Economy & Markets #18 - Energy Turmoil and a Weak Yen Can't Stop the U.S. AI Rally

This week's topics:

Oil prices are nearing new records as Trump threatens new attacks

Anyone who has been following oil prices in recent weeks might have mistakenly concluded that stabilization around $90 per barrel signaled a de-escalation of the conflict. Nothing could be further from the truth. The Strait of Hormuz remains largely blocked, and strategic reserves in Asia and Europe are rapidly dwindling. It is estimated that there has been a production loss of 15 million barrels of crude oil and refined products, such as kerosene, diesel, and gasoline. This represents a significant disruption in global supply (roughly a 15% shortfall).

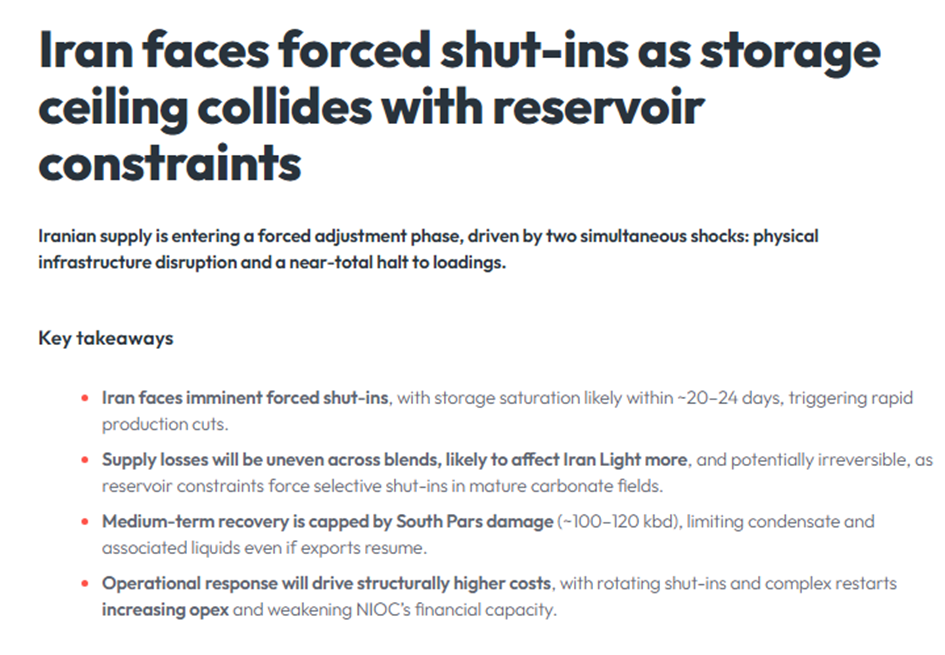

With this blockade, the United States is attempting to further increase economic pressure on Iran and halt Iranian oil exports. If Iran cannot export oil to China and/or India, nor store it domestically, there is a significant risk that this will lead to a prolonged interruption in production, causing lasting damage to Iranian oil fields. Iran has only limited storage capacity, and due to years of sanctions, it may lack the resources to shut down oil fields in a controlled manner and restart them later without significant damage. If pressure in the fields drops or saltwater intrudes, production capacity could be permanently lost.

But Trump remains impatient, and now that he is threatening to ramp up military pressure further this week, oil prices are rising rapidly once again. Moreover, the underlying market structure points to ongoing stress in the global oil system. The chart below shows that oil is still trading in backwardation: immediate delivery is priced at a premium relative to later delivery. This means the market is willing to pay extra for physical oil in the short term. Such a structure typically indicates tightness in the spot segment of the market and uncertainty about the availability of barrels in the short term.

