Family Holdings #9 - Navigating a nervous market with a long-term focus

This week's topics:

Heico saw revenue rise 14% to USD 1.18 billion in the first quarter of FY2026, with earnings per share of USD 1.35 far exceeding market expectations. The intraday price drop of more than 10% was caused by lower operating cash flow due to pension payments and margin pressure in the ETG division, factors that management believes are incidental and cash-neutral in nature. With a record order book, a healthy balance sheet, and a debt ratio of 1.79x operating profit, the company remains focused on organic growth and disciplined acquisitions within the aviation and defense sector.

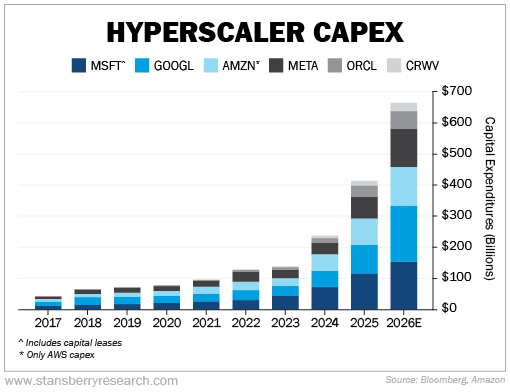

Brookfield CEO Bruce Flatt tempers fears of contagion from the private credit market by pointing to the limited size of problem sectors and the fragmented nature of this niche. Brookfield is betting heavily on AI infrastructure as the new backbone of the economy and estimates the global capital requirement for this at USD 7 trillion. To manage the risks of overcapacity, the holding company uses a model in which construction projects and the leasing of AI computing power are laid down in advance in long-term contracts with creditworthy counterparties.

Markel Group CEO Tom Gayner recently gave a rare in-depth interview to In Practise about capital allocation, the internal workings of the company, and his vision for the future. Gayner describes Markel as a company that has been deliberately built to create increasing allocation freedom over time, with Berkshire Hathaway as an explicit roadmap, but earlier in the curve. He candidly discusses the concentration in his equity portfolio, the wind-down of loss-making reinsurance operations, and recent organizational changes as early signs of a simplified and more focused Markel. You can read the full interview at the bottom of this newsletter.

In Brief:

Asseco Poland (Warsaw: ACP) founder and CEO Adam Góral has taken advantage of the recent decline in the share price to increase his stake. Through his family fund, a total of 82,500 shares were purchased on February 20 and 23 for approximately PLN 15 million (approximately €3.55 million). The purchase underscores the founder's confidence in the company's long-term prospects.

Both Sofina ( Brussels: SOF) and Scottish Mortgage Investment Trust (London: SMT) are benefiting from a sharp revaluation of ByteDance, TikTok's parent company. A proposed secondary sale by General Atlantic implies a valuation of $550 billion, well above previous transactions ($480 billion in November and $330 billion in last year's buyback). The rising private market valuation supports the intrinsic value of both investment holdings.

Sofina also remains active in the ecosystem. Brussels-based Syndicate One closed a second fund of €22 million, with Sofina as a returning anchor investor. The fund supports Belgian tech startups in their early stages and continues to build a compounding network of entrepreneurs and investors, further deepening Sofina's exposure to growth companies in Europe.

Alphabet ( New York: GOOGL) is taking further steps in the commercialization of its AI infrastructure. According to Reuters, Meta Platforms has signed a multi-year, multi-billion dollar agreement to lease Google's Tensor Processing Units (TPUs) for the development of new AI models. With this move, Google is emphatically positioning its own chips as an alternative to Nvidia, and TPU leasing is becoming an important driver within Google Cloud. In addition, robotics software company Intrinsic, which originated from Alphabet's Other Bets X division, will be fully integrated into Google. The Flowstate platform, which makes industrial robots easier to program, will collaborate more closely with Gemini and Google DeepMind.

Asseco Poland, Sofina, Scottish Mortgage Trust, and Alphabet are currently traded on the Toronto, New York, and Amsterdam stock exchanges at prices of PLN 179.50, EUR 252.60, GBP 12.40, and USD 308.12 per A share, respectively.

