Family Holdings #14 - From Record Dividends at Asseco to the Facts Behind the Panic in the Private Credit Market

This week's topics:

In 2025, the total intrinsic value of Sofina to EUR 10.8 billion, but the value per share remained virtually stable at EUR 305.77 as a result of a strategic capital increase. A 10% underlying increase in the portfolio’s value was almost entirely offset by negative exchange rate effects, resulting in a net value creation of 1.9%. With a robust gross cash position of EUR 1.7 billion and a portfolio that combines innovation with defensive stability, the company has sufficient resources for future growth.

The private credit market is currently grappling with a negative spiral in which fears about the sustainability of software loans and media pressure are leading to a run on semi-liquid funds. Although quality players such as Brookfield and Oaktree are proving their stability by stepping in with their own capital and employing conservative structures, market sentiment often unfairly equates them with weaker industry peers. At KKR , actual exposure to the riskiest credit segments is limited to approximately 5% of total assets, a fact recently underscored by management with a substantial share buyback of USD 50 million.

In Brief:

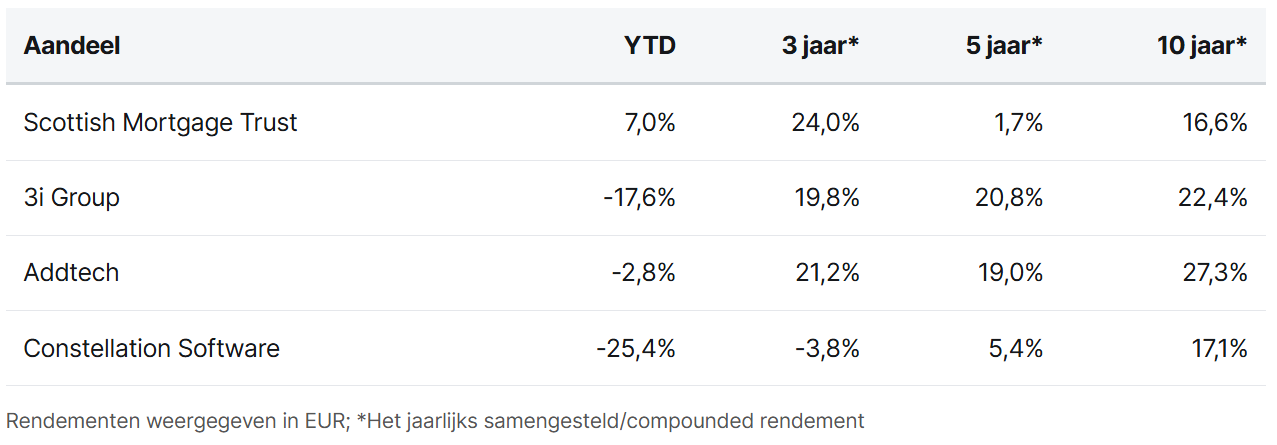

The Scottish Mortgage Investment Trust (London: SMT) has significantly increased the valuation of its stake in SpaceX. The valuation of Elon Musk’s space company has been raised on the balance sheet; although the exact figures have not yet been released, it is likely to approach $1 trillion or more. As a result of this increase in value, SpaceX’s weighting within the total portfolio has risen to 19.3%, further strengthening its already dominant position in the trust.

Following a sharp decline in the share price of 3i Group (London: III), management is sending a clear signal by buying back shares on a large scale. Peter Wirtz, Head of Private Equity and Senior Partner at 3i Group, increased his stake in the company by purchasing 25,000 shares. At a price of £23.39 per share, this investment amounted to nearly £600,000. CEO Simon Borrows, however, went one step further. Having recently acquired 30,000 shares, he has now purchased over 350,000 more in a single transaction. With this additional investment of nearly £9 million, Borrows underscores his unwavering confidence in the company’s intrinsic value and long-term potential.

The Swedish acquisition powerhouse Addtech ( Stockholm: ADDT.B) has acquired the Dutch company Staka through its Safety business unit. Staka designs, manufactures, and sells custom-made outdoor enclosures for European installers and OEM customers in sectors such as energy, infrastructure, and water management. The company has approximately 60 employees and generates annual revenue of about €15 million.

Constellation Software (Toronto: CSU) continues to be active through its subsidiaries, having completed several more acquisitions. In the United States, Perseus acquired IronHQ, a North Carolina-based provider of CRM and inventory management software for dealers in the agricultural and construction sectors, while Volaris made a move in Germany with the acquisition of zetVisions, a Heidelberg-based specialist in legal entity management and master data management software. Furthermore, Vela expanded its presence in Croatia through the acquisition of Infoprojekt, a provider of ERP systems for local governments, and its subsidiary Datamine in South Africa acquired Mineware, a company that provides operational software and consulting services to the mining sector.

Scottish Mortgage Trust, 3i Group, Addtech, and Constellation Software closed the trading week on the London, Stockholm, and Toronto stock exchanges at prices of GBP 12.68, GBP 26.87, SEK 320.60, and CAD 2,441.27 per share, respectively.

