Family Holdings #13 - European holding companies and the financial results of their flagship companies

This week's topics:

D'Ieteren saw reported profit decline by 10.3% in 2025 due to high interest expenses and currency effects, though underlying performance (+3.8%) held up thanks to star performer Belron and growth engine PHE. While divisions such as TVH and Automotive are grappling with margin pressure and a cooling market, Belron is shining with record margins due to the increasing technological complexity of automotive glass. The group is now meticulously preparing its crown jewel for an IPO, with aggressive debt reduction and strong cash flows paving the way for a cash-out at maximum valuation.

In Brief:

Addtech (Stockholm: ADDT.B) zag onlangs een teken van vertrouwen toen bestuurslid Fredrik Börjesson voor SEK 2,1 miljoen aan aandelen kocht. Deze aankoop op de beurs van Stockholm sluit aan bij de recente trend, waarbij insiders van onze Zweedse holdings hun belangen in eigen bedrijf verder uitbreiden.

Investor AB (Stockholm: INVE.B), grootaandeelhouder van Atlas Copco, heeft deze week 214.635 aandelen gekocht in de industriële serial acquirer. De aandelen werden aangekocht tegen een koers van SEK 138,23 per aandeel, wat neerkomt op een transactiewaarde van SEK 29,7 miljoen.

KKR (New York: KKR) onderstreept het succes van zijn breedgedragen eigendomsmodel bij de verkoop van CoolIT Systems aan Ecolab voor 4,75 miljard dollar, een deal die de investeringsholding een rendement van 15 keer de inleg oplevert. Dankzij de 'skin in the game' van de 650 werknemers delen zij direct mee in dit succes met aanzienlijke uitbetalingen die variëren van één tot maar liefst acht jaarsalarissen per persoon.

Brookfield (New York: BN) gaat samen met investeerder La Caisse de Canadese duurzame energieproducent Boralex volledig overnemen in een deal met een ondernemingswaarde van circa CAD 9 miljard. Door deze privatisering krijgt Boralex toegang tot de grootschalige kapitaalbronnen en het wereldwijde netwerk van Brookfield, wat essentieel is voor de versnelde uitbreiding van hun portfolio in wind-, zonne- en waterenergie binnen Noord-Amerika en Europa.

Berkshire Hathaway (New York: BRK.B) vergroot de blootstelling aan Japan door voor circa USD 1,8 miljard een belang van 2,5% te nemen in verzekeraar Tokio Marine Holdings. De investeringsholding van nieuwbakken CEO Greg Abel zet hiermee in op een langdurige samenwerking op het gebied van herverzekeringen en sluit verdere uitbreiding van het belang in de toekomst niet uit.