| Share | YTD | 3 years* | 5 years* | 10 years* |

|---|---|---|---|---|

| Asseco Poland | -21,5% | 41,5% | 28,6% | 17,9% |

| Sofina | 1,6% | 4,5% | -0,7% | 11,6% |

| Scottish Mortgage Trust | 3,8% | 21,3% | 2,0% | 16,8% |

| Alphabet | -2,1% | 45,8% | 25,8% | 23,0 |

Returns shown in EUR; *The annual compounded/compounded return

Strong Q4 for Topicus, AI leaders offer support for software

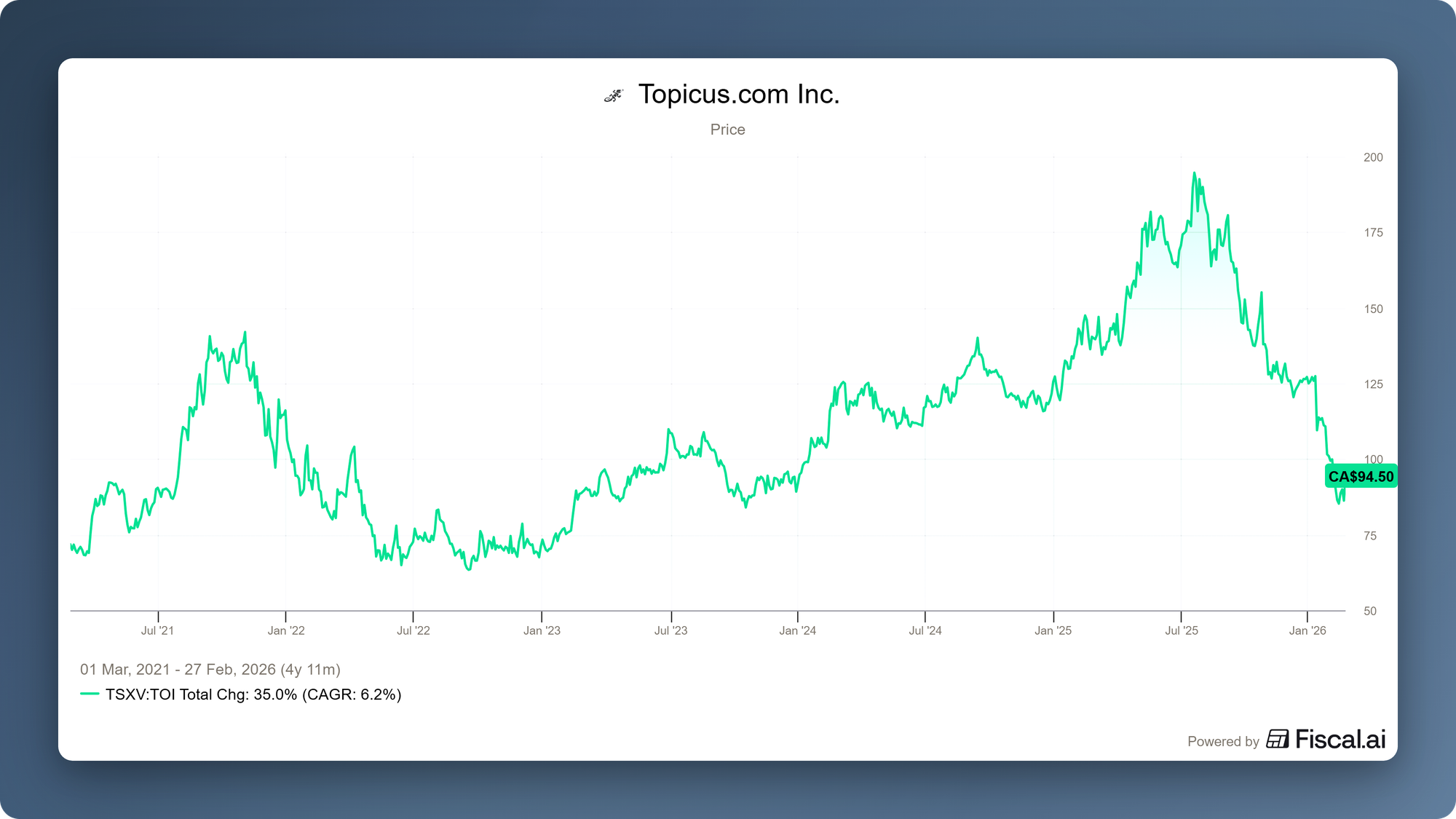

This week, Dutch investment holding company Topicus.com (Toronto: TOI) published its figures for the fourth quarter of 2025. While the share price is under pressure due to AI fears among investors, the company continues to perform at a high level in operational terms.

