Family Holdings #15 - MBB's Record Figures Leave Us Wanting More

This week's topics:

Chapters Group is accelerating its AI offensive with the launch of Altamount Ignite, a new venture designed to drive innovation within its portfolio companies. To finance this growth and new “AI-proof” acquisitions, the holding company is raising additional capital from an existing bond issue. In doing so, Chapters reaffirms its aggressive strategy to create sustainable value through technological leadership and rigorous investment criteria.

Brookfield and KKR are caught up in the market turmoil surrounding private credit. We provide the nuance that sensationalist media fail to deliver.

Following the impressive annual results from 3i Group subsidiary Action, attention is now turning to the planned expansion into the United States in 2027. Despite his reputation as Mr. No, 3i CEO Simon Borrows has given the green light to this project. Together with CEO Hajir Hajji, he is convinced that the unique Action concept fills a gap in the U.S. market that has remained untapped until now.

Berkshire Hathaway’s Warren Buffett may have officially stepped down as CEO, but anyone who hears him speak on CNBC immediately realizes that the 95-year-old investor is still keeping a close eye on everything. Although his age is starting to take its toll physically and his voice has slowed somewhat, his mental acuity remains unchanged. In a candid conversation, he shares his view on the current market, explains why he sold Apple too early, and warns of the silent power of inflation affecting savers worldwide.

In Brief:

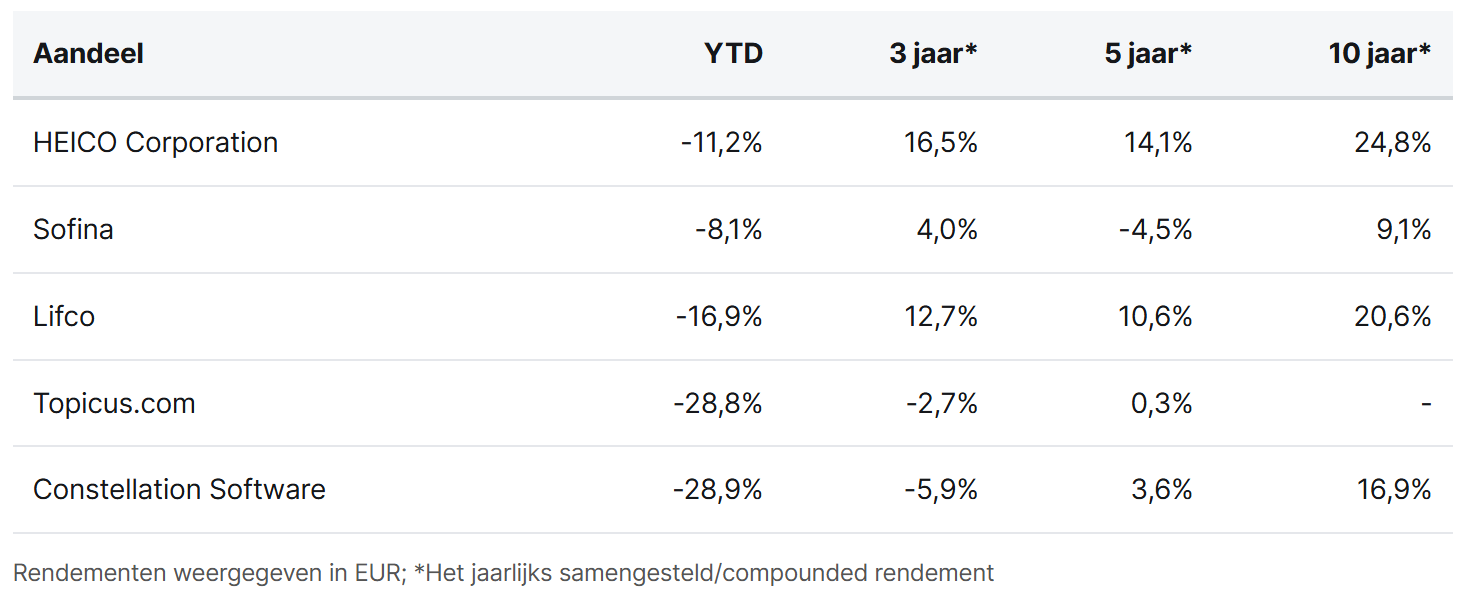

Heico ( New York: HEI.A) further strengthened its position in the defense and aviation sectors this week with two strategic acquisitions within both of the company’s divisions. The Flight Support Group acquired an 80% stake in Sherwood Avionics and Accessories, a specialist in the maintenance and overhaul (MRO) of critical components for military platforms such as the C-130 and F-16. Shortly thereafter, the Electronic Technologies Group acquired a 90% stake in Southwest Antennas, further expanding Heico’s expertise in high-performance antenna technology for defense and law enforcement.

