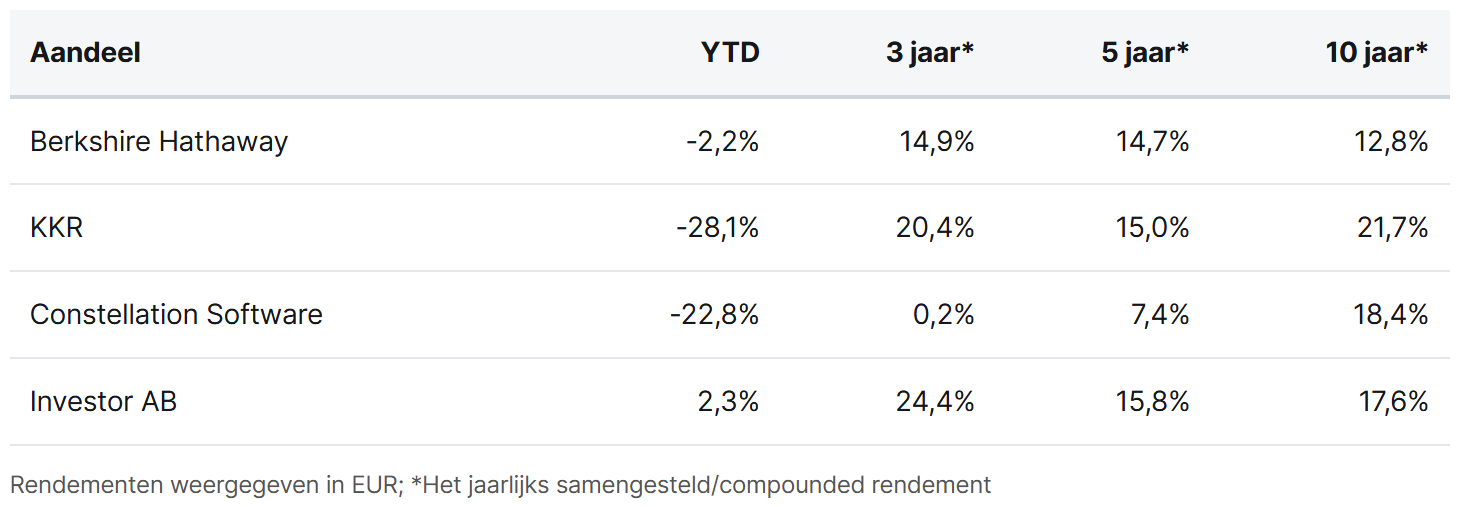

Berkshire Hathaway (New York: BRK.B) has gotten off to a flying start with its recently announced share buyback program. Immediately following the official announcement, the holding company opened its wallet to purchase the first shares. A recent filing shows that in the first few days, the company spent roughly $226 million to buy back “only” 309 Class A shares.

KKR ( New York: KKR) is poised to realize a significant profit from the sale of the cooling technology company CoolIT. The firm acquired a majority stake in the company in 2023 at a valuation of $270 million. CoolIT is reportedly set to be sold at a valuation of between $4.5 and $5 billion. In addition, the firm is investing up to $310 million in an initial investment for the fund dedicated to the climate transition in India. KKR is acquiring a majority stake in the electric bus platform PMI Electro and Allfleet India, which plans to roll out a fleet of more than 5,000 buses.

Constellation Software (Toronto: CSU) saw three of its platform companies make new acquisitions. For example, its subsidiary Volaris acquired the U.S.-based company Compose, a provider of cloud-based software for policy and procedure management. Furthermore, Vela completed no fewer than three acquisitions in Brazil: Alfasig (tax documentation), Alpino Tecnologia (invoicing), and ERP Praeter (management systems). Jonas was also active; through its subsidiary Vesta, it acquired the Hungarian company SK Trend. This insurance technology company offers a front- and back-office platform for intermediaries and marks Jonas’s fourth acquisition in Hungary.