Refining margins are rising in tandem with oil prices

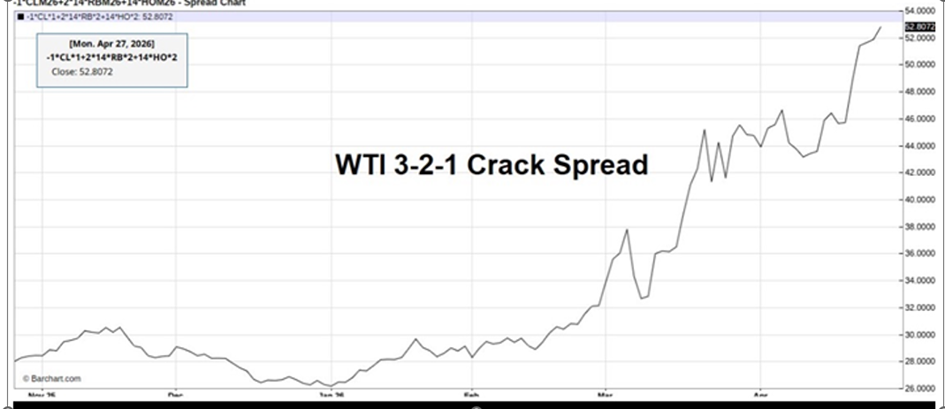

The crack spread shown below also indicates that refining margins—in this case on the U.S. Gulf Coast—have risen sharply. The U.S. Gulf Coast 3-2-1 crack spread stood at around USD 41.75 per barrel in April. While this is slightly lower than in March, it is still nearly twice as high as a year earlier. Diesel and distillate margins, in particular, remain exceptionally high, indicating a shortage of refined products. These high margins are more significant than the oil price alone. They show that market tension is not limited to crude oil but also extends to the availability of finished products such as diesel, gasoline, and kerosene. When logistics routes are under pressure, transportation costs rise, or refineries in Europe and Asia do not receive sufficient quantities of suitable crude oil, regional product shortages can arise.

At the same time, U.S. refineries in particular are benefiting from a favorable combination of factors. They have relatively good access to crude oil and natural gas from North America, with Canadian oil in particular often trading at a discount to international benchmarks. At the same time, product prices remain high and crack spreads have risen sharply. In the summer, demand for gasoline and kerosene typically increases due to the vacation season and higher mobility. Additionally, diesel markets remain vulnerable. According to the EIA, U.S. diesel margins are expected to remain at historically high levels throughout the summer, partly due to persistent international supply pressures. As a result, U.S. refineries have a competitive advantage: relatively cheap inputs on the one hand and high yields for refined products on the other. This strengthens the United States’ position not only as a major oil producer but also as an increasingly important exporter of refined oil products.

Gulf States Under Pressure, Cracks in OPEC Oil Cartel

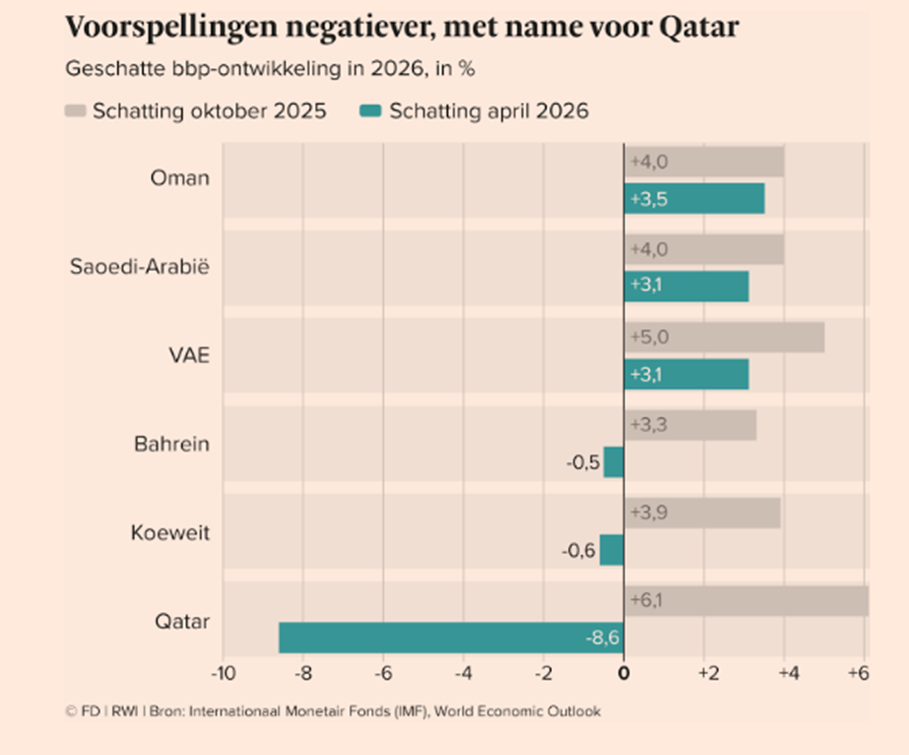

The crisis surrounding Iran and the Strait of Hormuz is hitting the Gulf States in two ways. In the short term, they are benefiting from higher oil and gas prices, but at the same time, their export routes are becoming more vulnerable. Higher transportation costs, insurance premiums, and delivery risks highlight just how dependent the region remains on safe passage through Hormuz. Countries that can export via pipelines, such as the United Arab Emirates and Saudi Arabia, and to a lesser extent Kuwait, can still export some of their oil and gas (with higher prices compensating for the disruption). Qatar, on the other hand, sees its entire gas exports disappear due to the closure of the Strait of Hormuz and damaged production facilities.