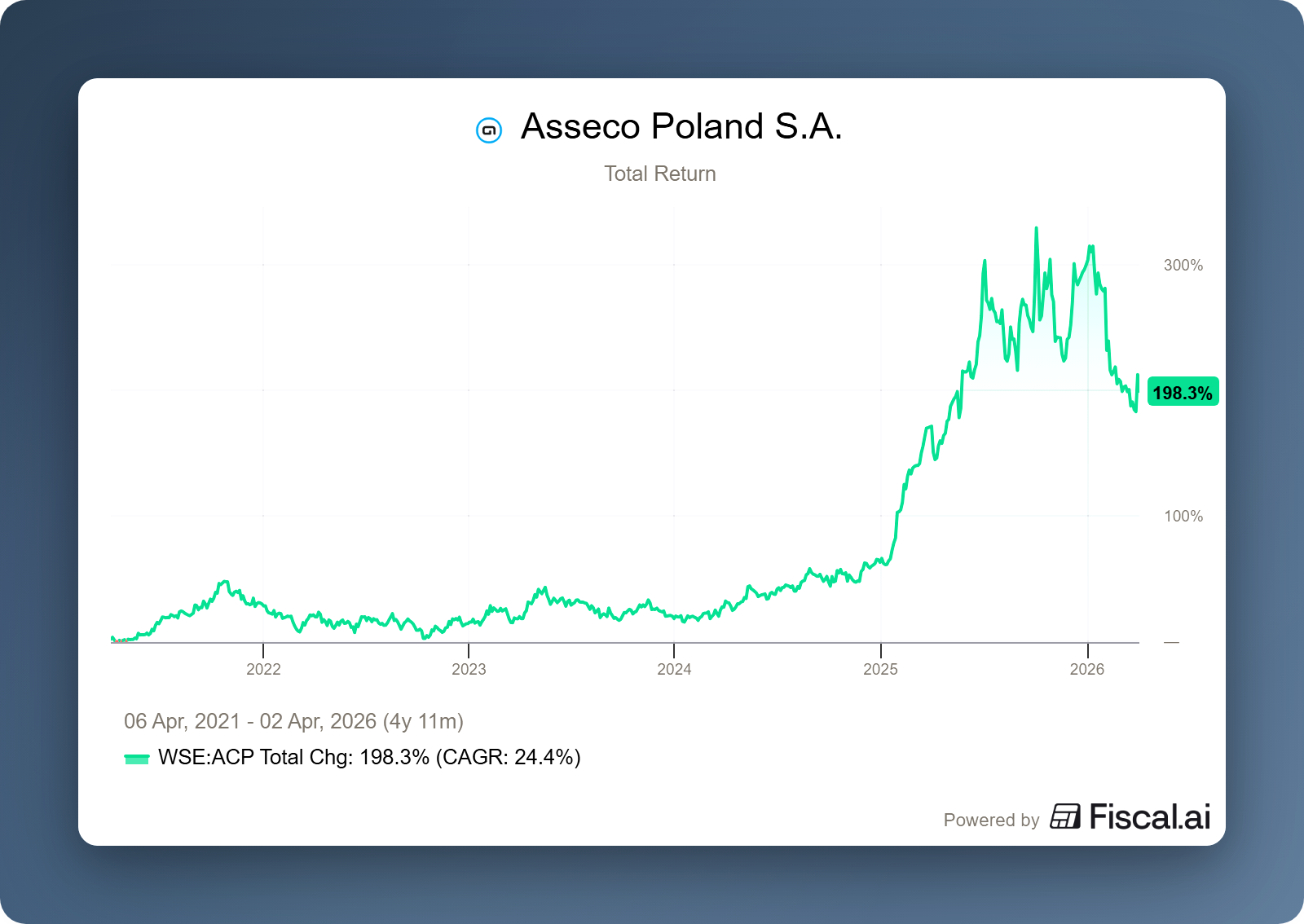

Asseco's strong profits lead to a record dividend for shareholders

Asseco Poland (Warsaw: ACP) published its 2025 annual results on March 31; so late, in fact, that they could have presented them almost simultaneously with the Q1 results. Looking at the presentation, it is striking that the company is communicating with increasing transparency. This is likely not entirely unrelated to the arrival of Topicus as a major shareholder. For many investors, that stake is therefore at the core of their investment thesis. The company’s focus is on improving margins without hindering growth.

For investors in Asseco Poland, the consolidated figures are only partially relevant. Because the company has significant minority interests, particularly through Formula Systems, the consolidated results paint a distorted picture. Therefore, anyone who wants to see Asseco’s true value must look at the pro forma results. These show exactly what portion of the profit and revenue belongs to the holding company’s shareholders.