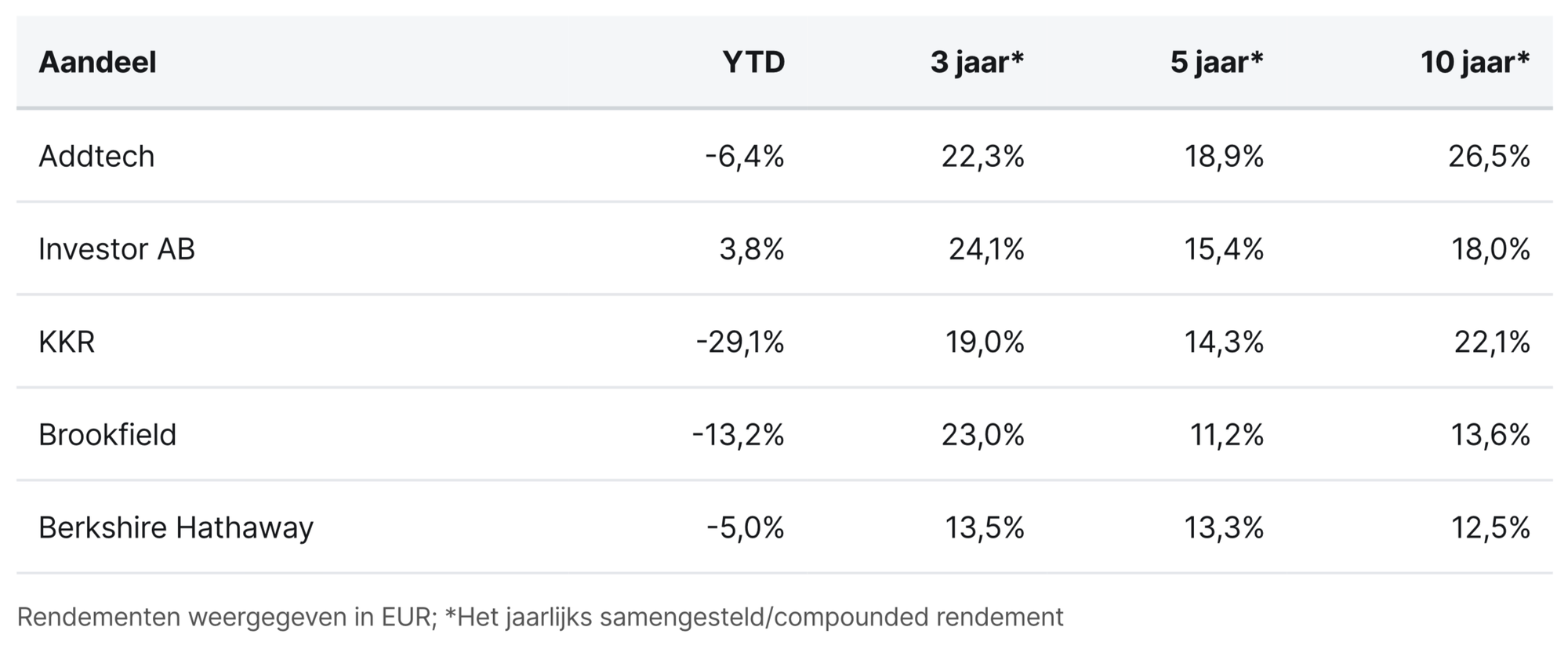

Addtech, Investor AB, KKR, Brookfield en Berkshire Hathaway zijn de handelsweek aan de beurzen van Stockholm en New York geëindigd op koersen van respectievelijk SEK 308,80, SEK 345,50, USD 88,50, USD 39,00 en USD 468,49 (B-aandeel) per aandeel.

Is a "compounding machine" heading toward standardization?