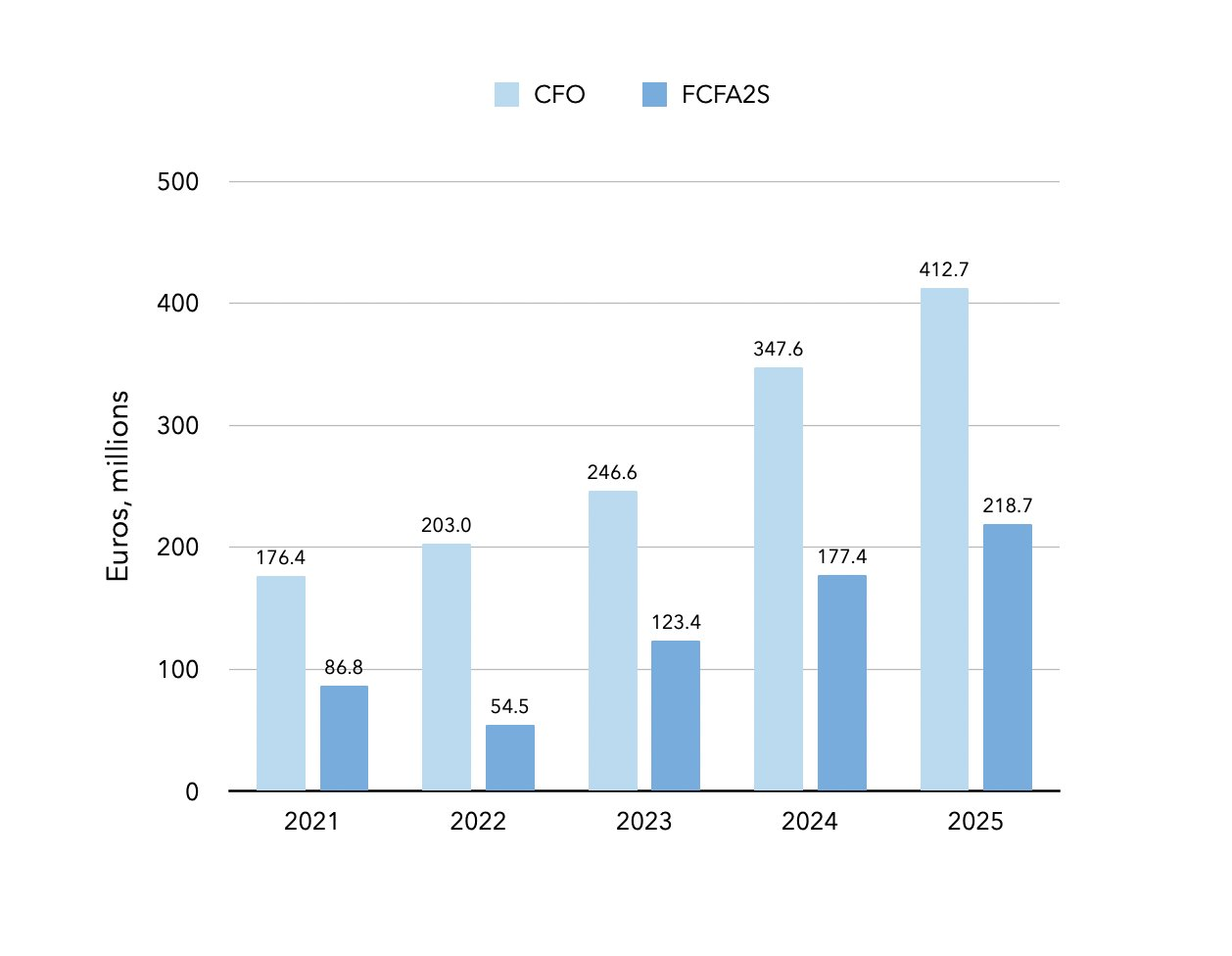

In the fourth quarter, Topicus' revenue grew by 20% to EUR 436.8 million, of which 4% was organic growth. The most important revenue component, recurring maintenance revenue, showed strong organic growth of 6%. Operating cash flow (CFO) increased by 35% to EUR 107.7 million. Free cash flow available to shareholders (FCFA2S) rose by 40% to EUR 51.2 million.

For 2025 as a whole, we can speak of an operationally excellent year. Revenue rose by 20% to EUR 1.55 billion, while operating cash flow rose by 19% to EUR 412.7 million and FCFA2S increased by 23% to EUR 218.7 million.

The figure above shows the development of cash flow from 2021 to 2025. Operating cash flow grew annually by a compound percentage of over 23%, while free cash flow, as defined above, even showed annual growth of 26%.

acquisitions While the third quarter was still somewhat modest in terms of acquisitions (EUR 19.2 million), the fourth quarter showed a clear acceleration. Topicus spent EUR 69.8 million on acquisitions in the last three months of 2025. In addition, the second tranche of the investment in Polish serial acquirer Asseco Poland was completed, involving EUR 216.9 million. In total, Topicus spent more than EUR 700 million on acquisitions in 2025, a record and a multiple of what was spent in previous years.

2026 has also gotten off to a good start, with Topicus spending another EUR 20.3 million on acquisitions in the first two months. With a debt ratio equal to approximately 1x its operating cash flow, Topicus also has sufficient firepower to make additional acquisitions. With the uncertainty surrounding software companies and valuations under pressure, this presents opportunities for an acquisition machine like Topicus.

Artificial intelligence

The company is performing well. Cash flows are growing rapidly, organic growth in recurring revenue is healthy, and it has been a good quarter in terms of acquisitions. However, the elephant in the room is investors' fear of the impact of artificial intelligence. As you will have noticed, we have devoted a lot of attention to this topic in recent weeks, including in the deep dive below.

This week , analyst Nikotes published an interesting article. He argues that the impact of AI on industry-specific software companies such as Topicus will be largely limited because their systems are deterministic and business-critical. Customers demand absolute accuracy and strict compliance with regulations for their core operational processes, and this fault tolerance is incompatible with the probabilistic nature of modern AI applications. The competitive advantage of companies such as Topicus and Constellation Software is fundamentally rooted in specific domain knowledge and significant switching costs, which make end users reluctant to trade reliable workflows for experimental solutions. Well-managed VMS platforms, on the other hand, will successfully integrate AI technology as a tool to increase their own efficiency and further consolidate their market position in a process he characterizes as software Darwinism.