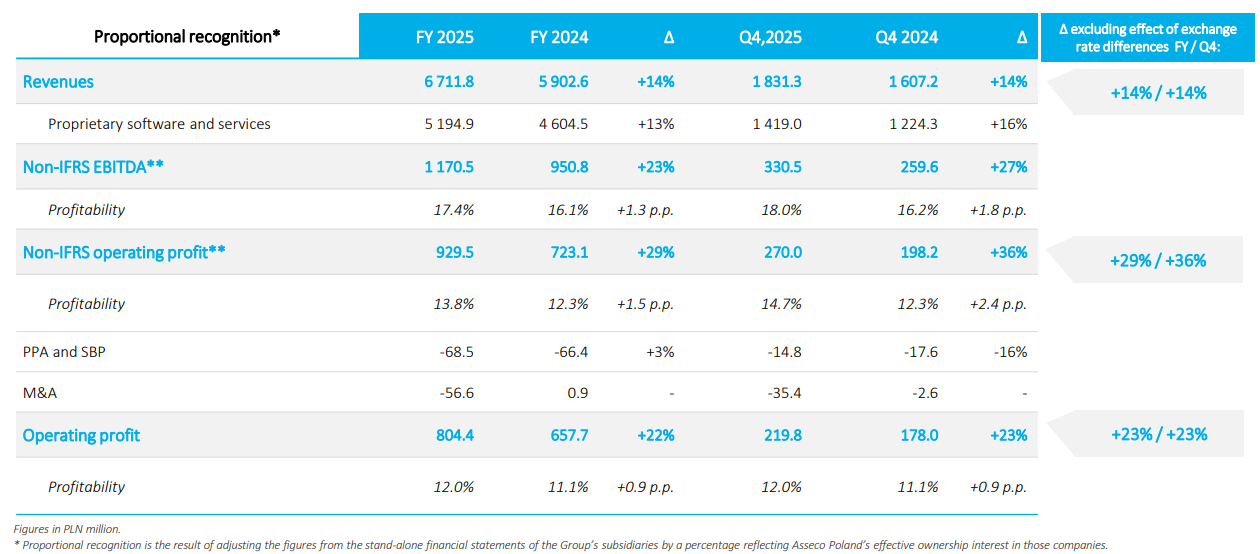

The key figures paint an encouraging picture. In 2025, revenue grew by 14% to PLN 6.7 billion, with 12.4% of that growth coming from organic sources. While management is very proud of this, the real focus is on profitability. On an annual basis, the EBITDA margin increased by 1.3 percentage points to 17.4%, and the operating profit margin rose by 1.5 percentage points to 13.8%. On a quarterly basis compared to the last quarter of last year, the margin improved by as much as 2.4 percentage points.

The Constellation Group—and thus Topicus/TSS as well—has always openly stated that, in its own words, it is capable of guiding every company in its ecosystem toward an operating margin of approximately 30%. Asseco is still a long way from that, but the first quarters under TSS’s involvement are already showing positive momentum. We saw a similar scenario earlier with the Polish company Sygnity; after TSS’s intervention, this company transformed from a mediocre player into an efficient vertical software powerhouse with high profitability.

Dividend Payout Beneficial for Topicus

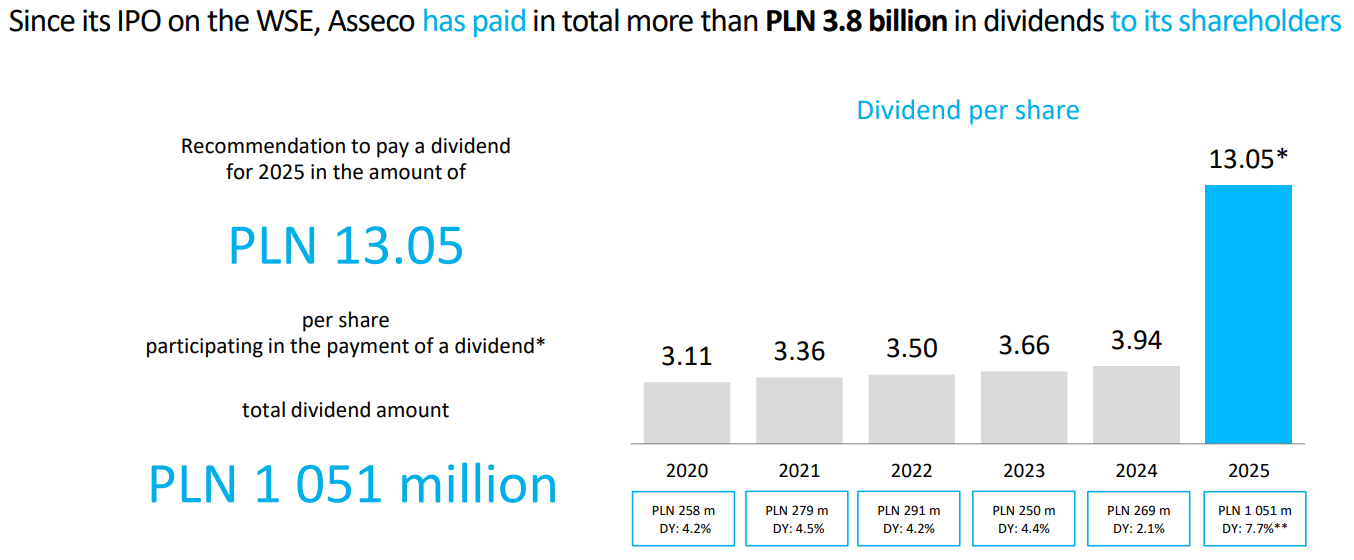

It had been known for some time that Asseco would propose a special dividend payout in 2026 and, if approved, would carry it out. This distribution stems from the earlier sale of treasury shares to Topicus/TSS and the sale of the stake in Sapiens International to subsidiary Formula Systems in 2025. Last week, management announced that the sale of the Sapiens stake generated an accounting profit of approximately PLN 500 million for the parent company’s shareholders.

The proposed amount of the special dividend has now been set at PLN 13.05 per share. Based on the current share price of approximately PLN 170, this represents a dividend yield of nearly 8%, and the total payout amounts to PLN 1.051 billion (approximately EUR 245 million).

For Topicus, which holds a stake of approximately 25% in Asseco, this proposal represents a significant cash inflow. Since they made their investment at a purchase price of PLN 85 per share, this single dividend will immediately return more than 15% of their original investment.