Vinted, one of the key portfolio companies of the Belgian holding company Sofina ( Brussels: SOF), has surpassed the EUR 1.1 billion revenue milestone for the first time, representing growth of nearly 40%. Despite this record revenue, net profit fell by 19% to EUR 62 million, which CEO Thomas Plantenga attributes to significant investments in new markets (such as the U.S.) and lower-cost delivery options. Although there are rumors of an IPO, the CEO emphasizes that this is not currently on the agenda; the platform is now focusing first on international expansion and new categories such as electronics.

The Swedish acquisition powerhouse Lifco ( Stockholm: LIFCO.B) has acquired a majority stake in the Italian company Metalltech. This company specializes in the design and manufacture of expanded metal for architectural applications. With 53 employees, the company generated revenue of approximately EUR 15.8 million in 2025. Following the acquisition, Metalltech will be consolidated within Lifco’s Systems Solutions division.

Within the Constellation family, there were numerous insider purchases between March and April 2026. At Topicus ( Toronto: TOI), executives such as Robin van Poelje and Ramon Zanders significantly increased their holdings through the usual purchase plans, with the combined purchases by these insiders totaling over $1.6 million. There was also plenty of activity at Constellation Software ( Toronto: CSU) itself, with buyers such as Jeffrey Bender, Dexter Salna, and Barry Symons collectively acquiring more than $1.8 million worth of shares.

On top of that, Constellation Software ’s ( Toronto: CSU) acquisition spree continues in full swing. Its subsidiary, Volaris Group, acquired the Brazilian company Interplayers. Interplayers serves as a technology hub that connects the entire healthcare chain in Brazil through software, IT services, and consulting. Their platform integrates the value chain for a wide range of clients, including clinics, hospitals, pharmacies, distributors, and health insurers. With approximately 900 employees, this can be viewed as a very substantial acquisition; the purchase price remains undisclosed.

Heico, Sofina, Lifco, Topicus, and Constellation Software are traded on the New York, Brussels, Stockholm, and Toronto stock exchanges at prices of USD 219.13 (Class A shares), EUR 223.60, SEK 292, CAD 91.37, and CAD 2,284 per share, respectively.

MBB's record figures leave us wanting more

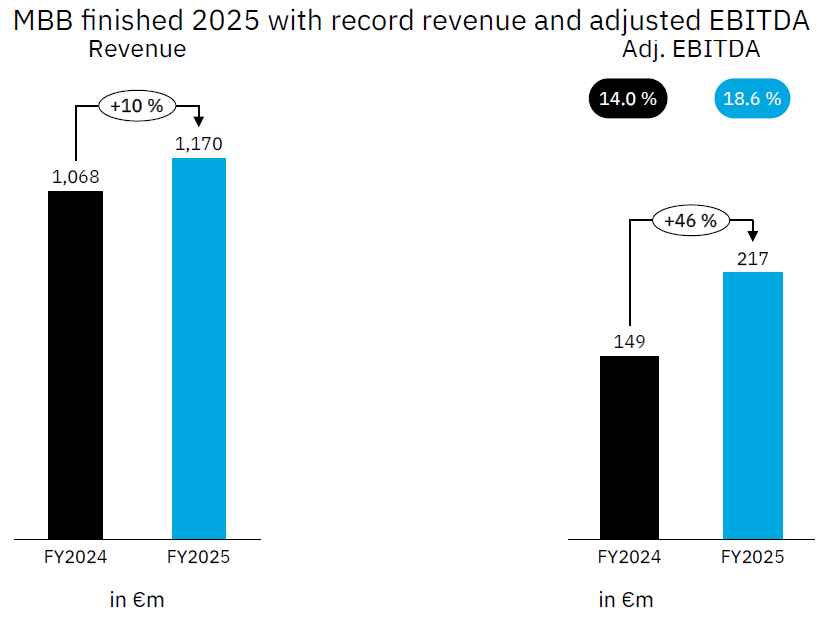

The German investment holding company MBB (Frankfurt: MBB) posted record figures in 2025, both in terms of revenue and operating profit. In this article, we share the highlights from the annual results published in the annual report on March 30.

During the earnings presentation, CFO Torben Teichler emphasized the company’s unique profile as a family-owned business. MBB offers long-term solutions for succession planning at medium-sized companies. Because MBB’s founders remain major shareholders and are deeply involved in operations, they share the same DNA as the companies they acquire. Three subsidiaries have since been successfully taken public. This provides excellent access to the capital market for further growth. The strategic focus is and remains on the long term, with no intention of reselling acquired companies.