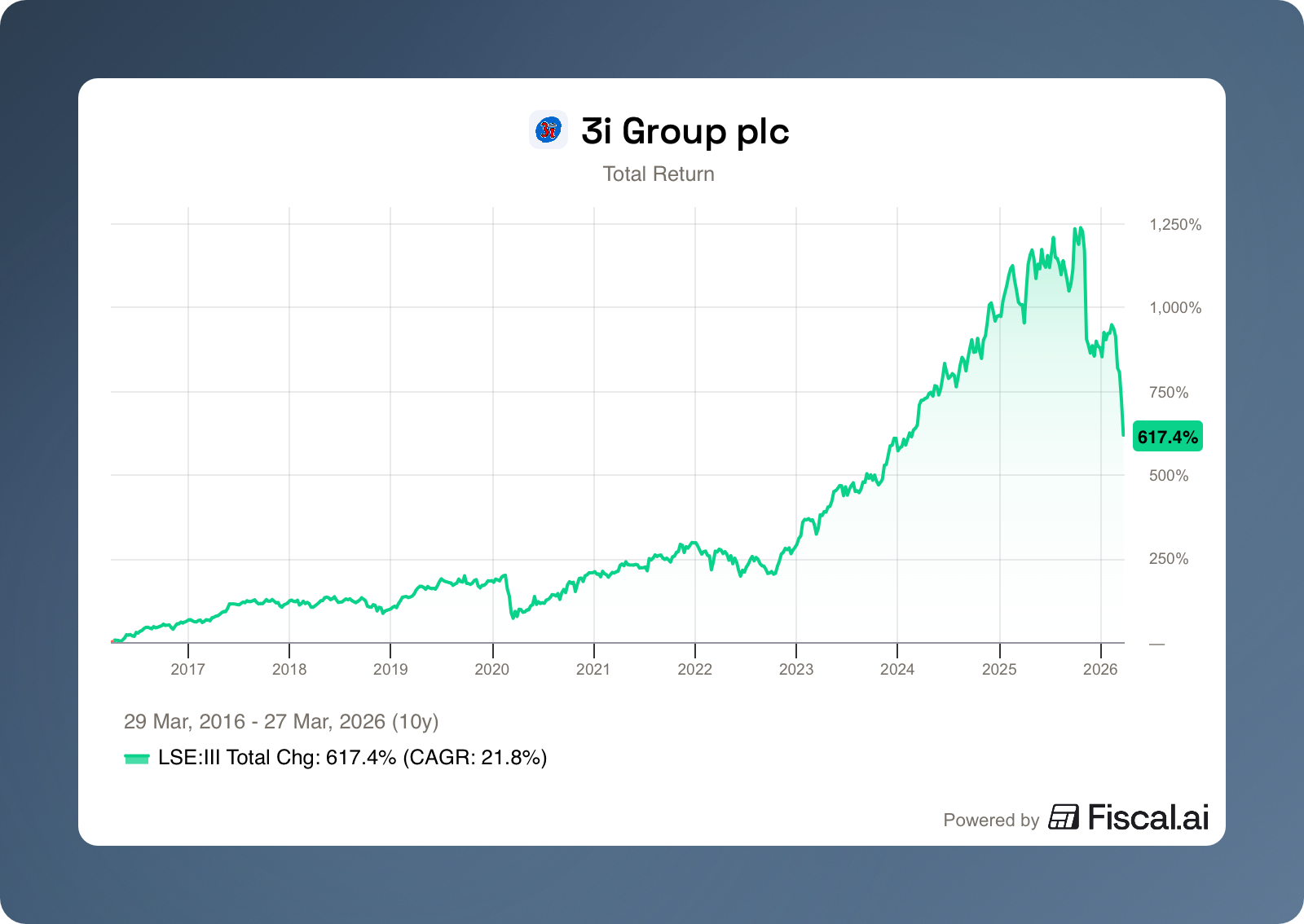

De Britse investeringsholding 3i Group (Londen: III) hield onlangs haar jaarlijkse webinar over Action, een belang dat met een aandeel van 75% tot 85% van de intrinsieke waarde de absolute kern vormt van de portfolio. Tijdens dit event gaf het management uitgebreid inzicht in de onderliggende cijfers en de strategische koers van de discountketen, waarbij specifiek werd ingezoomd op de huidige prestaties in kernmarkten zoals Frankrijk en de plannen voor intercontinentale groei.

Insights from 2025 and the first weeks of 2026

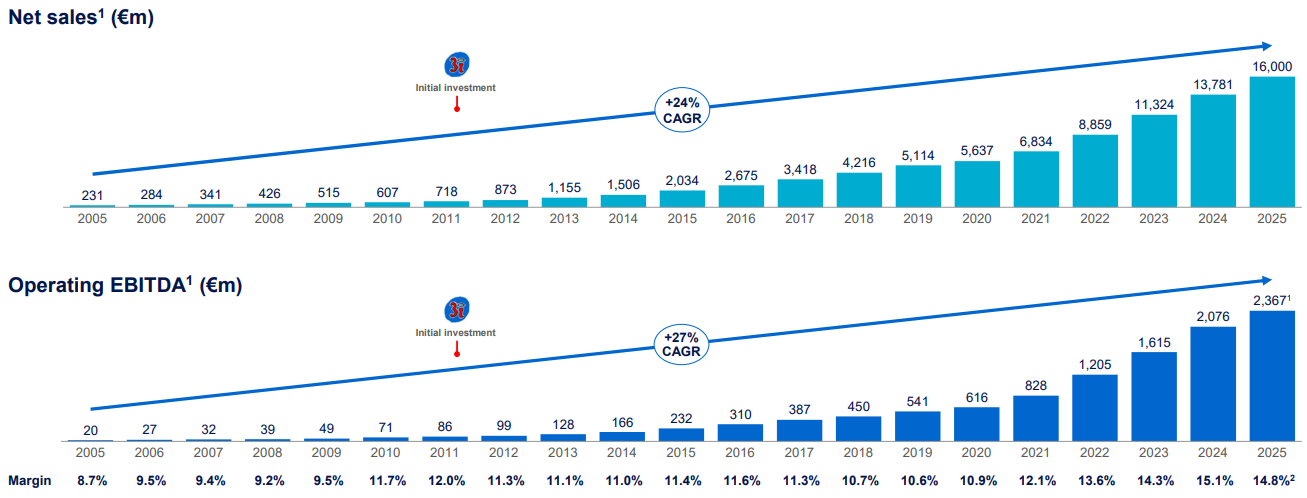

Action has built an unprecedented track record since 3i Group’s initial investment in 2011. The chain operates as a true compounding machine: since 2005, annual revenue growth has averaged 24%. Operating profitability (EBITDA) rose by as much as 27% per year during that same period, driven by a margin expansion from 8.7% to 14.8%.

De resultaten over 2025 laten een omzetgroei zien van 16,1% (tot €16 miljard) en een stijging van de winstgevendheid met 14,0%. Hoewel deze cijfers onder zowel de langjarige als de kortere termijn gemiddelden liggen (zie afbeelding hieronder), blijft het fundament van Action uiterst stabiel. Het is goed denkbaar dat we hier de eerste tekenen zien van een toekomstige normalisatie. Dat is op zichzelf een logische ontwikkeling; er zijn immers maar weinig bedrijven die een groeitempo van +20% decennialang weten vol te houden. Een zekere mate van afvlakking lijkt op termijn simpelweg een onvermijdelijk gevolg van de enorme schaal die het bedrijf inmiddels heeft bereikt.