AI as an Expert Amplifier

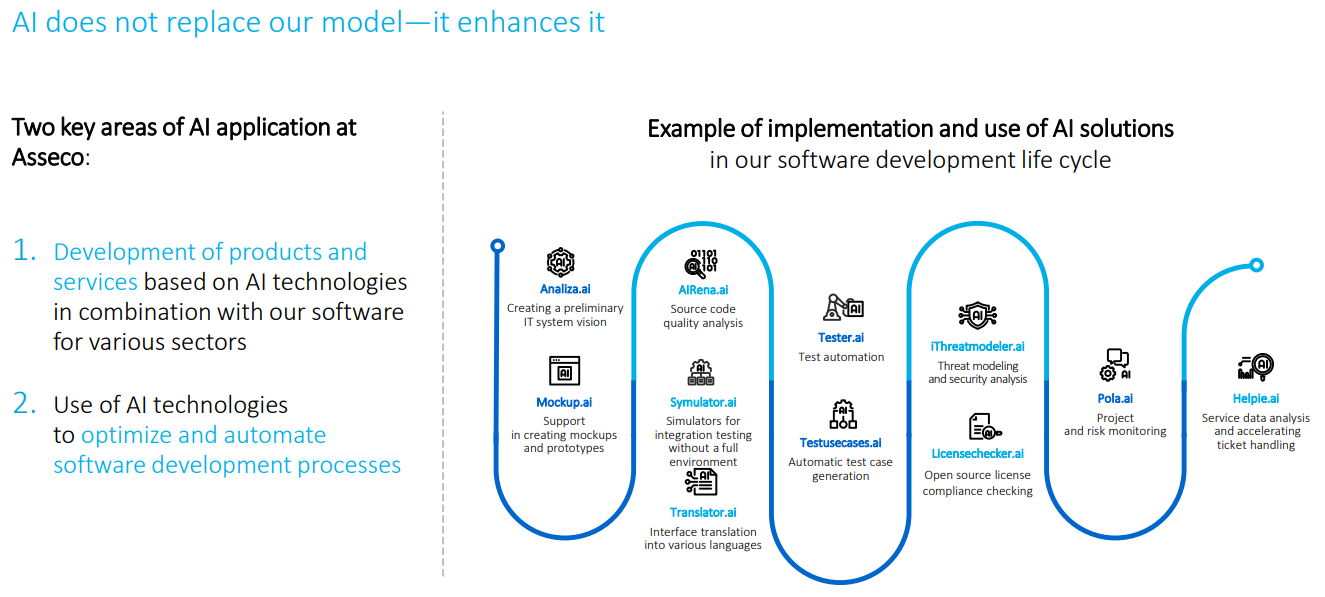

Another notable slide in the report focuses on the organization’s use of AI. It is inevitably the most discussed topic within the VMS sector, a fact that will not have escaped the attention of our newsletter readers. The slide provides an overview of internal AI tools that the company has installed and built in-house for its own development processes. These range from Mockup.ai for building prototypes to Tester.ai for test automation, AIRena.ai for code quality analysis, and iThreatmodeler.ai for threat modeling and security analysis.

Adam Góral, founder and chairman of the board of directors at Asseco, emphasizes that the rise of artificial intelligence is having an irreversible impact on the industry. He states: "AI is undoubtedly shaping our world, and our companies must respond appropriately." In his view, however, AI is not a replacement for human specialists, but a tool to enhance service quality and improve efficiency. The group’s goal is to achieve more with the exact same team by deeply integrating AI solutions into the internal production process.

According to Góral, Asseco’s foundation lies in the knowledge accumulated over many years by its more than 30,000 employees—whom he prefers to describe as his “business partners”—spread across more than 50 countries. In an industry where 87% of the workforce is employed in product-related roles, this deep, industry-specific expertise serves as the most significant barrier to competition. With an average tenure of 12 years at Asseco Poland, the organization possesses unique knowledge of complex customer processes in sectors such as healthcare, banking, and government. This years-long experience and human intelligence form the foundation upon which AI builds; Góral believes that AI will actually require more time to match or replace such non-standard, specialized solutions.

Asseco Poland closed the trading week on the Warsaw Stock Exchange at a price of PLN 178.20 per share.

Receive weekly insights in your inbox

Exclusive analyses and updates on family holdings and global market developments.