's 2025 figures Revenue rose by about 10% in 2025 to EUR 1.17 billion. Operating profit surged by an impressive 46% to EUR 217 million. This brought the operating profit margin to an equally impressive 18.6%. Founder Christof Nesemeier writes in his letter to shareholders that these figures would have been unimaginable at the time of the company’s founding in 1995 or its IPO in 2006. The fourth quarter of 2025 in particular contributed significantly to this, with an excellent operating profit margin of nearly 24%. This result was largely due to strong project execution at subsidiaries and tight and successful cost management across all companies in the portfolio.

On May 9, 2026, MBB will celebrate its 20th anniversary as a publicly traded company. Since its initial public offering, MBB has generated a staggering return of 2,200% for its shareholders. Nesemeier emphasizes that 2026 also promises to be a good year and expresses his ambition for the future:

""We intend to improve our operational performance through further acquisitions and to continue to enhance shareholder value through dividends, share buybacks, and an intensive dialogue with you, our shareholders. However, we will continue to nurture and protect our strong financial position as usual, and use it prudently only for the type of investments for which you know us."

Interview with Nesemeier

Following the release of the annual results, Christof Nesemeier gave an interview in German. The CEO provided further insight into the performance and strategic positioning of the various subsidiaries. He emphasized that the world has changed significantly since the end of 2025 due to geopolitical tensions and substantially higher energy prices. These developments are creating a striking dichotomy within the company’s portfolio.

On the one hand, the subsidiary Friedrich Vorwerk is benefiting enormously from current market conditions. The political commitment to a carbon-neutral world and the resulting need to invest in energy infrastructure are ensuring well-filled order books with highly profitable projects. Nesemeier expects this exceptional growth to continue and to remain the driving force behind MBB’s overall positive performance. In addition, Vorwerk acquired two locations from a competitor last year to specifically strengthen its workforce for large-scale projects.

To meet the continued demand from international investors and increase liquidity in Vorwerk shares, MBB strategically and carefully reduced its stake to just under 40% in the first few months of 2026.

On the other hand, subsidiaries such as Aumann are feeling the effects of inflation and the economic slowdown. Consumer uncertainty is leading to reluctance to purchase cars, which directly impacts automakers’ willingness to invest. Aumann therefore expects a significant decline in revenue, but according to Nesemeier, the company will remain profitable and has a very strong cash position. This gives Aumann the flexibility to capitalize on opportunities in a shrinking market and gain market share at the expense of financially weaker competitors.

Companies such as Hanke Tissue and CT Formpolster are also facing headwinds due to sharply rising raw material prices and energy costs. The higher production costs cannot be passed on to the end customer immediately at the same rate. Although demand for products such as toilet paper and mattresses remains stable, the delayed price adjustment is resulting in temporarily lower profitability.

Cybersecurity as a Competitive Advantage

Cybersecurity firm DTS IT operates in a market with a consistently strong underlying trend. Demand for secure IT infrastructure remains high among both government agencies and private entities. To respond effectively to the clear trend toward European alternatives to U.S. players, DTS is further expanding its portfolio of proprietary security software, partly thanks to its earlier acquisition of ISL.

Furthermore, artificial intelligence is playing an increasingly important role as a driver of growth, both by enabling internal efficiency improvements and by addressing a rapidly evolving and increasingly complex landscape of online threats to customers. Although higher costs for hardware such as memory chips are having a slight dampening effect and certain hardware projects are sometimes being pushed back to the first half of 2026, management remains particularly optimistic about future growth and the potential within this segment.

In January, we spoke at length with Christof Nesemeier about MBB. You can read our in-depth article on the topic here.

Capital Allocation and Outlook for 2026

Nesemeier emphasizes MBB’s enormous financial strength. The company has net liquidity of more than EUR 750 million within the group and also has significant borrowing capacity. Although a share buyback program worth EUR 22.2 million is currently underway, the limited liquidity of the stock itself sets limits on its scope. Since its IPO, MBB has already distributed over EUR 250 million to shareholders through dividends and share buybacks. The strong cash position enables the company to capitalize on economically challenging times by investing in acquisitions that guarantee future growth without banking restrictions.

To support further expansion, the company is currently actively seeking solid acquisition targets in the German-speaking region with an operating profit of at least EUR 5 million. In the meantime, the substantial excess cash reserves are being managed conservatively through a diversified treasury portfolio that includes EUR 150 million in bonds and equities, as well as EUR 10 million in gold.

MBB has issued a cautious forecast for the 2026 fiscal year. Management aims to maintain revenue at least at the 2025 level, with an estimate ranging between EUR 1.1 billion and EUR 1.2 billion. The expected operating margin is between 15% and 18%. This forecast may be revised upward as market visibility improves over the course of the year.