CAGR Overview — Sales

CAGR Overview — Operating EBITDA

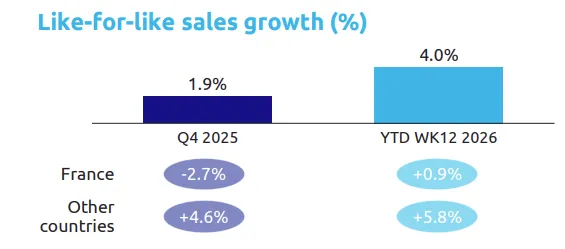

Although this could mark the beginning of a broader return to normalcy, a closer analysis shows that the current slowdown in growth is primarily concentrated in certain geographic regions. France, which accounts for approximately one-third of the group’s revenue, has been underperforming for two consecutive quarters, thereby dragging down the group’s results. In 2025, organic growth (LFL) in France stalled at a modest 1.3%, while the other markets posted a strong 7.2%. Although the weakness in France is likely to persist in the first half of 2026, an initial recovery is already visible. LFL growth improved from -2.7% in the fourth quarter of 2025 to +0.9% over the first twelve weeks of 2026.

The argument that the weakness in France, in addition to consumer confidence, is also due to market saturation or structural normalization is refuted by a comparison with the Netherlands. Although the Dutch market is virtually saturated (Action opened only three stores in the Netherlands in 2025) and holds the most mature position within the portfolio, this market actually showed above-average organic growth. This suggests that the current pressure in France is likely temporary and that growth figures will probably stabilize again in the longer term toward the group average.

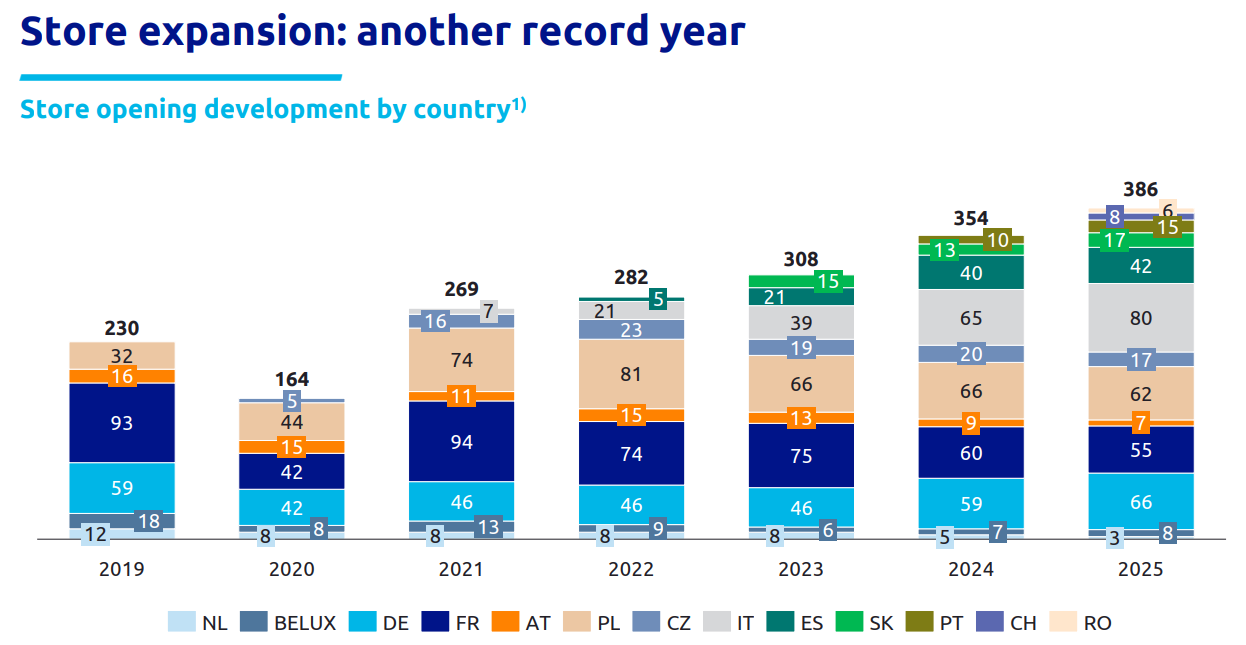

While organic growth is currently under some pressure, inorganic growth paints a very different picture. Over the past year, Action managed to open no fewer than 384 new stores, representing a 13.2% increase in its store portfolio, which is fully in line with the historical average.

This growth was partly driven by the successful expansion into Switzerland and Romania, where, according to management, the response has exceeded all expectations. In Romania, the rollout is proceeding so smoothly that a first distribution center (DC) is being opened. As is customary in Action’s logistics strategy, this DC is located near the border; in this case, in preparation for entering the Bulgarian market in 2027.