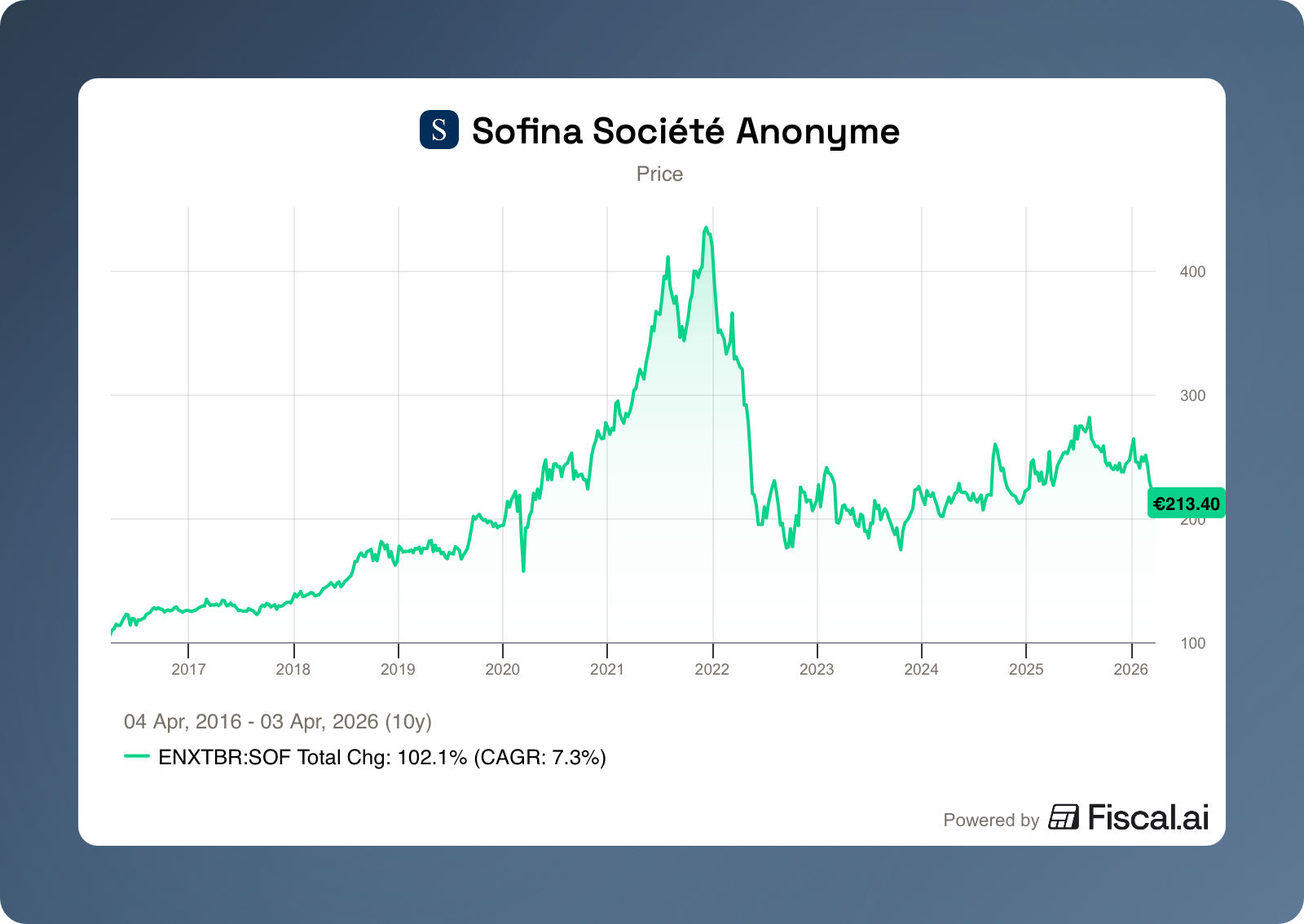

Sofina reports solid results for 2025

Sofina’s (Brussels: SOF) results for the 2025 fiscal year demonstrate resilience in a challenging market. While total Net Asset Value (NAV) rose to EUR 10.8 billion (compared to EUR 10.3 billion at the end of 2024), value per share remained virtually stable at EUR 305.77 compared to EUR 311.77 the previous year. Although total NAV increased in absolute euro terms, this was spread across more outstanding shares due to the recent capital increase.

Without this capital injection, the NAV per share would have been higher, but the decision to issue new shares was necessary to build up a "war chest" for future growth. This was a strategic move; Sofina saw deal flow in the market accelerating and wanted to have the necessary firepower to be able to act more aggressively in the coming years.

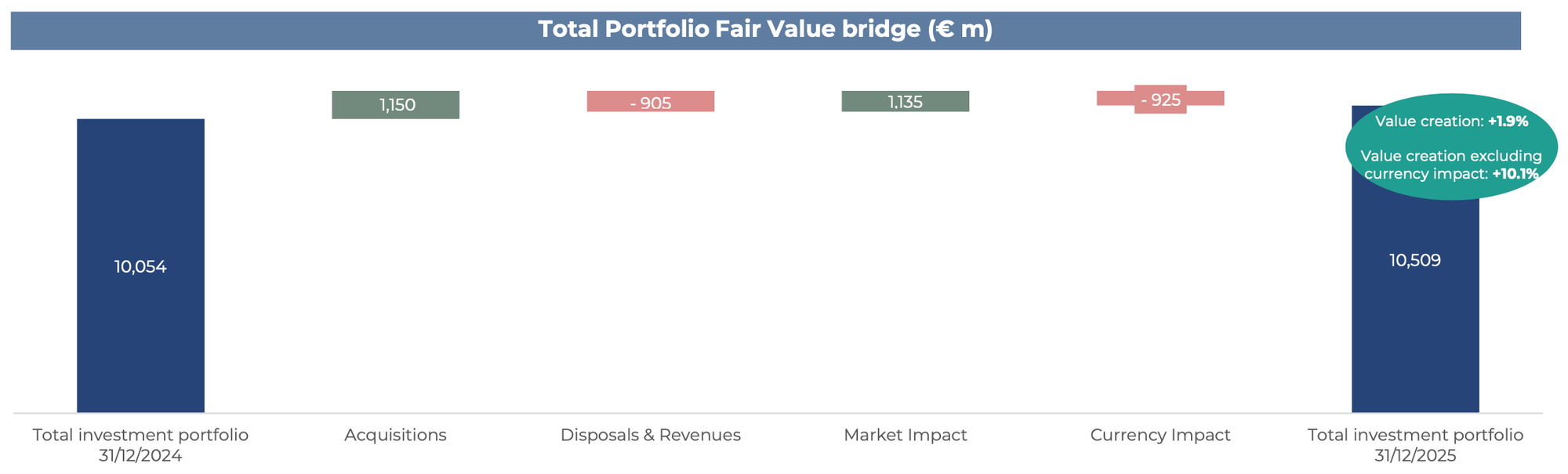

To understand how things have evolved over the past year, let’s look at the chart below. It shows the “bridge” in the portfolio’s performance.

Sofina invested slightly more (in acquisitions) than it recovered in capital (from sales and capital distributions from funds). What stands out in the chart is the approximately 10% increase in the portfolio’s value. "Market impact" reflects this underlying increase in value. However, this is almost entirely offset by the impact of exchange rates, resulting in actual value creation of only 1.9%.