The United Arab Emirates’ withdrawal from OPEC+ is part of this broader shift. The UAE wants greater freedom to utilize its own production capacity and to be less bound by quotas that are largely dominated by Saudi Arabia. Officially, this is a strategic and economic reorientation, but at its core, it is about greater autonomy in a rapidly changing oil market.

Receive weekly insights in your inbox

Exclusive analyses and updates on family holdings and global market developments.

Chinese President Xi is preparing for the summit in mid-May. Growth remains steady, but risks persist

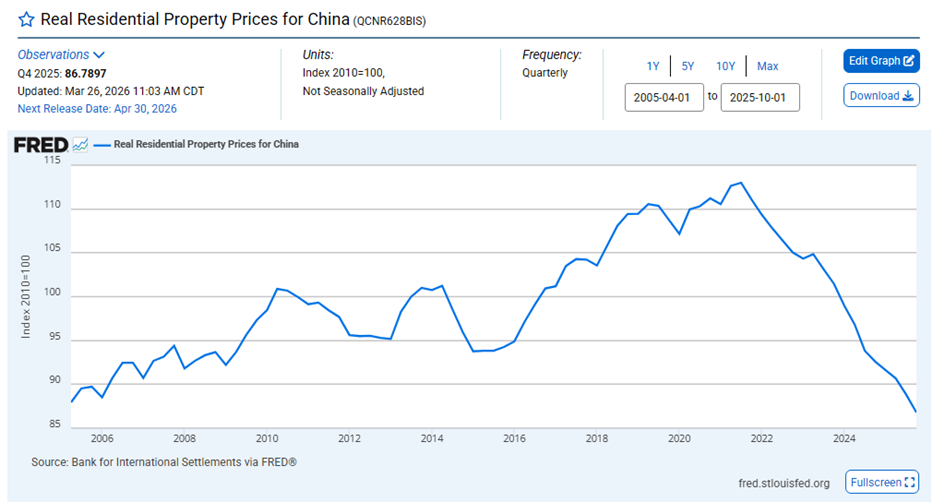

The Chinese economy is performing better than sentiment often suggests. In the first quarter, GDP grew by 5.0% year-over-year, keeping China on track with its official target (which, incidentally, comes as little surprise). The industrial sector of the economy is particularly strong: industrial production rose by 5.7% in March, while high-tech manufacturing grew by 12.5% in Q1. Underlying conditions remain mixed. Growth relies primarily on industry, exports, and policy support, while consumers remain cautious. Retail sales rose by only 1.7% year-over-year in March, and the real estate sector continues to be a clear drag. China’s inflation fell to 1.0% year-over-year in March 2026, down from 1.3% in February. That 1.3% was still the highest level in three years. Moreover, the decline was lower than the market expectation of 1.2%, pointing to persistently weak price pressure and moderate domestic demand. Housing prices (see figure) also continue to fall. For many Chinese, a (second) home is the only form of wealth (besides savings); in other words, the structural decline in prices makes a future pension highly uncertain.

The labor market also sent a worrying signal. Youth unemployment among 16- to 24-year-olds, excluding students, rose from 16.1% in February to 16.9% in March. That was the highest level since November 2025 and broke the downward trend that had been in place since September. Unemployment also rose among the 25- to 29-year-old group, again excluding students: from 7.2% to 7.7%. So despite the energy crises, inflation remains low, pointing to limited domestic demand and an economy operating at excess capacity.

Against this backdrop, Xi Jinping heads into a summit with Donald Trump in a relatively strong position, though not without vulnerabilities. The key issues are trade, technology, critical minerals, and Taiwan. China holds bargaining power through its position in supply chains and rare earths, while the U.S. maintains pressure through tariffs, chip restrictions, and sanctions. Trump is in a relatively strong position at the negotiating table. The US remains dominant in technology, capital markets, and defense, while recent conflicts have raised questions about the reliability of Chinese weapons systems in countries such as Pakistan, Venezuela, and Iran. American high-tech weapons appeared superior to their Chinese counterparts, and Trump could also choke off energy supplies to China by blocking the Strait of Hormuz.

Japan is caught between a weak yen, interest rates, and energy imports

Japan appears to have intervened again to prop up the yen. Last Thursday, the currency rose by 2.5% within minutes. Rumors suggest that over USD 70 billion in dollars were sold during the intervention, though this has not been officially confirmed.