Nvidia CEO Jensen Huang also weighed in on the discussion during an interview with CNBC. Huang argues that the market is misjudging the impact of AI on the software sector and that the recent price declines are unjustified. Instead of replacing existing platforms and applications, AI agents will function as users of these tools. He emphasizes that digital workers will not build new systems, but will simply use proven software such as browsers or accounting programs to perform their tasks. Because companies will deploy hundreds of thousands of AI agents alongside "biological employees" in the future, Huang believes that the total use of software licenses will actually increase significantly. Established software companies will retain their competitive advantage because their systems will continue to serve as indispensable data sources and they will develop specialized agents for their platforms themselves.

This is what the head of product at Anthropic said today in the WSJ and it makes perfect sense to me.

— Drew Cohen (@DrewCohenMoney) February 24, 2026

As I wrote before and said on The Synopsis Podcast yesterday,

the AI companies are not going to be able to create products and support teams around every single product that a… pic.twitter.com/Y7ZM3WzzvR

Another boost for software companies came from Scott White, Head of Product Management at Anthropic. He stated this week in the Wall Street Journal that platforms such as Cowork can actually help software companies deliver more value to their customers and help end users get the most out of that software. White argues that Anthropic is not a company that tries to own every workflow within every software tool, but that they try to help people get their work done. This is ironic, given that it was Anthropic's product announcements that put pressure on software companies' share prices for fear that Anthropic would replace them.

We will continue to monitor developments closely and keep you informed of developments in this area through our newsletters and customer meetings.

Topicus is currently trading on the Toronto Stock Exchange at a price of CAD 92.76 per share.

Receive weekly insights in your inbox

Exclusive analyses and updates on family holdings and global market developments.

HEICO shares criticize minor sticking points

As usual, investment holding company Heico (New York: HEI-A) opened its earnings call with a heartfelt thank you to God and to the more than 10,000 team members who keep the company's engine running day in and day out. It is a kind of ritual within the company, designed to convey a culture that is difficult to replicate and a track record that many competitors can only envy.

The figures for the first quarter of fiscal 2026 were largely in line with analysts' expectations. Revenue rose 14% to $1.18 billion, of which 10.2% was organic, a sign that growth is not solely driven by acquisitions but is broadly supported. Operating profit climbed 15% to $259.9 million, with an operating margin that remained virtually unchanged at 22.1%, despite margin pressure from the Electronic Technologies Group (ETG) division. The figures translated into earnings per share of $1.35, well above the analyst consensus of $1.27. Nevertheless, the stock plummeted by more than 10% intraday at the opening. The market saw something it didn't like.

's declining operating cash flow The first unexpected negative figure came in operating cash flow, which fell from $203 million last year to $179 million this quarter, a decline of nearly -12%. At first glance, this seems worrying, but there appeared to be a good explanation for it. CFO Carlos Macau explained that this was influenced by payments from the Leadership Compensation Plan (LCP) to a team member who has been with the company for over 40 years. He clarified that these payments are in fact cash-neutral for the company because they are fully funded through investments in life insurance policies owned by the company (this then goes through the investment cash flow). Macau also mentioned that variable bonus payments for fiscal year 2025 were significantly higher, simply because that year was exceptionally good. Management has already stated that a further payment of approximately $73 million is planned for the rest of the year, which will again reduce the reported operating cash flow, but will not affect the company's actual cash position.

The 'Perfect Storm' at the ETG division

Another concern for investors was the operating results of the Electronic Technologies Group (ETG). Although revenue grew by 12.2%, operating profit fell by 4.3%. The margin shrank by no less than 330 basis points to 19.8%. However, according to the Mendelson brothers, there was a "perfect storm" in terms of the product mix. More defense products with lower margins were delivered this quarter, while high-margin space shipments lagged behind. In addition, the aerospace market is shifting. During the Q&A, questions were asked about the shift from the traditional GEO market to the LEO market; GEO refers to large satellites at high altitudes that remain stationary at a single point (such as for TV), while LEO refers to smaller satellites in a low, fast orbit around the Earth (such as for Starlink internet).

Originally, the business was heavily focused on GEO, but we now have a stronger presence in LEO. The shift to LEO is not cheap; margins are initially lower due to high R&D costs. But we go where the customers are. We now have a very strong offering in LEO with healthy margins, although it remains a volatile business from quarter to quarter. - Eric Mendelson

Management emphasized that order books are at record levels and that such fluctuations are inherent to the niche market in which they operate.