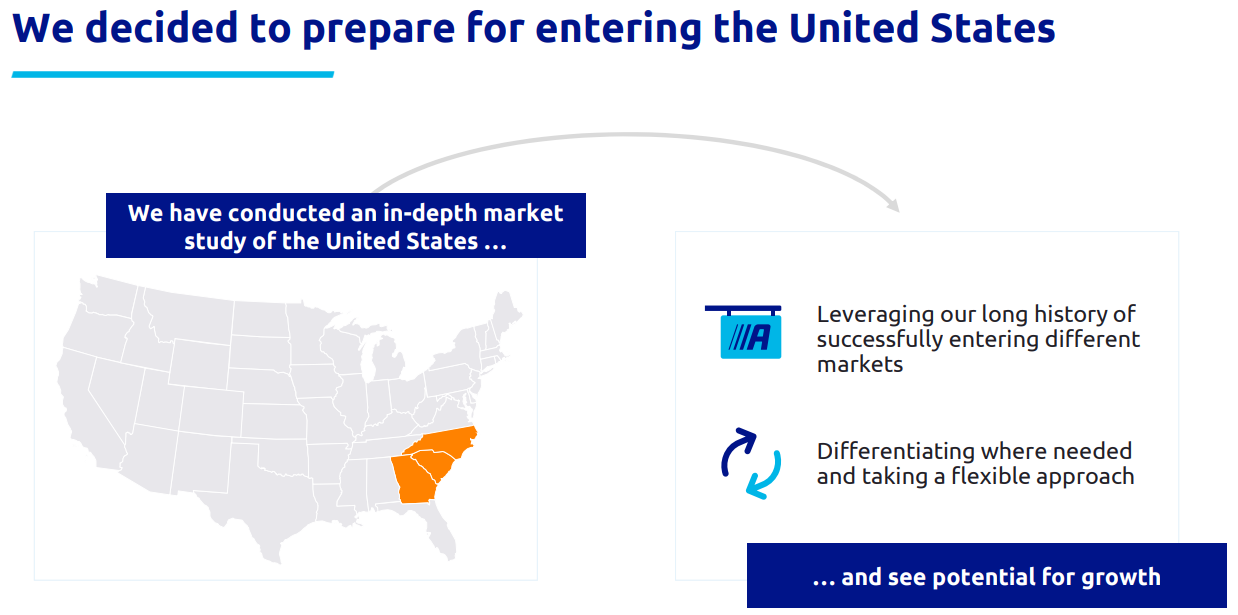

Action Goes to the U.S.A.

In addition to its expansion plans in Europe, management also unveiled concrete plans for entering the U.S. market for the first time. Following a thorough two-year study, Action has decided to enter the market in Georgia, North Carolina, and South Carolina by the end of 2027 at the earliest. By the end of 2030, 100 stores are expected to be operational in this region.

However, this expansion comes with a higher cost. Action is investing in a local procurement team and stepping up its marketing efforts to build the necessary brand awareness. In addition, capital expenditure (CapEx) per store opening in the U.S. is higher than in Europe. However, the company has already gained valuable experience with such a cost profile during its recent entry into the Swiss market. Although the payback period there is slightly above the group average due to higher costs, it is still only about one year. All of this leads to a longerbreak-even period per store, a point that investors view critically. The memory of other European retailers, such as Tesco and Sainsbury’s, which struggled in the U.S. market, is causing the market to exercise caution.

Although the United States is a challenging market with a different consumer profile and formidable competitors such as Costco, Dollarama, and Five Below, Action’s management has repeatedly demonstrated its ability to successfully scale a proven formula to new markets. Current concerns about a failure therefore seem premature.