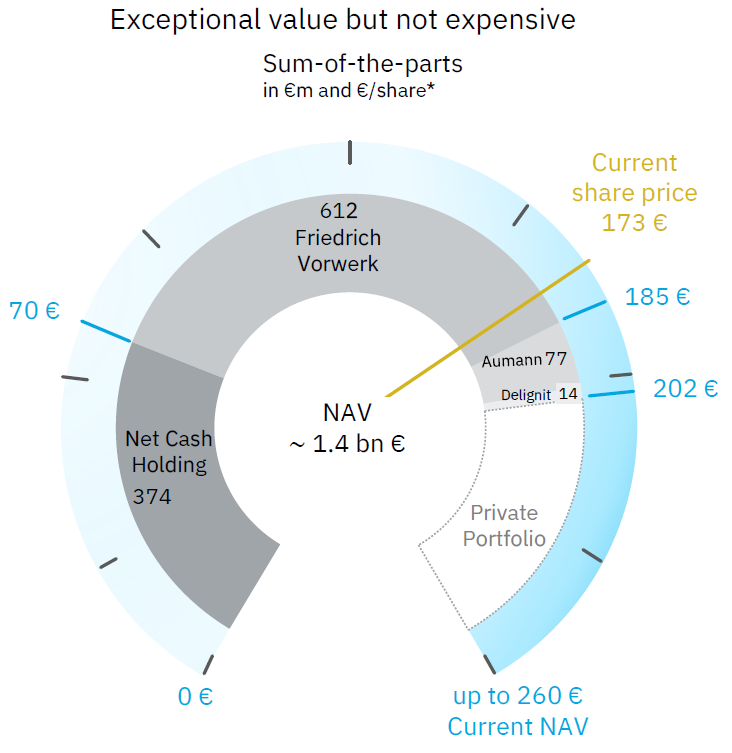

Attractively valued

CFO Teichler used the image above to calculate that the intrinsic value—based solely on the listed holdings and cash reserves within the holding company—amounts to EUR 202 per share. This calculation completely disregards the entire private portfolio of profitable companies, which underscores the upside potential relative to the current stock price.

Despite an impressive track record and various strengths, such as Vorwerk, DTS, and the flexibility of its cash position, MBB is still trading at an attractive valuation.

MBB closed the trading week on the Frankfurt Stock Exchange at a price of EUR 182.20 per share.

Receive weekly insights in your inbox

Exclusive analyses and updates on family holdings and global market developments.