M&A discipline in a hot market

Currently, the aerospace sector in particular finds itself in what could be described as an overheated market. More and more smaller companies are emerging that combine the words 'space' and 'AI' and thus achieve valuations in the billions before they are even profitable. Victor Mendelson acknowledged that acquisition multiples are indeed higher at present, but emphasized that HEICO is often the "buyer of choice" for family businesses that want to secure their legacy. Paying for a company without cash flow is not something HEICO will ever do, the co-CEO stressed.

"Don't compound your losses by paying insane prices."

With a debt leverage ratio of 1.79x operating profit, HEICO also has a highly flexible balance sheet to capitalize on new opportunities in its well-filled acquisition pipeline. Even increased competition in the PMA (Parts Manufacturer Approval) market, where HEICO is the market leader, does not worry the CEO. He sees the fact that other players are now also buying up PMA companies as validation:

People used to think we were crazy to get into repair and distribution. Now everyone sees the value. We have the best customer relationships in the industry, and you can't change that just like that.

Conclusion:

The drop in share price appears to be an overreaction to accounting noise surrounding the pension plan and a temporary dip in the product mix. Looking beyond the figures, we see a company that is growing organically at double-digit rates, has a healthy balance sheet, and fosters a culture that simply cannot be bought elsewhere.

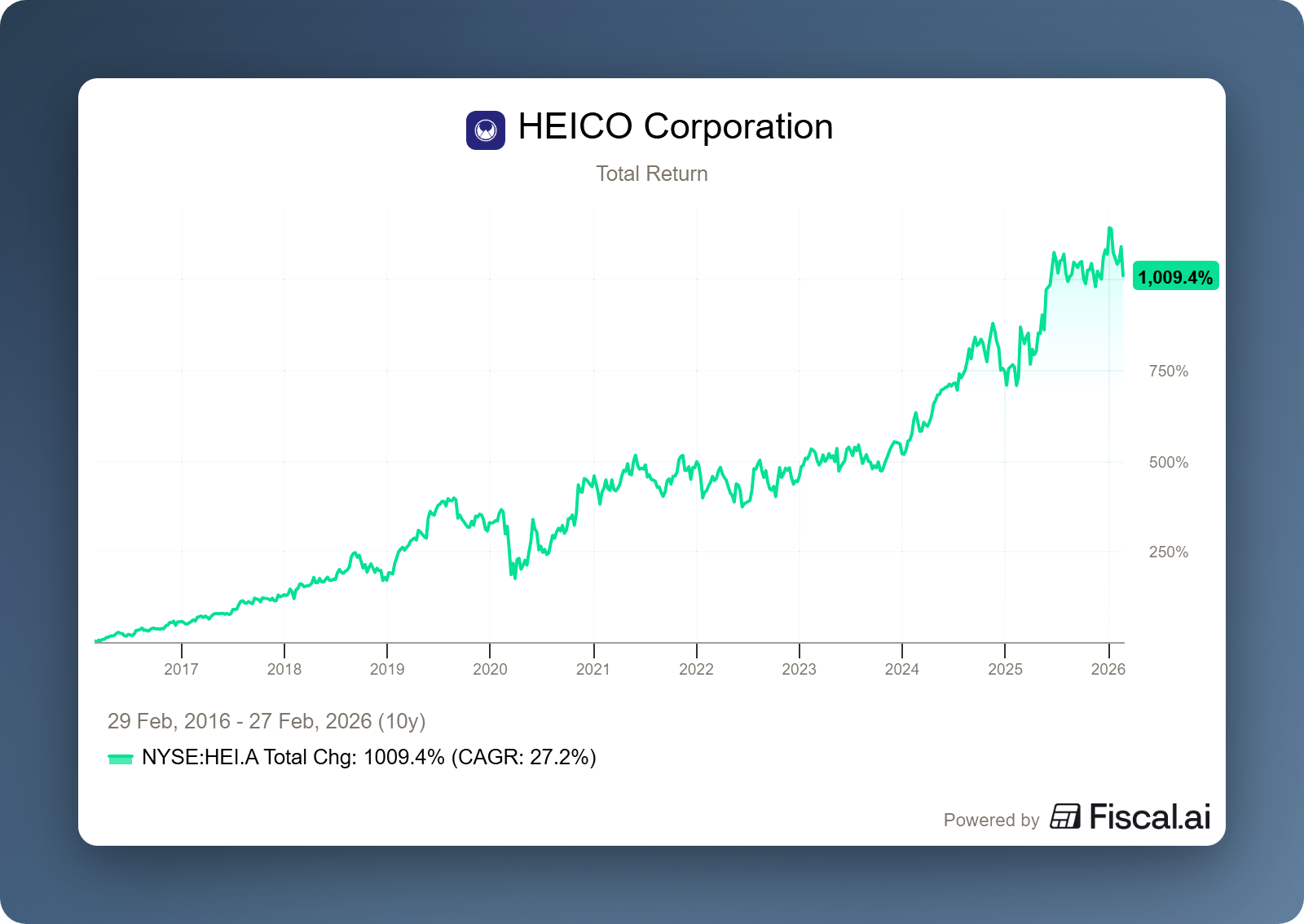

HEICO is currently trading on the New York Stock Exchange at a price of USD 243.83 per A share.