Supply chain management

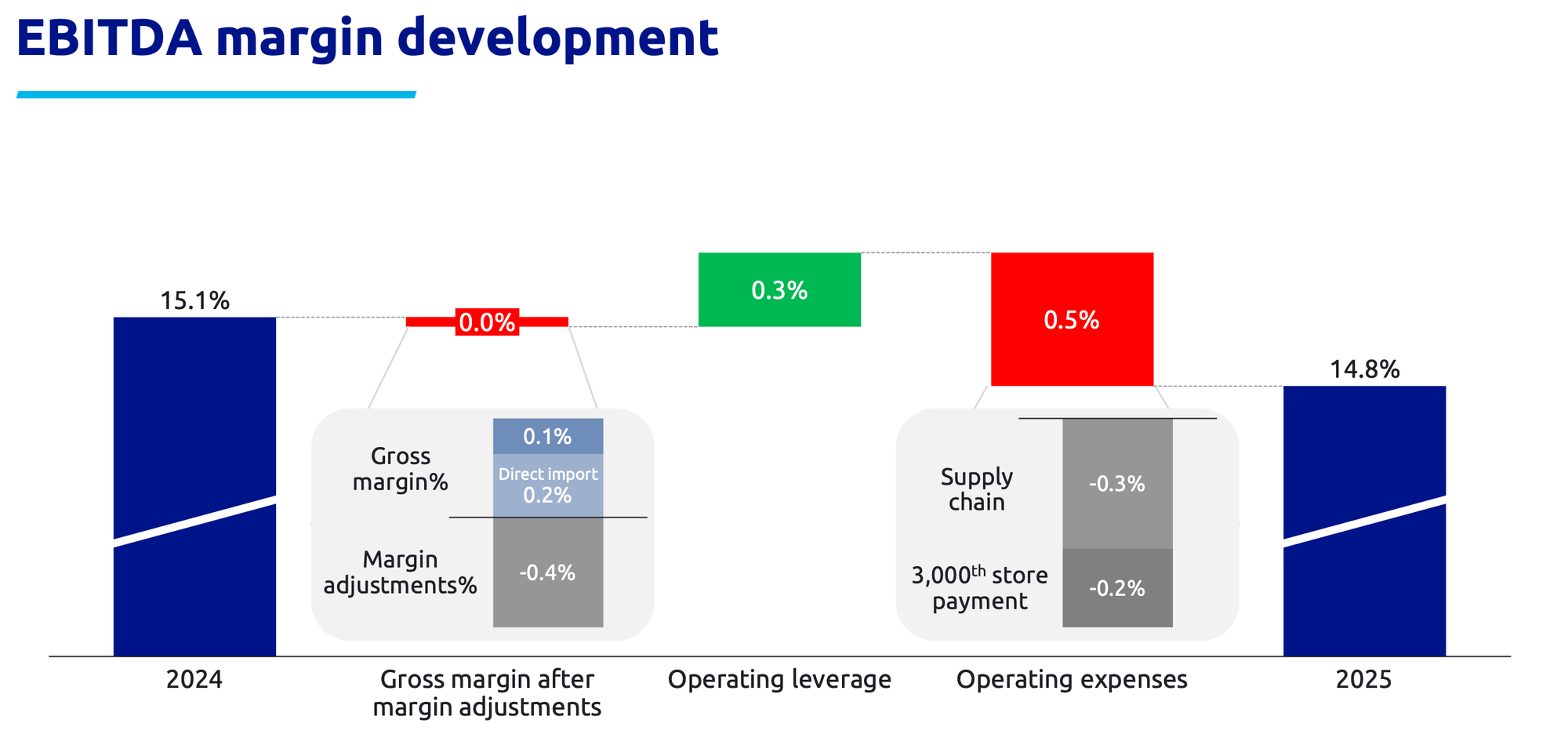

Now that revenue growth is slowing slightly, investors’ focus is inevitably shifting to margins. After all, a normalization of growth should not be accompanied by a decline in profitability. Although the margin fell slightly last year, this effect was minimal when excluding the one-time employee bonus awarded to celebrate the opening of the 3,000th store.

CFO Joost Sijpenbeek explained that the pressure on margins was partly due to a strategic investment in the supply chain. Action is increasingly sourcing products directly from manufacturers and holding them in stock itself. Although this process entails costs during the initial phase, it will ultimately lead to lower procurement costs and thus an improvement in margins.

Management is clear about how these economies of scale are distributed:

- One-third is reinvested in streamlining logistics processes.

- Two-thirds of it is used to improve quality and further lower prices.