The vulnerability is clear: Japan imports a significant amount of energy, so a weak yen makes oil, gas, and raw materials more expensive and increases inflationary pressure. At the same time, a stronger yen would require higher interest rates, but that would make it more difficult to finance the high national debt. The interest rate differential with the U.S. remains 3% higher, which is causing capital to flow from the JPY to the USD.

This puts Japan in a bind: higher interest rates set by the Bank of Japan (BOJ) support the yen but put pressure on the country’s debt; low interest rates keep the debt manageable but further weaken the currency.

AI capital expenditures under scrutiny amid concerns about OpenAI

Concerns about AI capital expenditures intensified this week following a report by The Wall Street Journal on OpenAI. According to the newspaper, OpenAI reportedly missed internal targets for revenue and user growth, even as the company commits to significant investments in data centers and computing power. This led to sharp profit-taking in AI-related stocks, including Oracle, CoreWeave, Nvidia, and SoftBank.

OpenAI refuted the negative perception and emphasized that its core business remains strong. Nevertheless, the focus of the discussion is shifting: the central issue is no longer just the demand for AI computing power, but rather who can continue to finance the massive investments in chips, cloud capacity, data centers, and electricity.

As a result, AI capital expenditures are increasingly becoming a balancing act. For AI labs such as OpenAI and Anthropic, computing power is no longer just an ordinary expense, but a strategic requirement for remaining competitive.

This also explains why, according to Techzine/Bloomberg, Anthropic is exploring a new round of funding, potentially at a valuation of $900billion, with initial plans to raise approximately $50 billion.

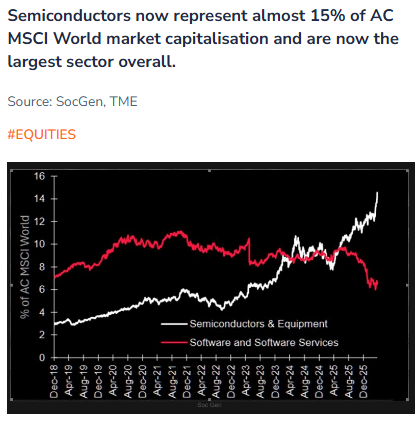

The semiconductor sector’s strong performance underscores that investors still view the AI infrastructure cycle as a structural growth story. The SOXX index is up around 50% this year, while the broader chip rally was also evident in an 18-day winning streak for the PHLX Semiconductor Index. This shifts the discussion from whether hyperscalers will continue to invest to how quickly the entire supply chain can absorb these investments.

The primary beneficiaries remain manufacturers and suppliers of AI accelerators, high-bandwidth memory, advanced packaging, networking, power management, data center cooling, and related infrastructure. As long as Meta, Alphabet, Microsoft, and Amazon continue to increase their investment budgets, demand for AI chips and related infrastructure will remain robust.

At the same time, the AI sector is expanding. The initial market reaction was concentrated mainly in chip companies such as Nvidia, Broadcom, AMD, and TSMC, but investors are now also looking at the bottlenecks beyond the chip: data center capacity (such as Oracle and Nebius), power supply (such as Caterpillar, Schneider Electric, and Bloom Energy), cooling (such as Schneider), and grid connections provided by companies like Siemens and ABB.

Hyperscaler Capex Overview All amounts are in billions of USD. Year-over-year growth is calculated based on the midpoint of the range.

| Company | 2025 Capital Expenditures | 2026 (New) | Adjustment | Year-over-Year Growth | 2027 Estimate |

|---|---|---|---|---|---|

| Meta | 72.2 | 125–145 | +10 | +86.9% | No official guidance |

| Alphabet | 91.4 | 180–190 | +5 | +102.4% | Further increase expected |

| Microsoft¹ | ~80 | ~190 | ~+45 | +137.5% | No official guidance |

| Amazon² | ~131.8 | ~200 | No change | +51.7% | No official guidance |

All amounts are in billions of USD. Year-over-year growth is calculated based on the midpoint of the range.

AI data centers can only grow if there is sufficient reliable electricity available. This is precisely where bottlenecks are increasingly occurring, because new grid connections, gas-fired power plants, and transmission infrastructure require years of planning, permitting, and construction. Due to strong demand for gas turbines from companies such as GE Vernova and Siemens, delivery times can in some cases stretch to several years, with estimates reaching up to approximately seven years.