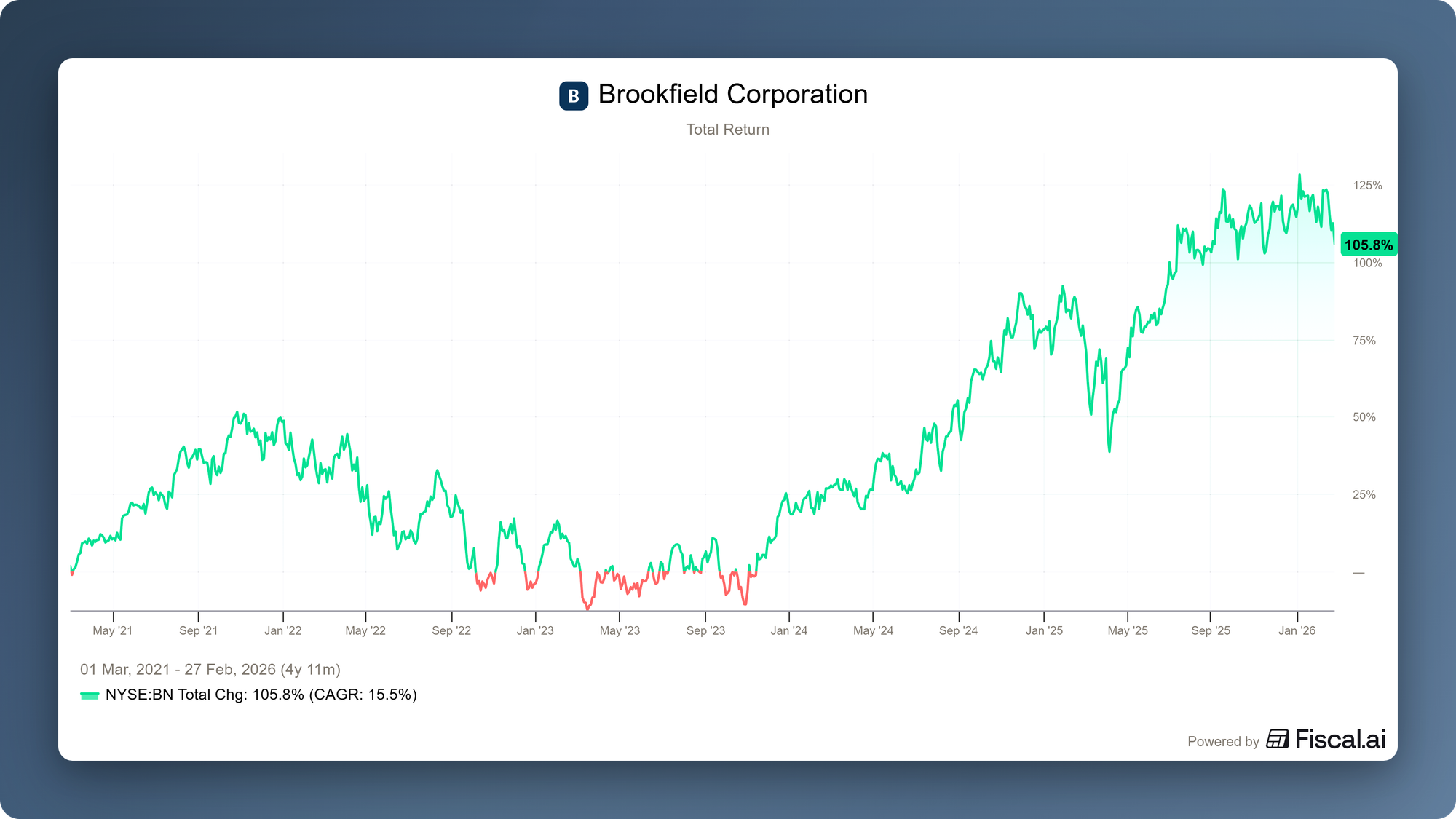

Brookfield CEO tempers private credit fears and goes all in on AI infrastructure

This week, Bruce Flatt, CEO and one of the major shareholders of Canadian investment holding company Brookfield Corporation (New York: BN), was interviewed by Bloomberg.

Private credit fears are going too far

Several bankruptcies among companies financed by private credit have made investors more uncertain about this sector in recent months. Shares in investment holding companies such as Brookfield, KKR, and Investor AB's EQT are under pressure as a result. This has recently been exacerbated by software fears, as many software companies have received financing from private credit companies. In the interview, Flatt played down the recent nervousness surrounding private credit. In his view, it represents only a small part of the global credit market. Loans to software companies constitute an even smaller segment within that market. He therefore does not see the unrest as a risk that could spread to the entire financial system.