The management of the Swedish family-owned holding company Investor AB (Stockholm: INVE.B) has once again demonstrated strong confidence in the company’s stock price. Both CEO Christian Cederholm and board member Thomas Kidane increased their holdings this week with purchases of SEK 1 million and SEK 0.7 million, respectively. At subsidiary Atlas Copco, CEO Vagner Rego also sent a clear signal by buying SEK 1.5 million worth of shares.

Berkshire Hathaway, KKR, Constellation Software, and Investor AB are currently trading on the New York, Toronto, and Stockholm stock exchanges at prices of USD 483.57 (Class B shares), USD 89.90, CAD 2,509.57, and SEK 338.00 per share, respectively.

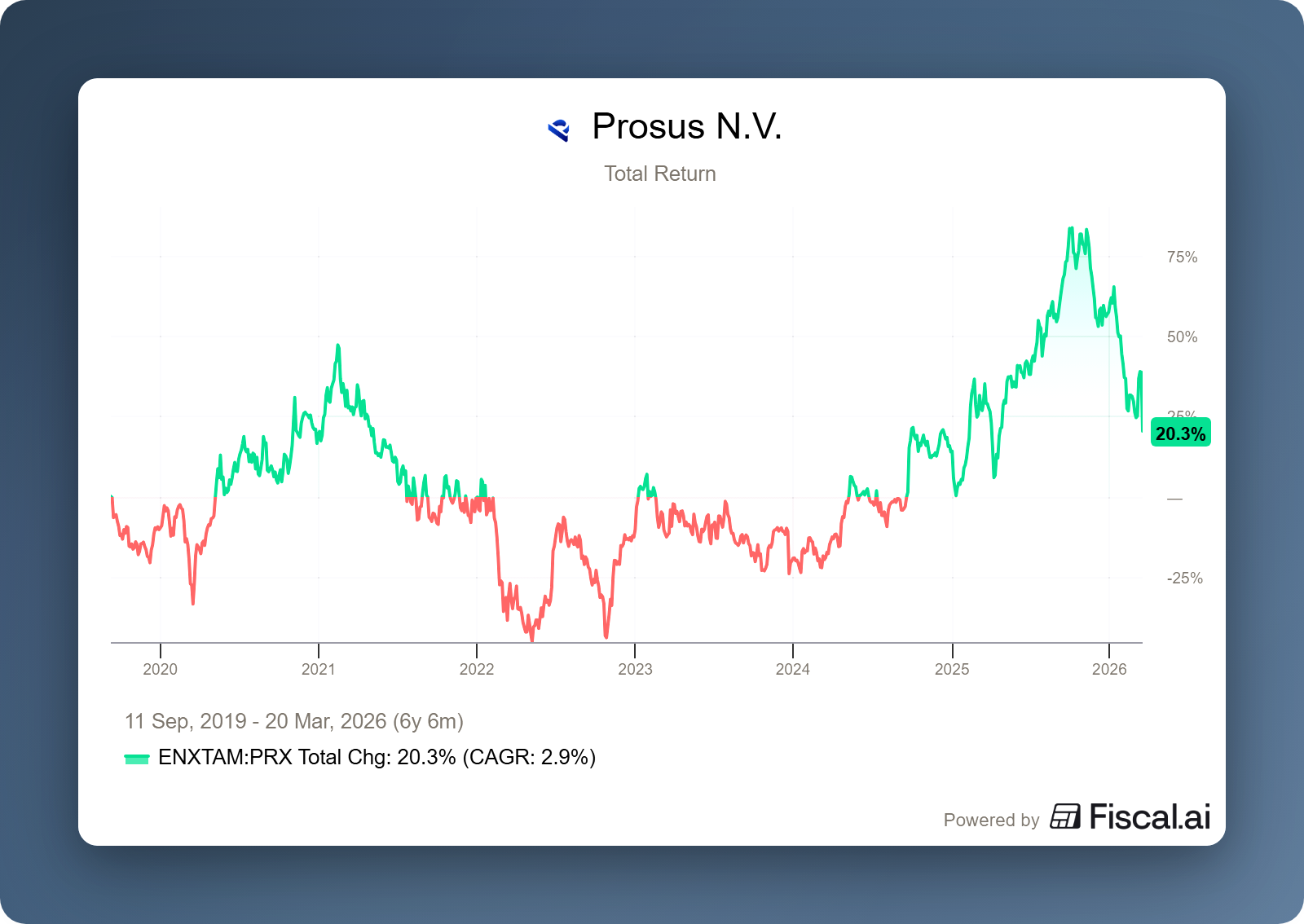

Tencent's AI investment impacts Prosus

For shareholders in the Dutch investment holding company Prosus (Amsterdam: PRX), Tencent’s results are the key indicator of intrinsic value. With a stake representing approximately 80% of Prosus’s intrinsic value, Tencent serves as the primary driver of its return profile. The 2025 figures show a financially robust company that now aims to build on this momentum through increased AI investments.

A quick look at the numbers

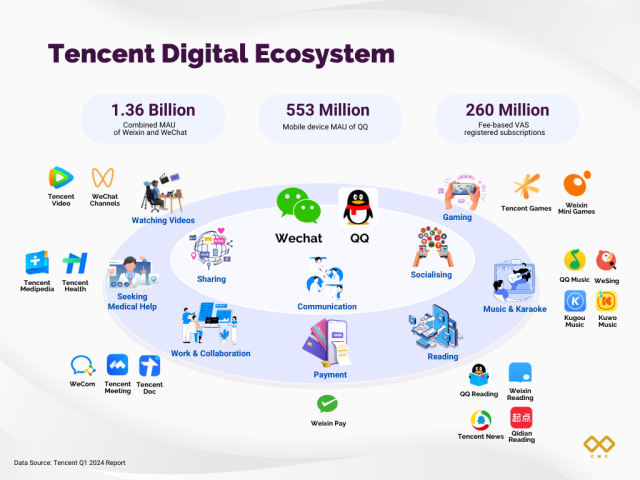

Tencent closed out the 2025 fiscal year with a set of robust results that exceeded market expectations on an operational level. Total annual revenue rose by 14% to RMB 751.8 billion, and gross profit increased by a whopping 21%. The company has thus consistently demonstrated over the past few years that it can grow profits faster than revenue, resulting in structurally rising profit margins.

Rather than simply chasing volume, management has succeeded in more effectively converting users within the WeChat ecosystem (Weixin) into profitable services. The fundamentals underpinning key growth drivers therefore remain as strong as ever:

International expansion: The gaming division outside China has now become a full-fledged growth engine. With annual revenue surpassing the $10 billion mark for the first time, driven by 33% year-over-year growth, the company’s reliance on the Chinese domestic market is decreasing. This fundamentally improves the company’s risk profile.

Advertising efficiency: Thanks to the integration of AI algorithms, Tencent is able to deliver more relevant ads, which directly translates into higher ad rates and a greater willingness among advertisers to shift their budgets to Tencent.

The Cloud Comes of Age: A key milestone this year is that the cloud business was profitable for the first time over a full fiscal year, with an operating profit of approximately $726 million. This proves that years of investment in infrastructure are finally beginning to pay off.

The market likes AI applications, but not AI investments

Despite this strong operational performance, the stock market reacted negatively, resulting in a drop of more than 7% in the share price. The dissatisfaction is not directed at yesterday’s figures, but at management’s decisions regarding future AI investments.