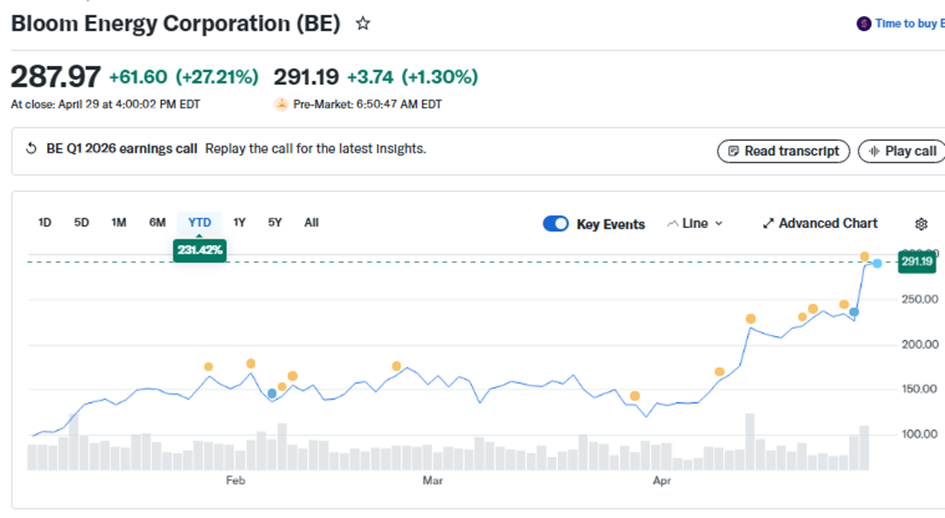

Bloom Energy is a company that stands to benefit directly from these delays. The company supplies modular fuel cells that can provide on-site power to data centers and industrial customers. In doing so, Bloom addresses one of the biggest bottlenecks in the AI infrastructure cycle: a reliable power supply. The market increasingly views Bloom as the winner of the second phase of the AI trade: not the chip itself, but the power behind the chip.

This is also reflected in the figures. Bloom reported revenue growth of 130% for the quarter and raised its revenue forecast for 2026 to USD 3.4–3.8 billion, representing approximately 80% growth. The market reaction was also strong: the stock is trading significantly higher this year and has risen sharply over the past twelve months. It is noteworthy that one of the external managers we have selected for clients holds Bloom Energy in their portfolio with a weighting of over 10%.

Powell remains a key figure at the Fed, while Warsh moves into the spotlight

Jerome Powell will remain influential within the Fed for the time being, even though his term as Fed chair ends on May 15, 2026. His separate term as a member of the Board of Governors runs until January 31, 2028, meaning he will retain institutional clout even without the chairmanship.

The Fed is keeping its policy rate stable for now within the 3.50–3.75% range. Persistent inflation risks and a resilient U.S. economy make rapid rate cuts less likely. At the same time, an interest rate hike is not immediately on the horizon, as long as higher energy prices and other price pressures do not convincingly feed through to underlying inflation.

Kevin Warsh is considered Powell’s likely successor. He is seen as a candidate who may place greater emphasis on growth, the labor market, and a more clearly defined role for the Fed. This could lead to a somewhat more dovish tone over time, but does not automatically mean that interest rate cuts will follow soon. His appointment requires Senate confirmation; the Senate Banking Committee has already approved his nomination.

For now, the outlook for long-term U.S. interest rates remains less dovish. As long as the economy remains resilient and inflation risks persist, 10-year and 30-year yields could stay relatively high—around 4.4–4.5% and approximately 5%, respectively—even if the market later begins to price in further rate cuts.

Receive weekly insights in your inbox

Exclusive analyses and updates on family holdings and global market developments.

Would you like more information about our services?

Contact usDisclaimer:

No rights can be derived from this publication. This is a publication by Tresor Capital. Reproduction of this document, or parts thereof, by third parties is only permitted with written permission and with reference to the source, Tresor Capital.

This publication has been compiled with the utmost care by Tresor Capital. The information is intended in a general sense and is not tailored to your individual situation. The information should therefore expressly not be regarded as advice, an offer or a proposal to purchase or trade investment products and/or purchase investment services, nor as investment advice. The authors, Tresor Capital and/or its employees may hold positions in the securities discussed, either for their own account or for their clients.

You should carefully consider the risks before you start investing. The value of your investments may fluctuate. Past performance is no guarantee of future results. You may lose (part of) your investment. Tresor Capital accepts no liability for any inaccuracies or omissions. This information is for indicative purposes only and is subject to change.

Read the full disclaimer at tresorcapitalnieuws.nl/disclaimer .