CEO Harold Boël explained during our investor day that this has a neutral effect on operations over the very long term. In an international business model, exchange rates work in your favor one year and against you the next. Sofina’s broad geographic spread, with interests in the U.S., Europe, and Asia, and the fact that Sofina buys and sells foreign currencies such as dollars on a daily basis through the capital calls and distributions of its venture and growth capital funds, acts as a natural hedge that smooths out these fluctuations over time.

Would you like to read more about Tresor Capital’s investor day and the content of Mr. Boël’s presentation? You can do so via the link below:

Despite its strong fundamentals and active deal flow—including new investments in companies such as Scalable Capital and IPOs by Lenskart and Pine Labs, among others—the consensus is that "things need to and could be better." With a gross cash position of EUR 1.7 billion and a low loan-to-value ratio of 4.1%, Sofina certainly has the firepower to realize that ambition in the next cycle.

Looking at the portfolio’s actual composition, we see that Sofina’s top 10 holdings now collectively account for approximately 29% of the total value. This concentration reflects where Sofina has the strongest conviction.

What makes this portfolio unique is the balance between high growth and defensive stability. While the hundreds of smaller investments made through the Sofina Private Funds provide broad exposure to innovation, the bulk of the capital is strategically allocated to structural growth trends such as Digital Transformation (23%) and Education (14%).

At the same time, the positions in Consumer (22%) and Healthcare (12%) (such as Cognita in the top 10) provide an essential counterbalance. These sectors are less sensitive to economic cycles and form the qualitative anchor of the portfolio. It is precisely this specific mix that explains Sofina’s resilience: a combination of aggressive growth opportunities and defensive value creation, supported by a rock-solid cash position.

Sofina closed the trading week on the Brussels Stock Exchange at a price of EUR 214.20 per share.

Headlines are causing concern in the private credit sector

The private credit market is currently under significant pressure. While traditional private credit strategies typically have a maturity of about seven years—with distributions made on a quarterly basis only after a certain number of years have passed, and with no real exit options—new semi-liquid funds have been established in recent years to meet the growing demand from individual (retail) investors. These offer investors the option to request up to 5% of the fund’s value for redemption each quarter, a structure that is causing quite a stir in the current market climate.

The prevailing concern is that many of these loans are carried on the balance sheet at values that, partly due to the rapid rise of AI, are no longer sustainable. Investors assume that a large portion of these loans has been extended to software companies whose market value in the near future will be significantly lower than their current book value justifies.

Due to current market anxiety, many funds are now reaching these limits. It is crucial to understand that these limits exist to protect both the fund and the investors. Because the underlying investments have a long-term horizon and are inherently illiquid, premature liquidation of positions could seriously harm returns for existing investors. However, an essential distinction must be made here: forced sales of underlying assets should only occur if the manager cannot absorb the outflow from its own liquidity position or current cash flows.

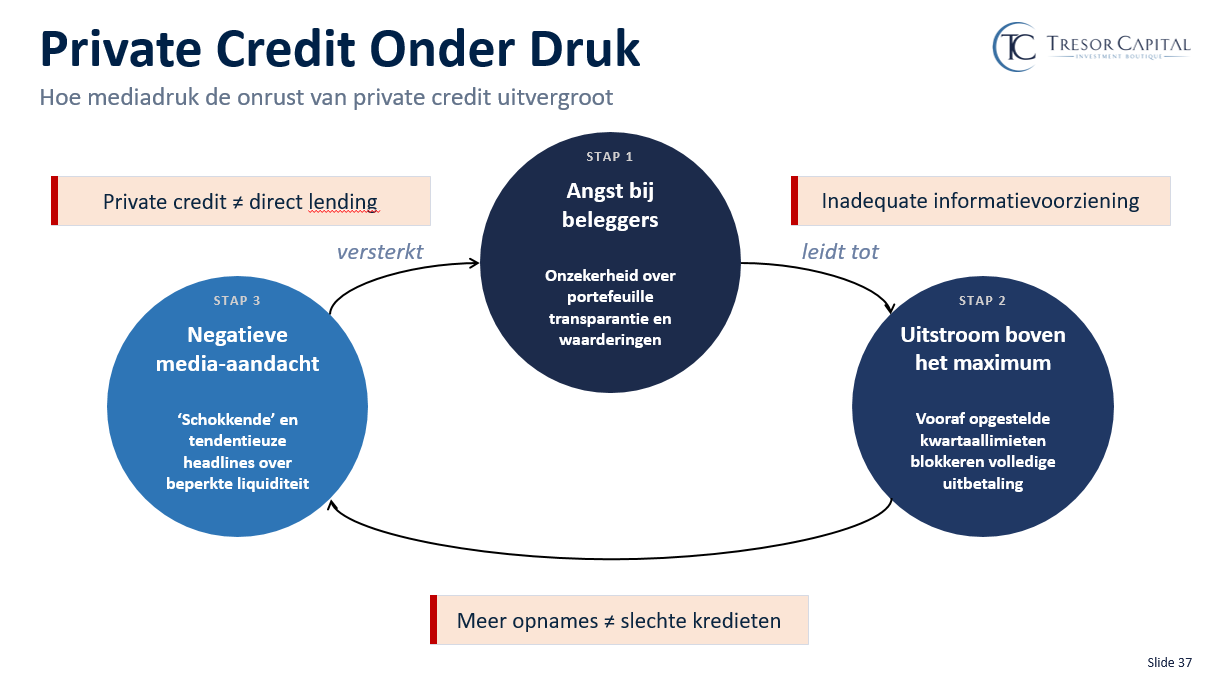

What we are currently seeing in the market is a self-perpetuating cycle of fear. As the attached image illustrates, a harmful dynamic is emerging: uncertainty about valuations is driving investors en masse toward the exit, causing maximum outflow limits to be immediately reached. As soon as that “door” closes, the media jumps on the story with sensational headlines. In this coverage, terms like private credit and direct lending are often unfairly lumped together. The negative tone also suggests that an increase in drawdowns is synonymous with bad loans, which only further fuels panic among investors. This creates a vicious cycle in which inadequate information and media pressure push the markets unnecessarily deeper into the red.