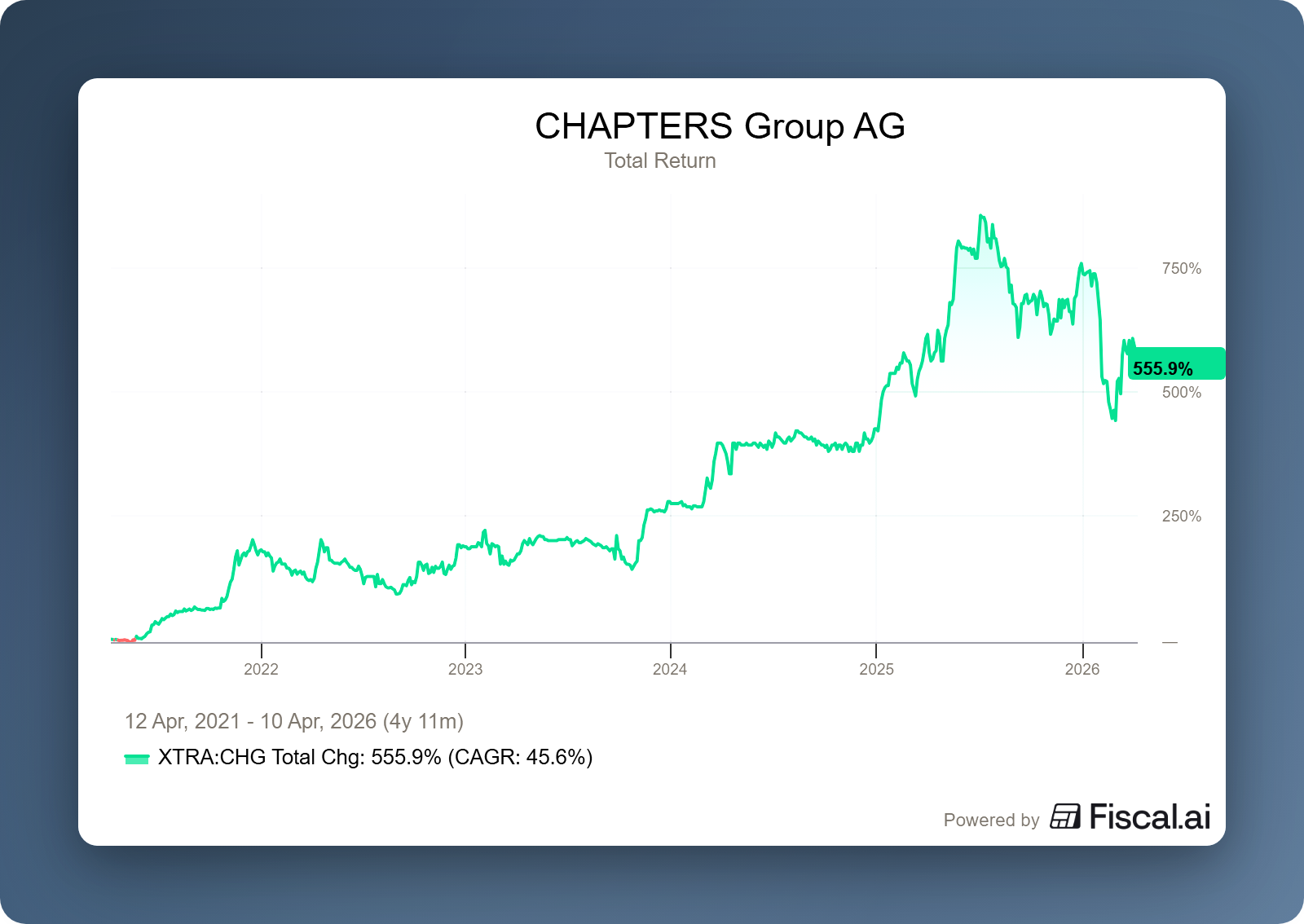

Actions speak louder than words at Chapters Group

We recently wrote at length about our initial insights from the Redeye Serial Acquirer Conference in Stockholm, where we spoke with the management team of the German VMS specialist Chapters Group (Frankfurt: CHG). That meeting made it abundantly clear that Chapters is aggressively preparing for the future. While many industry peers are still hesitating or remaining defensive, Chapters is going on the offensive to become and remain AI-ready.

Read our recent, in-depth report on Chapters Group here.

This week, that forward-thinking approach was reaffirmed with the announcement of a new venture called Altamount Ignite. This new division will be part of the Altamount Software acquisition platform and will serve as the technological catalyst for the entire group. The goal of Altamount Ignite is:

"To drive AI applications and innovation within the operating companies of Altamount and Chapters. This will make these companies more agile, faster, and more innovative, enabling them to deliver sustainable value to customers through advanced technological solutions."

This division will most likely serve as the connecting link for the Chapters Momentum initiative, which was successfully launched earlier this year to develop concrete AI products within the portfolio companies. The new division will be led by Lennart May, who brings a wealth of experience from Lufthansa, where he managed a large team for many years. It is noteworthy, however, that he does not have a specific technical or AI background.

In addition to its strategic expansion, Chapters is also securing the necessary financial resources. The company announced that it will draw down a portion of the remaining EUR 28 million from its 2025 bond issue. This fresh capital provides the flexibility to both accelerate its AI expansion and pursue new acquisitions that meet its stricter, "AI-proof" investment criteria.

Chapters Group closed the trading week on the Frankfurt Stock Exchange at a price of EUR 31.35 per share.

Receive weekly insights in your inbox

Exclusive analyses and updates on family holdings and global market developments.