Flatt also points out that private credit is often discussed as a single entity, whereas the market actually consists of many different niches. He does not find it surprising that some loans or valuations turn out to be overly optimistic in hindsight. In every cycle, there are periods when too much is paid or expectations are not met. This can hurt specific investors and structures, but he does not see it as a chain reaction that disrupts the credit system. In his view, the unrest is being exaggerated, partly because the news media likes to latch onto a small topic that is currently in the spotlight.

Flatt acknowledges that private credit, precisely because it is concluded outside the stock market, is sometimes perceived as opaque. According to him, this fuels the feeling that there may be "something" beneath the surface. But he emphasizes that the scale of private credit is limited compared to the total credit market, and that incidents within a niche should not automatically be interpreted as widespread contagion. He also believes that loans to companies that are coming under pressure due to technological changes are mainly individual cases, rather than a problem that is spreading throughout the entire system.

Artificial intelligence

In the interview, Flatt emphasizes the role of AI as new basic infrastructure. Brookfield focuses on financing everything needed to enable that growth, from energy and equipment to physical infrastructure. The investment amount mentioned by Brookfield is enormous. The group estimates that the development of AI will require approximately USD 7 trillion in capital investment worldwide.

Flatt puts this development into perspective. For decades, Brookfield has been building what you might call the backbone of the economy. Only its content changes over time. First, it was water networks, pipelines, and toll roads. Then came telecommunications towers, for example. Now the focus is shifting to data centers and what he calls "AI factories." Flatt argues that the economy is constantly acquiring new basic facilities and that AI is now part of that, comparable to the infrastructure that enabled previous phases of growth.

Brookfield made its AI infrastructure ambition a reality this week with the acquisition of Ori Industries, a company that provides access to AI chips as a service. Brookfield has merged Ori into Radiant, its own platform that aims to offer companies and governments computing power on demand. Brookfield approaches this as a rental model with tightly defined contracts, whereby customers continue to pay the agreed fee even if the need for chips decreases later on. In doing so, Brookfield wants to prevent returns from becoming dependent on the rate at which chips decline in value or become technologically obsolete. Radiant also focuses on so-called sovereign clouds, computing environments where data must remain within national borders, an issue that is becoming increasingly important for governments and large organizations.

Fear of overinvestment

With such an immense wave of investment, the question quickly arises as to whether too much is being built. In recent weeks, we have seen investors becoming nervous as the big technology companies announce their investment plans. Flatt makes an important distinction here with previous technology periods. In previous network investments, construction sometimes took place first, with the hope that customers would follow. The projects Brookfield is working on are different. Construction only starts once contracts have been signed in advance with a country or a company. This means that, according to him, the risk of demand falling short does not lie with the builder, but with the party that has committed to using the infrastructure.

He emphasizes that these are very strong counterparties. Countries that have these types of facilities built are highly creditworthy. The large technology companies are so big that he compares them to countries. They are looking for parties with the scale and capital to not only realize the building, but also the entire chain surrounding it, such as the connection to energy, the connections, and the interior design. According to Flatt, the bottleneck is not the demand, but the speed at which construction can take place. In his view, there is a shortage of capacity rather than a risk of overcapacity.

The three Ds: digitization, deglobalization, and decarbonization

Flatt summarizes Brookfield's long-term strategy with three themes. These are digitization, sustainability (decarbonization), and a world in which countries want to build more locally (deglobalization). He indicates that these themes have remained the same, but that their interpretation has shifted. Digitalization initially revolved around cloud facilities, but now focuses on AI facilities. Sustainability was mainly about renewable energy, but is now broader because much more electricity is simply needed. And where construction initially focused mainly on the United States, he now sees the need to set up local infrastructure in several countries at the same time.

Despite all the sensational headlines, Flatt remains remarkably calm about the bigger picture. He says that the world often thinks that now is the worst moment, fueled by all those headlines, while there have been several periods in his career that felt more difficult. Looking back in a few decades, he believes we will see that the world is progressing. And looking ahead now, we can see that developments in technology and medicine are increasing productivity and making people healthier. This fits in with the type of investments Brookfield focuses on. These are projects with a horizon of decades, not a judgment on the sentiment of the month.

Brookfield Corporation is currently trading on the New York Stock Exchange at a price of USD 44.08 per share.

Receive weekly insights in your inbox

Exclusive analyses and updates on family holdings and global market developments.

CEO Gayner considers Markel to be a younger Berkshire Hathaway.

Under the leadership of CEO Tom Gayner, Markel Group (New York: MKL) has evolved from a pure niche insurer to a diversified holding company driven by what Gayner describes as a "three-engine architecture." This structure consists of core specialty insurance operations, investments in publicly traded equities, and a growing portfolio of fully managed industrial and commercial businesses under the Markel Ventures banner.

Flexible capital allocation

The central theme within the Markel Group's vision is the deliberate design of a system aimed at creating maximum flexibility in capital allocation. "We are on the same path as Berkshire, but we are even earlier in the curve," says Gayner.