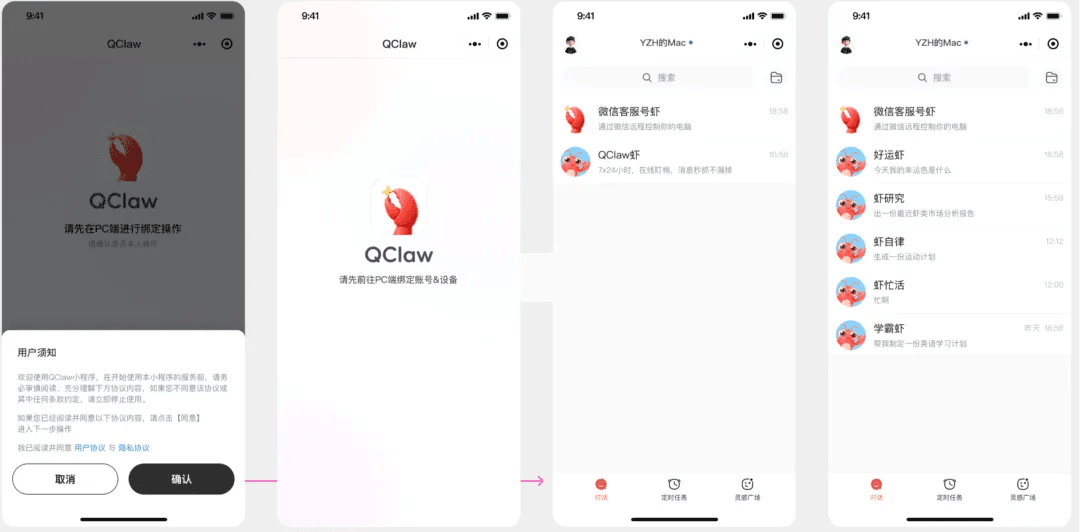

The contrast with the week before the earnings report is striking. Back then, the stock price rose sharply following news of the sponsorship of the OpenClaw community and the launch of QClaw, an AI assistant that has since entered public beta. This "digital version of yourself" is deeply integrated into WeChat and allows users to perform complex tasks on their computers via their smartphones. Now that Tencent has officially announced plans to scale up its AI investments (both OPEX and CAPEX) to record levels by 2026, the market has suddenly reacted negatively. The reason for this is that management has decided to scale back the volume of share buybacks compared to 2025 in order to finance these billion-dollar investments.

The fundamental question is whether Tencent is striking the right balance between capital allocation and innovation at this stage of the AI cycle. On the one hand, there is a belief that Tencent does not have to choose between investing and rewarding shareholders at all. With a ‘triple-A’ balance sheet, a net cash position of $15 billion, and a substantial investment portfolio, its financial firepower is enormous. Precisely because there is currently skepticism about AI spending and the stock price is under pressure, share buybacks seem lucrative at this moment. Tencent could even justify taking on a modest amount of debt to win the AI race while simultaneously capitalizing on the historically low valuation by aggressively buying back its own shares.

On the other hand, the risk of falling behind in the AI race is many times greater than the short-term gains from share buybacks. In the technology sector, the return on share buybacks is ultimately zero if a company loses its growth trajectory to the competition. From that perspective, strengthening the operational foundation is a necessary survival strategy that secures the company’s competitive moats in the long term.

Although the call for a more aggressive share buyback program at these prices is understandable, the strategic rationale behind the current focus on AI integration appears solid. Furthermore, the market impact of the reduced buybacks is partly offset by the fact that Prosus is currently selling fewer Tencent shares to finance its own share buyback program, which somewhat neutralizes the pressure on Tencent’s stock. Now that Tencent is explicitly going on the offensive in 2026, this may cause some volatility in the short term, but at the same time, it strengthens the foundation for Prosus in the coming years.

Prosus closed the trading week on the Amsterdam Stock Exchange at a price of EUR 40.02 per share.

Receive weekly insights in your inbox

Exclusive analyses and updates on family holdings and global market developments.