The nuances of private credit are sometimes hard to find

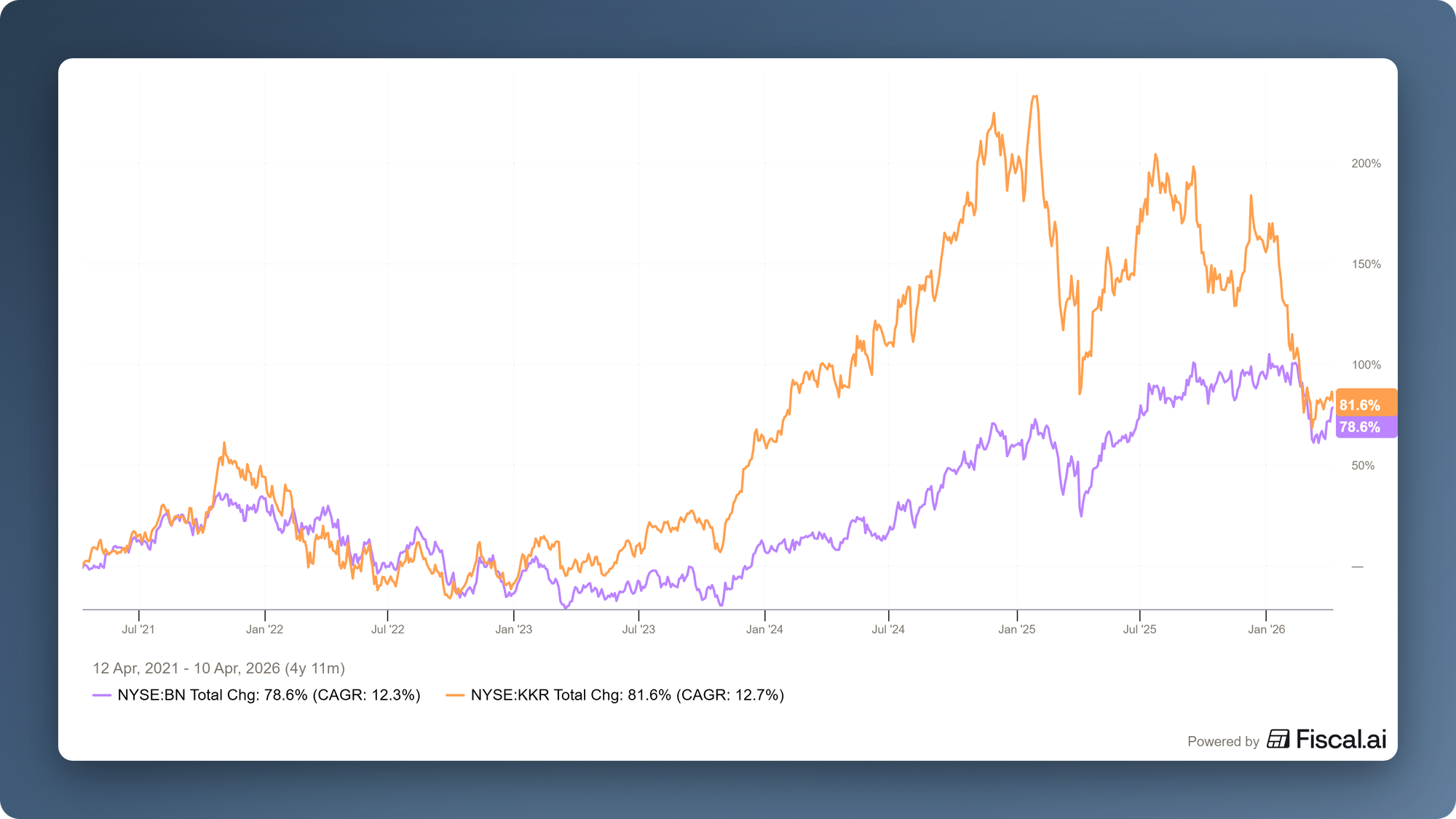

There has been a lot of buzz surrounding private credit in recent months. Investment holding companies with exposure to private markets, such as Brookfield Corporation (New York: BN) and KKR (New York: KKR), are being swept up in this turmoil. We covered these two companies last week; you can read that article below:

Newspaper headlines often make a big deal out of it when private credit funds stick to the clearly agreed-upon withdrawal limit of 5% per quarter. Commentators sometimes add fuel to the fire. That’s why it’s not a bad idea to take a step back every now and then and put things into perspective.