This exposes a fundamental flaw in the information provided by fund managers. Investors have invested in funds whose illiquid nature and associated risks they were unable to fully grasp. In this vicious cycle, the combination of this structural mismatch and the resulting media pressure is driving the market down.

Brookfield

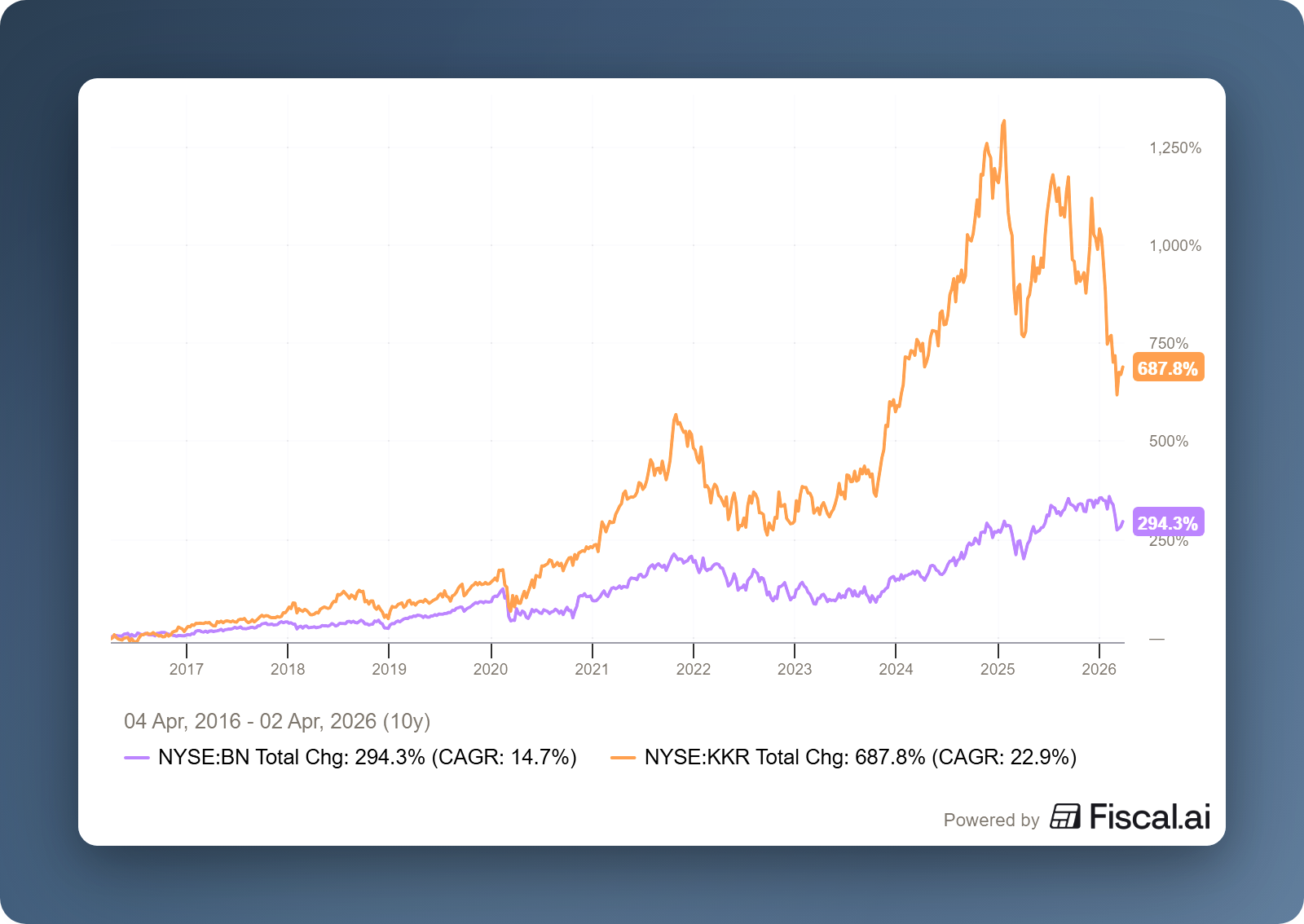

At Brookfield (New York: BN) and its subsidiary Oaktree, we see a reassuring dynamic. They have chosen to cover any liquidity shortfalls partly out of their own pockets. This “skin in the game” sends a powerful signal to the market that the underlying value of their portfolios is solid.

Armen Panossian (co-CEO of Oaktree) states that we are currently seeing a correction, but that it is not systemic. He specifically points to a difference in performance between loans issued before 2022 and those issued afterward. Panossian emphasizes that Oaktree has prepared for this by prioritizing client interests: “We couldn’t predict exactly what would happen, but we did prepare by operating prudently, maintaining liquid assets, and not overleveraging.” As a result, they are now able to capitalize on the volatility.

Connor Teskey (CEO of Brookfield Asset Management) elaborates on this from Brookfield’s perspective. He points out the human tendency to misjudge liquidity: “Liquidity is a strange instrument; it is vastly overvalued when you don’t need it, but it is undervalued in an almost laughable way when you do need it.” Brookfield’s strength lies in its focus on the “backbone” of the economy and its careful de-risking of deals to ensure it isn’t backed into a corner precisely during those rare moments.