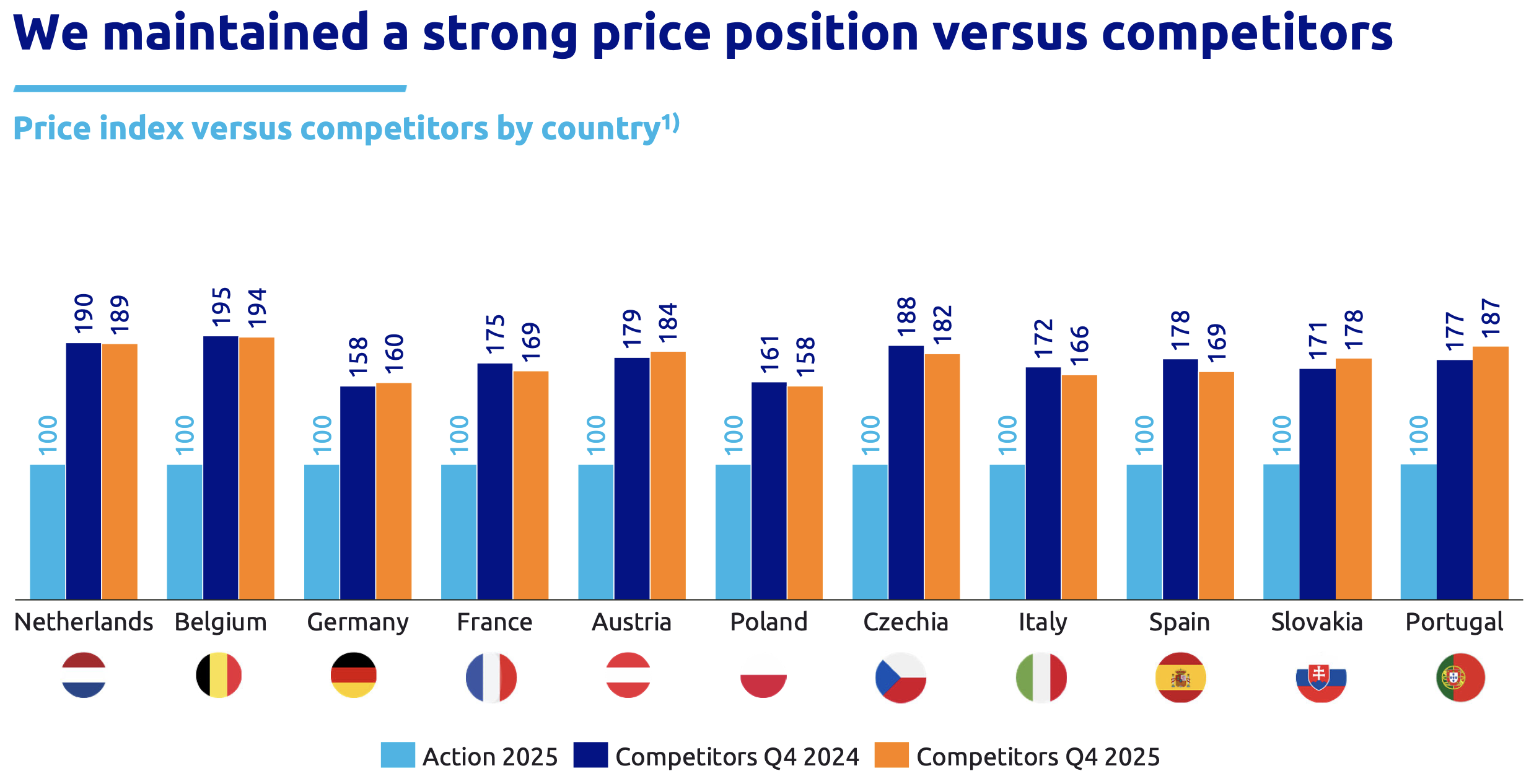

The latter is a crucial weapon in today’s market. CEO Hajir Hajji emphasized that Action in France actively lowered prices in late 2025 and early 2026 to boost flagging consumer confidence. The company can afford this aggressive pricing strategy thanks to the structural cost advantage it has built up over its competitors (see photo below).

Outlook Looking ahead to 2026, management is adopting a broader range of expectations. This caution can be directly attributed to the current geopolitical turmoil, particularly in the Middle East. After all, rising fuel prices could drive up transportation costs and, through persistent inflation, put further pressure on consumer confidence.

- Store openings:Action aims to open at least 400 new stores by 2026, with a focus on the second half of the year.

- Organic growth:The projected LFL growth of 4–5% appears conservative, but makes sense given the ongoing pressure in France. By comparison, the rest of the countries (excluding France) already posted 5.8% growth in the first twelve weeks of 2026.

- Profitability:The EBITDA margin is expected to remain stable at 14.8%.

In our view, management is thereby building in a small safety margin. Increased short-term uncertainty has led to a sharp correction in the stock market, but for the long-term investor, the fundamentals remain intact. Action is a mature organization that has proven its ability to weather economic headwinds. With the upcoming expansion in Southeast Europe and the United States, this discount giant’s growth story is far from over.

Als het miljoenendividend van Action binnenstroomt, zou het ons niet verbazen dat 3i Group een aandeleninkoopprogramma lanceert om van de actuele onderwaardering te profiteren. We houden ook de insideraankopen nauwlettend in de gaten, hetgeen als een additioneel teken van vertrouwen kan worden beschouwd.

3i Group PLC ended the trading week on the London Stock Exchange at a price of GBP 33.51 per share.

Receive weekly insights in your inbox

Exclusive analyses and updates on family holdings and global market developments.

Mixed results at D’Ieteren

D’Ieteren Group (Brussel: DIE) presenteerde recentelijk haar resultaten over 2025, waarbij de feitelijke, gerapporteerde winst vóór belastingen met 10,3% daalde tot €955,6 miljoen. Deze daling is de harde economische weerspiegeling van een jaar waarin de groep zware additionele rentelasten moest slikken door de omvangrijke schuldfinanciering eind 2024, gecombineerd met een ongunstige dollarkoers.