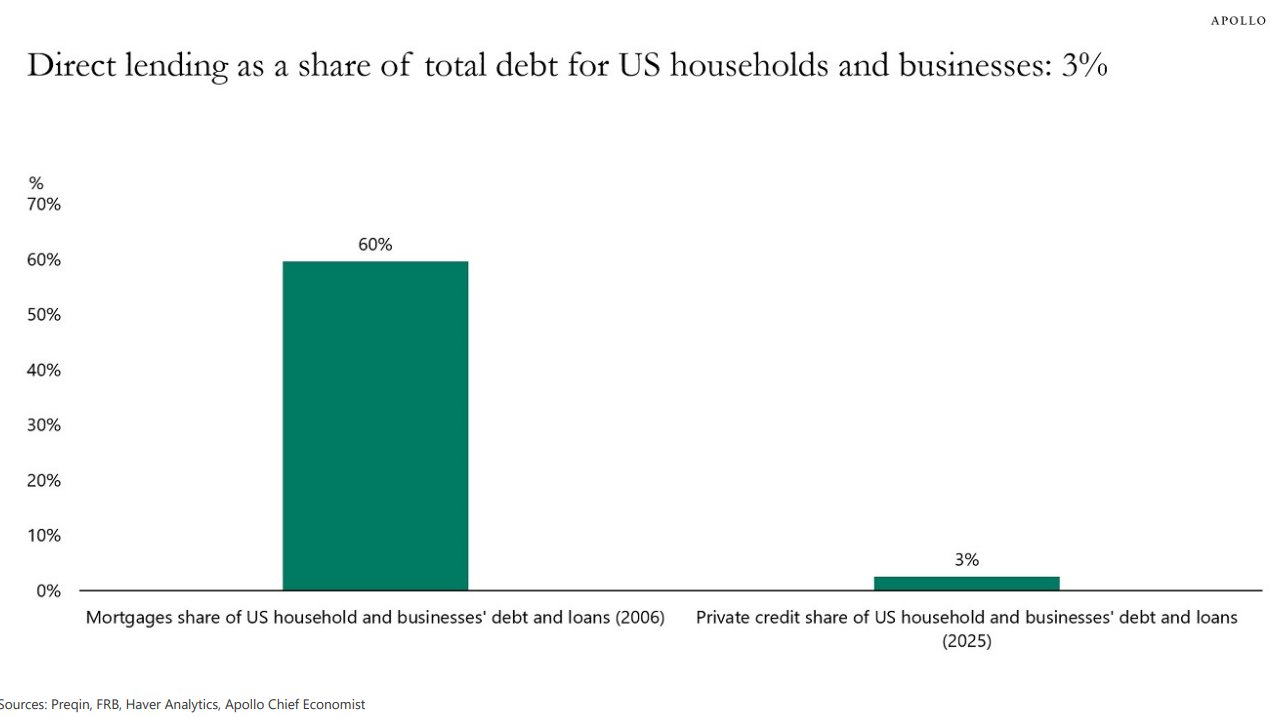

As we previously noted, Brookfield and KKR’s exposure is, on the whole, fairly limited. There is certainly no question of a so-called systemic risk, as some would have us believe. Torsten Slok, chief economist at Apollo, shared the image below this week. Private credit accounts for 3% of total debt held by U.S. households and businesses. By comparison, mortgages accounted for 60% in 2006, just before the credit crisis at the peak of the housing bubble.

In a detailed article (available via the link below), Blackstone debunks common myths about private credit (private loans) and emphasizes that the current market is fundamentally different from the 2008 financial crisis. Unlike the heavily indebted banks of that time, today’s lenders (such as BDCs) operate with much lower leverage and are highly regulated and transparent. They are subject to strict oversight by the U.S. SEC, utilize independent audits, and publish clear, up-to-date valuations, making the market significantly safer and more transparent than critics often claim.

In addition, the report dispels fears of a collapse in credit quality and a specific crisis in the software sector. Companies receiving loans are actually posting resilient earnings figures, and the loans are protected by substantial equity buffers (averaging around 60%), which limits the risk of significant losses in the event of default. Finally, it is emphasized that these investment products, thanks in part to a semi-liquid structure that protects against forced sales during market turmoil, are an effective and reliable tool for wealth accumulation not only for institutions but also for individual investors.

"Show me the incentive, and I'll show you the outcome."

- Charlie Munger

To put this into perspective, it is worth noting that both Apollo and Blackstone have exposure to the private credit market. They are therefore not independent parties; please keep this in mind as you read this article. However, the same applies to people like JP Morgan CEO Jamie Dimon, who warns of “cockroaches” and skeletons in the closet when it comes to private credit. He has every interest in warning about the risks of private credit, because as a financier, he wants nothing more than to regain market share from such parties.

As always, we continue to take a nuanced view of the actual exposure, and we see that investors have already priced in a great deal of bad news in the stock prices. Whether the end of this is in sight remains uncertain. But if things turn out to be not as bad as they currently seem, then—as has often been the case in the past—we can look forward to a strong recovery for these companies. In the meantime, however, headlines continue to influence stock prices.

Brookfield Corporation and KKR are currently trading on the New York Stock Exchange at USD 42.11 and USD 90.89 per share.

Why "Mr. No" wholeheartedly said "yes" to Action this time

Following our earlier analysis of the annual results during the Capital Markets Seminar—which focused on Action’s impressive role as a growth engine for 3i Group (London: III)—two fascinating articles have recently been published that offer a unique glimpse into the boardroom of this discount giant.

The move to the United States, scheduled for 2027, is viewed by many with healthy skepticism given the failed ventures of other European retailers. CEO Simon Borrows, who is known within 3i’s investment committee by the nickname “Mr. No” due to his critical eye, has nevertheless given his full endorsement to this project.

"My nickname on the 3i Investment Committee is Mr. No, but I believe that, in this case, the U.S. will eventually become a very significant growth opportunity for Action."