In the 1980s, Berkshire found itself in a position of extreme overcapitalization; in 1988, its book value was $3.4 billion, compared to only $600 million in insurance premiums. This meant that the ratio of premiums to capital was less than 20%, giving Berkshire the freedom to invest almost all of its assets in stocks without jeopardizing the security of policyholders. It's a scenario that Gayner Markel would love to "saddle" himself with, he jokes:

"May the Lord strike us with the curse of becoming overcapitalized as well."

The mathematical consequence of this is that the leverage of the balance sheet decreases, which opens up degrees of freedom on the asset side of the balance sheet. Where a traditional insurer is required to hold a large portion of its assets in high-quality bonds to meet future claim obligations, an overcapitalized company can shift these assets to equities and the outright acquisition of privately held companies, which offer higher expected returns over the long term.

Market Environment and Future Outlook

The Markel Group's equity portfolio, valued at approximately $12.5 billion at the end of 2025, is often misunderstood as being broadly diversified due to the 140 to 150 names in the portfolio. Gayner mentions that there is a reason for this. He argues that the changes he is seeing now, both technologically and geopolitically, are faster and more profound than anything he has experienced in his 40-year career. This reinforces his belief in the "information value" of a broad equity portfolio. By not trying to predict the future, but responding to what the market tells him through price action, he tries to avoid errors of "omission."

Despite the enormous spread in the number of companies, Gayner points out that in reality the portfolio is highly concentrated in economic terms, with two-thirds of the value concentrated in four specific "buckets."

Berkshire Hathaway: Gayner considers Berkshire to be the "new S&P 500" in the current climate. Where the actual index has increasingly become a concentrated tech bet, Berkshire offers the original promise of the S&P 500: broadly diversified exposure to the real economy (railroads, energy, manufacturing) at virtually zero cost. As the portfolio's "anchor," Markel provides stability and access to Buffett's capital allocation without requiring Gayner to hold large amounts of low-yielding cash.

The Magnificent Seven: Markel holds substantial interests in five of the seven major tech companies (Alphabet, Amazon, Apple, Microsoft, Meta), which are valued for their superior business models and returns on capital.

Large Asset Managers: Investments in companies such as JPMorgan, KKR, Apollo, Brookfield, and Blackstone. According to Gayner, these companies function as "royalty override" companies in the financial sector.

Market leaders: Companies with deep competitive moats such as Home Depot, Lowe's, Visa, and MasterCard.

According to Gayner, this equity strategy, combined with the flexible capital allocation mentioned above, is the fuel for what he describes as a "perpetual motion machine" of shareholder value.

His vision for the future, shared in the letter to shareholders published this week, rests on the foundation laid in 2025 and early 2026 by making rigorous choices, such as discontinuing reinsurance and promoting Simon Wilson (Insurance) and Andrew Crowley (Ventures) to Executive Vice Presidents to simplify the organization. Gayner describes the current improvements as the first "green shoots" of a renewed Markel. Although the company has been publicly traded for 39 years, he repeatedly states that he feels they are 'just getting started'. The ultimate ambition is to structure the organization in such a way that, regardless of technological or geopolitical headwinds, it is able to generate returns on capital across generations.

The full interview with In Practise can be accessed via the link below. It explores the following topics in greater depth:

- Lessons from mistakes: Gayner discusses how he recognizes "melting ice cubes" (companies in structural decline) and why he now values the loyalty of management teams more than purely numerical forecasts.

- Markel Ventures vs. Private Equity: Why Markel has an advantage as a "permanent home" for family businesses and how they compete without the need to resell companies after a few years.

- The psychology of the investor: How his dual role as CEO and investor has taught him that running a company is much more difficult than analyzing a spreadsheet, and how this influences his investment choices.

- Operational focus: The specific reasons behind discontinuing reinsurance activities and how the focus on insurance profits forms the basis for all their other investments.

- Internal culture: The role of the small investment team and how they use opportunity costs to choose between buying shares, acquiring companies, or purchasing Markel shares.

Markel Group is currently trading on the New York Stock Exchange at a price of USD 2,055.77 per share.

Receive weekly insights in your inbox

Exclusive analyses and updates on family holdings and global market developments.

Would you like more information about our services?

Contact usDisclaimer:

No rights can be derived from this publication. This is a publication by Tresor Capital. Reproduction of this document, or parts thereof, by third parties is only permitted with written permission and with reference to the source, Tresor Capital.

This publication has been compiled with the utmost care by Tresor Capital. The information is intended in a general sense and is not tailored to your individual situation. The information should therefore expressly not be regarded as advice, an offer or a proposal to purchase or trade investment products and/or purchase investment services, nor as investment advice. The authors, Tresor Capital and/or its employees may hold positions in the securities discussed, either for their own account or for their clients.

You should carefully consider the risks before you start investing. The value of your investments may fluctuate. Past performance is no guarantee of future results. You may lose (part of) your investment. Tresor Capital accepts no liability for any inaccuracies or omissions. This information is for indicative purposes only and is subject to change.

Read the full disclaimer at tresorcapitalnieuws.nl/disclaimer .