At constant exchange rates and excluding these additional financing costs, underlying profit growth came in at 3.8%. Although the holding company believes this better reflects the operational strength of the core businesses, this modest increase masks significant differences among them:

- Belron (Carglass):The undisputed leader. Despite headwinds in the first half of the year, a strong recovery in the U.S. led to record revenue of €6.7 billion and an impressive margin of 23.0%.

- D’Ieteren Automotive:Profit fell by nearly 10% to €215.3 million. Although the division maintained its market leadership in electric vehicles (28.8% market share), it is grappling with a challenging Belgian market and pressure on margins from manufacturers (OEMs).

- At TVH, profits plummeted by 26.3% to €72.1 million due to a global slowdown in the agricultural and forklift sectors. In addition, start-up costs for new distribution centers in the U.S. and Poland weighed on margins, while the search for a new CEO is still ongoing.

- PHE reaffirmed its role as a growth driver with a 9.7% increase in profit to €181.6 million, partly due to market share gains in France. The division is fully committed to further consolidation and is currently in exclusive negotiations regarding two major acquisitions in Spain.

Belron richting de IPO

De focus van de cijfers ligt echter onvermijdelijk op Belron, het onbetwiste kroonjuweel en de voornaamste kasstroomgenerator van de holding. Na een uitdagende eerste jaarhelft, waarin het bedrijf te kampen had met ‘claim avoidance’ door Amerikaanse verzekeraars, liet Belron in de tweede helft van 2025 een indrukwekkend herstel zien. Dit resulteerde in een recordomzet van €6,7 miljard en een aangepaste operationele marge van 23,0%.

According to CEO Francis Deprez, this success is due not only to higher volumes, but primarily to the increasing technological complexity of automotive glass. Nearly half of all repairs now require complex calibration of advanced driver-assistance systems (ADAS), which structurally increases the value per job. Management is optimistic about 2026 and expects further margin improvement toward the goal of more than 25% by 2028, supported by a normalizing U.S. market in which insurers are abandoning their defensive stance.

Tijdens de call met analisten was de IPO het onderwerp dat niet genegeerd kon worden, gevoed door recente mediaberichten over de aanstelling van zakenbanken die de beursgang moeten gaan begeleiden. Hoewel Deprez benadrukte dat D’Ieteren een "gelukkige meerderheidsaandeelhouder" is en blijft, erkende hij dat de private equity-partners in het kapitaal op termijn een exit zullen zoeken. "Wanneer dat moment precies komt, kan ik niet zeggen, omdat zij meer die knop indrukken dan wij," aldus de CEO. De groep bereidt zich echter minutieus voor door de schuldgraad van Belron in recordtempo af te bouwen, deze daalde namelijk in een jaar tijd van 5,2x naar 4,5x. Een lagere leverage in combinatie met de sterke vrije kasstroom van €374 miljoen positioneert Belron optimaal voor een beursgang tegen een maximale waardering.

Conclusie

De lauwwarme cijfers van D'Ieteren op holdingniveau wijzen op de gemengde resultaten bij de dochterondernemingen. Het toont aan dat het van belang is om een spreiding te hebben tussen diverse deelnemingen.

De ontwikkeling van de operationele cijfers van Belron en de aanstaande beursgang zullen de beurskoers de komende maanden beïnvloeden. Op langere termijn moeten TVH en PHE als serial acquirers de holding verder omhoog stuwen.

Met een ijzersterke wereldwijde marktleider als Belron, een lokale marktleider met D'Ieteren Automotive en twee goed gepositioneerde overnamemachines heeft D'Ieteren holding in ieder geval meerdere ijzers in het vuur om de komende jaren waarde te blijven creëren voor haar aandeelhouders.

D'Ieteren is de handelsweek aan de beurs van Brusse geëindigd op een koers van EUR 158,40 per aandeel.

Receive weekly insights in your inbox

Exclusive analyses and updates on family holdings and global market developments.

Would you like more information about our services?

Contact usDisclaimer:

No rights can be derived from this publication. This is a publication by Tresor Capital. Reproduction of this document, or parts thereof, by third parties is only permitted with written permission and with reference to the source, Tresor Capital.

This publication has been compiled with the utmost care by Tresor Capital. The information is intended in a general sense and is not tailored to your individual situation. The information should therefore expressly not be regarded as advice, an offer or a proposal to purchase or trade investment products and/or purchase investment services, nor as investment advice. The authors, Tresor Capital and/or its employees may hold positions in the securities discussed, either for their own account or for their clients.

You should carefully consider the risks before you start investing. The value of your investments may fluctuate. Past performance is no guarantee of future results. You may lose (part of) your investment. Tresor Capital accepts no liability for any inaccuracies or omissions. This information is for indicative purposes only and is subject to change.

Read the full disclaimer at tresorcapitalnieuws.nl/disclaimer .