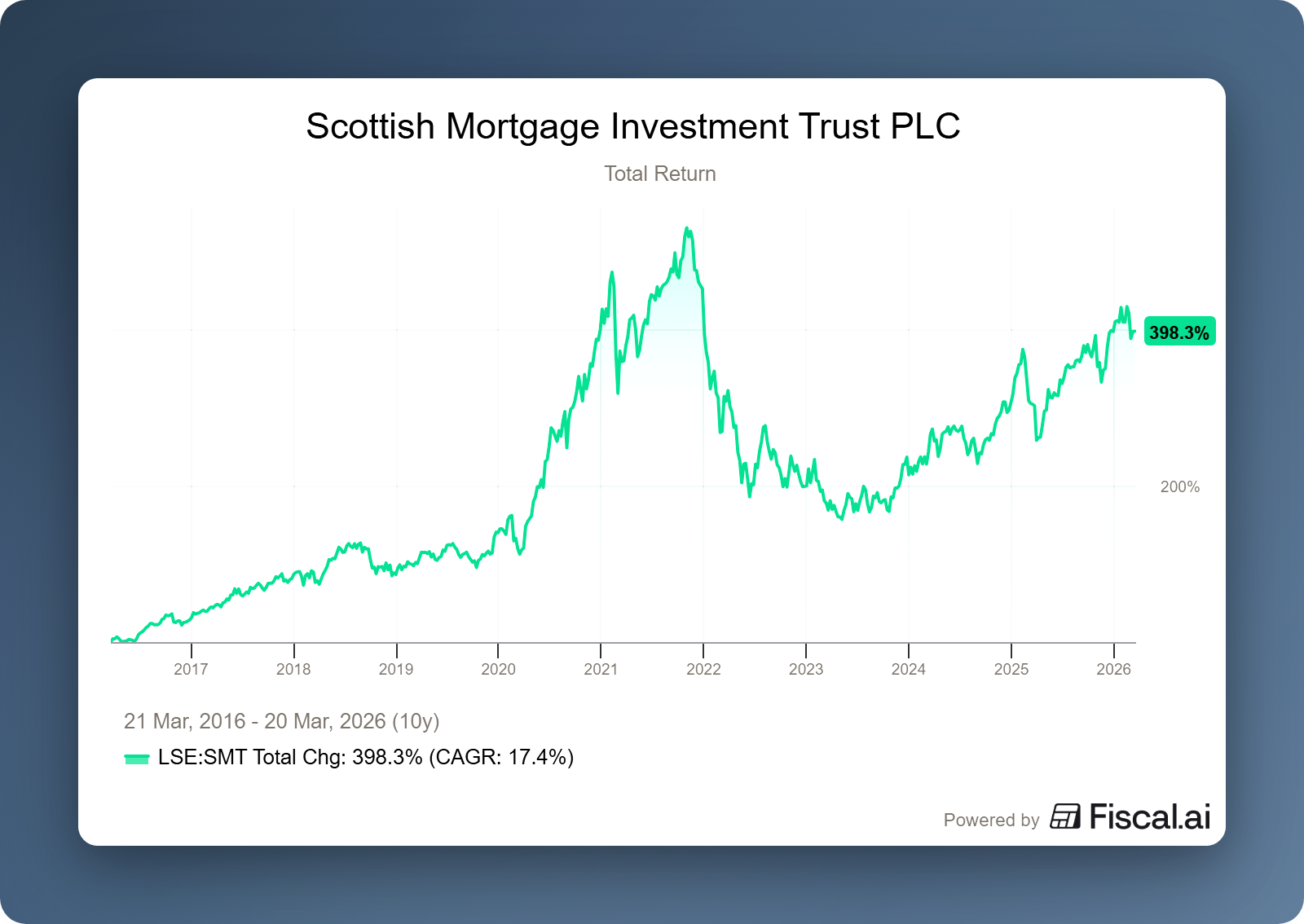

Scottish Mortgage as a safeguard against change

The managers of Scottish Mortgage Investment Trust (London: SMT) describe the current AI transition as the most impactful technological shift the world has ever seen. According to managers Tom Slater and Lawrence Burns, it is crucial for investors not to bet on any one specific component, but to spread their exposure across the entire value chain. In a recent series of updates, they provided insight into how they are positioning the investment holding company as an “insurance against change.”

During an in-depth Q&A session, the fund managers discussed the specific investment decisions within the portfolio, the challenges surrounding private interests, and their vision for the future of tech giants. Want to see the full interview? Watch the full Q&A video here:

A luxury problem with SpaceX

One of the most pressing questions for investors in Scottish Mortgage is how the fund handles its biggest successes. SpaceX has now grown to account for 15.4% of the total portfolio, which presents a luxury problem: the trust maintains a self-imposed limit of 30% for private (unlisted) holdings. Due to the massive increase in SpaceX’s value, exposure to private companies has grown to 37.3%, meaning the holding is formally above its limit.