A highly recommended interview with Connor Teskey, CEO of Brookfield Asset Management

In the interview, Teskey states that Brookfield tries to structure deals in such a way that they are exposed only to operational risk. Nevertheless, they cannot escape the negative correlation associated with the umbrella terms “private equity” and “credit”; when bad news emerges about structurally poorly managed peers in the sector, general market sentiment often unfairly lumps them into the same category.

KKR

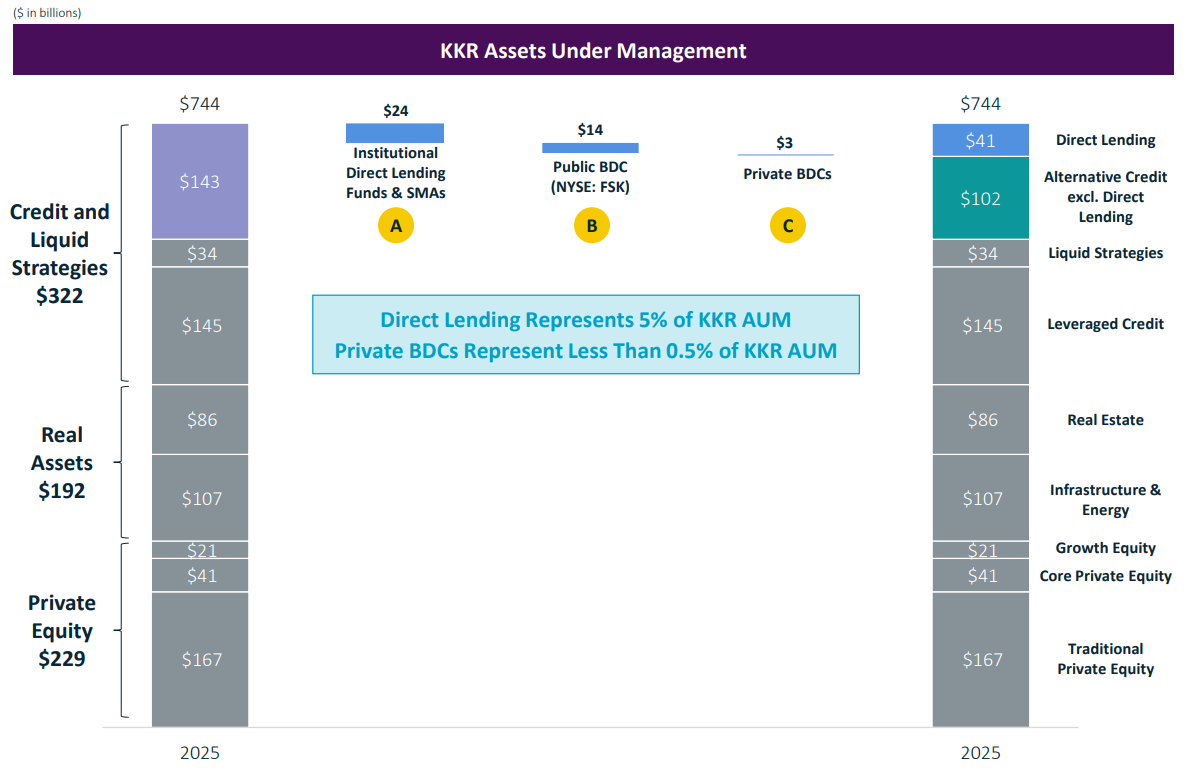

At KKR (New York: KKR), the situation is more nuanced. Compared to Brookfield, they are slightly more exposed to the current market pressure and have not chosen to the same extent to immediately replenish the full outflow with their own capital. Although this makes KKR more sensitive to market sentiment on paper, it is essential to put this into the right perspective. Relative to their total assets under management (AUM), the exposure remains very manageable. As the chart shows, Direct Lending—the segment currently receiving the most media attention — accounts for approximately 5% of total AUM. The BDCs, which are at the center of the discussion regarding drawdown limits, account for less than 3% of total capital.

Management has responded to these market dynamics through share buybacks, with the co-CEOs and other insiders recently purchasing more than USD 50 million worth of company shares using their personal funds. While headlines are currently heavily focused on credit-related segments, the majority of KKR’s portfolio remains allocated to sectors such as infrastructure, energy, and traditional private equity, which have a different risk profile.

Brookfield and KKR closed the trading week on the New York Stock Exchange at USD 40.89 and USD 91.23, respectively.

Receive weekly insights in your inbox

Exclusive analyses and updates on family holdings and global market developments.

Would you like more information about our services?

Contact usDisclaimer:

No rights can be derived from this publication. This is a publication by Tresor Capital. Reproduction of this document, or parts thereof, by third parties is only permitted with written permission and with reference to the source, Tresor Capital.

This publication has been compiled with the utmost care by Tresor Capital. The information is intended in a general sense and is not tailored to your individual situation. The information should therefore expressly not be regarded as advice, an offer or a proposal to purchase or trade investment products and/or purchase investment services, nor as investment advice. The authors, Tresor Capital and/or its employees may hold positions in the securities discussed, either for their own account or for their clients.

You should carefully consider the risks before you start investing. The value of your investments may fluctuate. Past performance is no guarantee of future results. You may lose (part of) your investment. Tresor Capital accepts no liability for any inaccuracies or omissions. This information is for indicative purposes only and is subject to change.

Read the full disclaimer at tresorcapitalnieuws.nl/disclaimer .