This conviction is shared by top executive Hajir Hajji. In an interview with *De Volkskrant*, she emphasizes that Action’s concept of fourteen non-food categories at rock-bottom prices simply doesn’t exist in the U.S. yet. Her motivation is rooted in an unshakable confidence in her own business model. "What we offer our European customers, I want them to have in America too," says Hajji. "Besides, I visit quite a few countries where I think: wow, everything is so terribly expensive. I would love for people to have an Action."

Despite geopolitical turmoil and logistical challenges, management remains steadfast. They are deliberately taking the time to carefully build on their success in the coming years. "We focus on what people need every day. We purchase these items in very large volumes and always ensure that margins are low," explains the CEO. A clear ambition has now been set for the U.S. market. "The goal is to have opened 100 stores in the United States by the end of 2030."

Hajji also wants to put an end once and for all to the stigma attached to the term “discount chain,” which is being used in a biased manner by *De Volkskrant*. In her view, this characterization does a disservice to both the company and its customers. "I really think the term 'discount chain' does a disservice to what we stand for," says the CEO. She emphatically positions Action as a serious retail chain that fulfills an important social role. "I think it’s important that we’re able to offer those low prices to people who have a little less to spend during difficult times. I take that role seriously."

In doing so, she sharply contrasts herself with the traditional retail sector. "When you see other stores selling items for seven or eight times the cost price, I think: who isn't doing things right here?" With a network of 3,300 stores and the ambition to open a new location every day starting in 2025, Action's drive for expansion seems unstoppable for the time being.

Readers with a subscription to the relevant publications can access the full articles via the links below:

- Financial Times: Why 3i’s ‘Mr. No’ Agreed to Launch the Discount Chain Action in the U.S.

- De Volkskrant: Action Goes American: “I think the term ‘discount store’ really doesn’t do justice to what we stand for”

3i Group closed the trading week on the London Stock Exchange at a price of GBP 26.91 per share.

Interview with "retired" Buffett

In his most recent interview with CNBC, Warren Buffett shows that, while he may be losing some of his physical vigor at the age of 95, mentally he is still the sharp "Oracle of Omaha" we know. Although he admits that everything takes him longer now, his passion for Berkshire Hathaway (New York: BRK.B) and the financial markets remains as strong as ever.

Since he officially stepped down as CEO on January 1 of this year, his daily routine has changed surprisingly little. He still goes to the office every day and remains closely involved in the company’s investment decisions. He works closely with his successor, Greg Abel, whom he praised highly: according to Buffett, Abel gets more work done in a single day than he did in a week during his absolute prime. Still, Buffett keeps his finger on the pulse; for instance, he calls his head of financial assets every day before the market opens to review orders and adjust limits. He even revealed that he recently made another “tiny” purchase for the investment portfolio, though he declined to say which company it was.

One of the most striking moments in the interview was his reflection on the investment in Apple. Although Berkshire made billions in profits on the stock, Buffett candidly admitted that he had reduced the position too early. He still called Apple a fantastic company—in his view, even better than many companies that Berkshire owns outright—but he added that, given the current valuation, he would not immediately buy more shares at this time.

In addition to financial figures, more serious social issues were also discussed. Buffett expressed his concerns about the geopolitical situation, particularly the threat of nuclear weapons in countries such as Iran. On the economic front, he was critical of the Federal Reserve’s current inflation policy; he personally advocates for a zero-percent inflation target instead of the current two percent, because in his view, inflation slowly but surely erodes savers’ purchasing power.

You can listen to the entire interview here:

Berkshire Hathaway is currently trading on the New York Stock Exchange at a price of $480.21 per Class B share.

Receive weekly insights in your inbox

Exclusive analyses and updates on family holdings and global market developments.

Would you like more information about our services?

Contact usDisclaimer:

No rights can be derived from this publication. This is a publication by Tresor Capital. Reproduction of this document, or parts thereof, by third parties is only permitted with written permission and with reference to the source, Tresor Capital.

This publication has been compiled with the utmost care by Tresor Capital. The information is intended in a general sense and is not tailored to your individual situation. The information should therefore expressly not be regarded as advice, an offer or a proposal to purchase or trade investment products and/or purchase investment services, nor as investment advice. The authors, Tresor Capital and/or its employees may hold positions in the securities discussed, either for their own account or for their clients.

You should carefully consider the risks before you start investing. The value of your investments may fluctuate. Past performance is no guarantee of future results. You may lose (part of) your investment. Tresor Capital accepts no liability for any inaccuracies or omissions. This information is for indicative purposes only and is subject to change.

Read the full disclaimer at tresorcapitalnieuws.nl/disclaimer .