Since the limit was exceeded due to increases in the value of existing positions rather than additional purchases, this is permitted under the policy, and the fund does not need to sell holdings prematurely. However, this does create the obstacle that the holding company cannot make new private purchases according to its own rules. Management therefore confirmed that it is considering an adjustment to the policy to pave the way for new “moonshots.” To create more flexibility, the board proposed a concrete policy adjustment this week. Although the general 30% limit for the managers remains in place, under the new rules the trust would be allowed to invest up to an additional £250 million in private companies, even if the exposure already exceeds 30%.

With rumors of a SpaceX IPO in 2026, a large portion of the portfolio would automatically shift from “private” to “public.” It seems unlikely that Scottish would sell its entire stake in an IPO; the investment holding company is known for holding onto winners on the public market for years, as long as their growth potential remains intact. In the case of SpaceX, Lawrence Burns sees this growth trajectory only widening, partly due to its close integration with xAI. According to Burns, this integration allows SpaceX to control the entire AI value chain, with space offering the solution to the enormous energy and cooling constraints facing data centers on Earth.

Although this vision of the future forms the basis for the current valuation in the eyes of many investors, it remains to be seen how SpaceX will make the enormous launch costs and the complex technical challenges of maintaining hardware in a vacuum profitable.

Why not invest in AI through an index

A common argument is that investors can also gain exposure to AI (through Nvidia or Microsoft) by investing in a low-cost index fund tracking the Nasdaq or S&P 500. Scottish Mortgage counters this with two key advantages of buying shares in the holding company instead.

First, access to private markets. Through stakes in companies like Anthropic (a direct competitor of OpenAI), the trust provides access to cutting-edge AI models that are out of reach for ordinary investors. Burns on Anthropic: “The recent wave of sales in software names was driven by Anthropic’s latest ‘agent’ product. That gives you an idea of its disruptive power. We simply don’t know yet where the limits of this impact lie.”

Second, diversification across the entire "stack." While trackers often rely heavily on hardware (Nvidia), Scottish also invests in the infrastructure and application layers. The goal is not to track the index, but to own the winners of the future before the rest of the market discovers them.

A third crucial argument is the structural shift in which companies are delaying their initial public offerings for increasingly longer periods. Because private markets have matured and vast amounts of capital are available for large deals, the need to turn to the public market for financing has diminished. For the index investor, this has major implications, as it means that a company’s most explosive growth phase increasingly takes place entirely outside the view of the public stock market.

Whereas companies used to go public to raise capital for expansion, they now do so only once their business model has been fully proven and scaled. As a result, index investors only get involved once a company has reached “maturity” and miss out on the years when the greatest value creation takes place. Scottish Mortgage thus offers access to a phase of the economy that simply remains invisible to conventional index funds.

Scottish Mortgage Investment Trust closed the trading week on the London Stock Exchange at a price of GBP 11.70 per share.

Receive weekly insights in your inbox

Exclusive analyses and updates on family holdings and global market developments.

Would you like more information about our services?

Contact usDisclaimer:

No rights can be derived from this publication. This is a publication by Tresor Capital. Reproduction of this document, or parts thereof, by third parties is only permitted with written permission and with reference to the source, Tresor Capital.

This publication has been compiled with the utmost care by Tresor Capital. The information is intended in a general sense and is not tailored to your individual situation. The information should therefore expressly not be regarded as advice, an offer or a proposal to purchase or trade investment products and/or purchase investment services, nor as investment advice. The authors, Tresor Capital and/or its employees may hold positions in the securities discussed, either for their own account or for their clients.

You should carefully consider the risks before you start investing. The value of your investments may fluctuate. Past performance is no guarantee of future results. You may lose (part of) your investment. Tresor Capital accepts no liability for any inaccuracies or omissions. This information is for indicative purposes only and is subject to change.

Read the full disclaimer at tresorcapitalnieuws.nl/disclaimer .