Family Holdings #18 - Cloud Week

This week's topics:

Markel Group saw its market value drop by 7% following an apparently weak first quarter of 2026, marked by a 21% decline in premiums and paper losses on the investment portfolio. However, this contraction is the result of a strategic restructuring in which loss-making divisions (reinsurance) were divested, resulting in significantly improved underlying profitability. On top of that, activist Jana Partners is pressing for the spin-off of the Ventures division and a $2 billion share buyback.

In Brief:

Belgian company Sofina (Brussels: SOF) is seeing the value of its stake in Vinted rise sharply now that the platform has been valued at €8 billion following an $880 million secondary share sale. This transaction by investors such as EQT and Schroders Capital follows Vinted’s impressive 2025 results, in which the company reported revenue of €1.1 billion and a profit of €62 million. For Sofina, which has been on board since 2019, this milestone confirms the platform’s successful growth from a Baltic startup to a profitable European tech giant.

Martijn van der Vorm, the driving force behind the family holding company HAL Trust (Amsterdam: HAL), has passed away at the age of 67. Under his leadership spanning several decades, HAL grew from a former shipping line into a global investment empire valued at €15.5 billion. Van der Vorm was associated with HAL for over 40 years, including 21 years as chairman of the Board of Directors. He transformed the capital from the sale of the Holland-America Line (1989) into a diverse portfolio with interests in companies such as Boskalis, Coolblue, and Vopak. Thanks in part to this success, the Van der Vorm family is considered one of the wealthiest in the Netherlands, with an estimated fortune of €9.4 billion.

In a strategic update for the first quarter of 2026, Scottish Mortgage Investment Trust (London: SMT) outlined its strategy for the coming years. According to the trust, we are entering a new era of artificial intelligence, in which the greatest opportunities no longer lie solely with chip manufacturers but are shifting toward innovative software companies and private enterprises.

Constellation Software (Toronto: CSU) is further expanding its global footprint with two strategic acquisitions by its operating groups. Subsidiary Vela has acquired Australian-based Eurofield Information Systems (EIS), a specialist in medical information systems for hospitals and insurers. At the same time, the Perseus group has acquired the UK-based Starkwood Media Group, which focuses on specialized websites and inventory management systems for the automotive sector. In addition to these acquisitions, the group is taking a major step toward optimizing its internal infrastructure with the launch of CSIPay. This new, custom-built payment platform is now available to all CSI companies and offers full control over the entire process, from onboarding to payout.

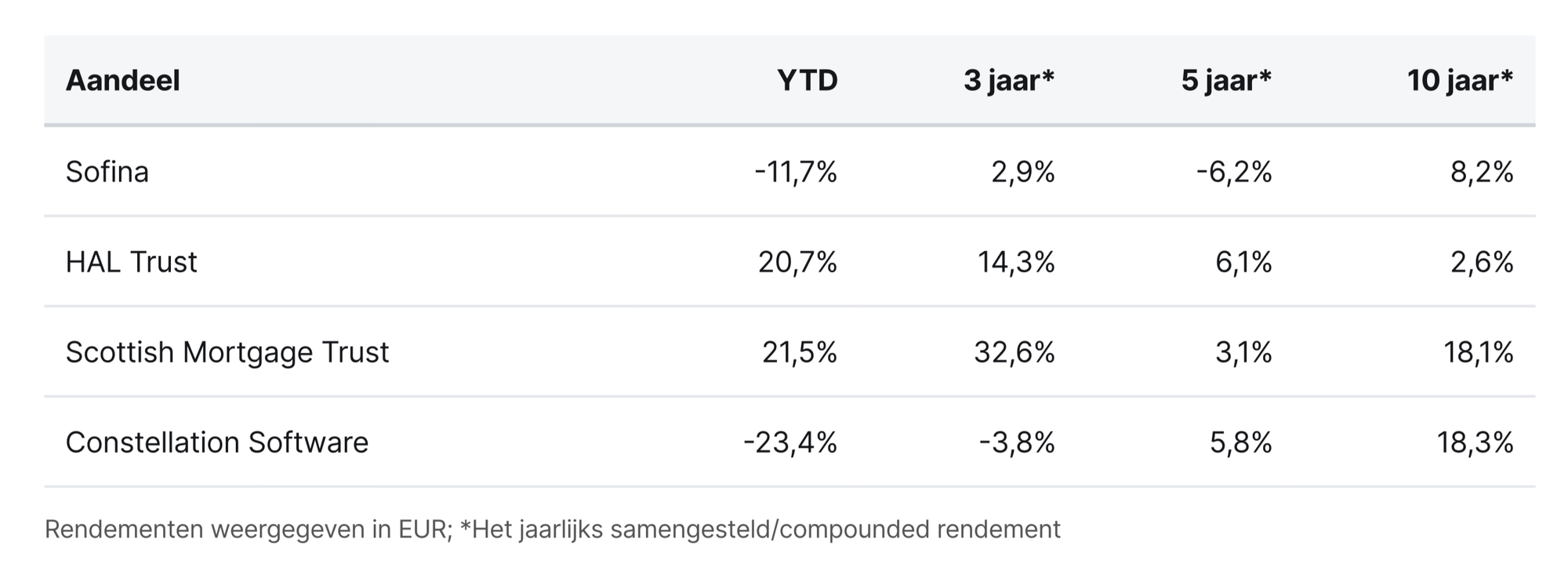

Sofina, HAL Trust, Scottish Mortgage Trust, and Constellation Software are traded on the stock exchanges in Brussels, Amsterdam, London, and Toronto at prices of EUR 218.00, EUR 170.60, GBP 14.25, and CAD 2,500.00 per share, respectively.

Google Cloud is soaring (once again) to new heights

You might not write about Alphabet (New York: GOOGL) for a few weeks, and then suddenly write about it three weeks in a row. This time, it’s not about new partnerships, but an article on the company’s recently released first-quarter 2026 earnings. The results came out on Wednesday after the market closed, just like Microsoft (New York: MSFT) and Amazon (New York: AMZN), which also reported that day, accounting for roughly 55% of the global cloud market. An important day that could either strengthen or weaken the bull case for AI.

Search is alive and well

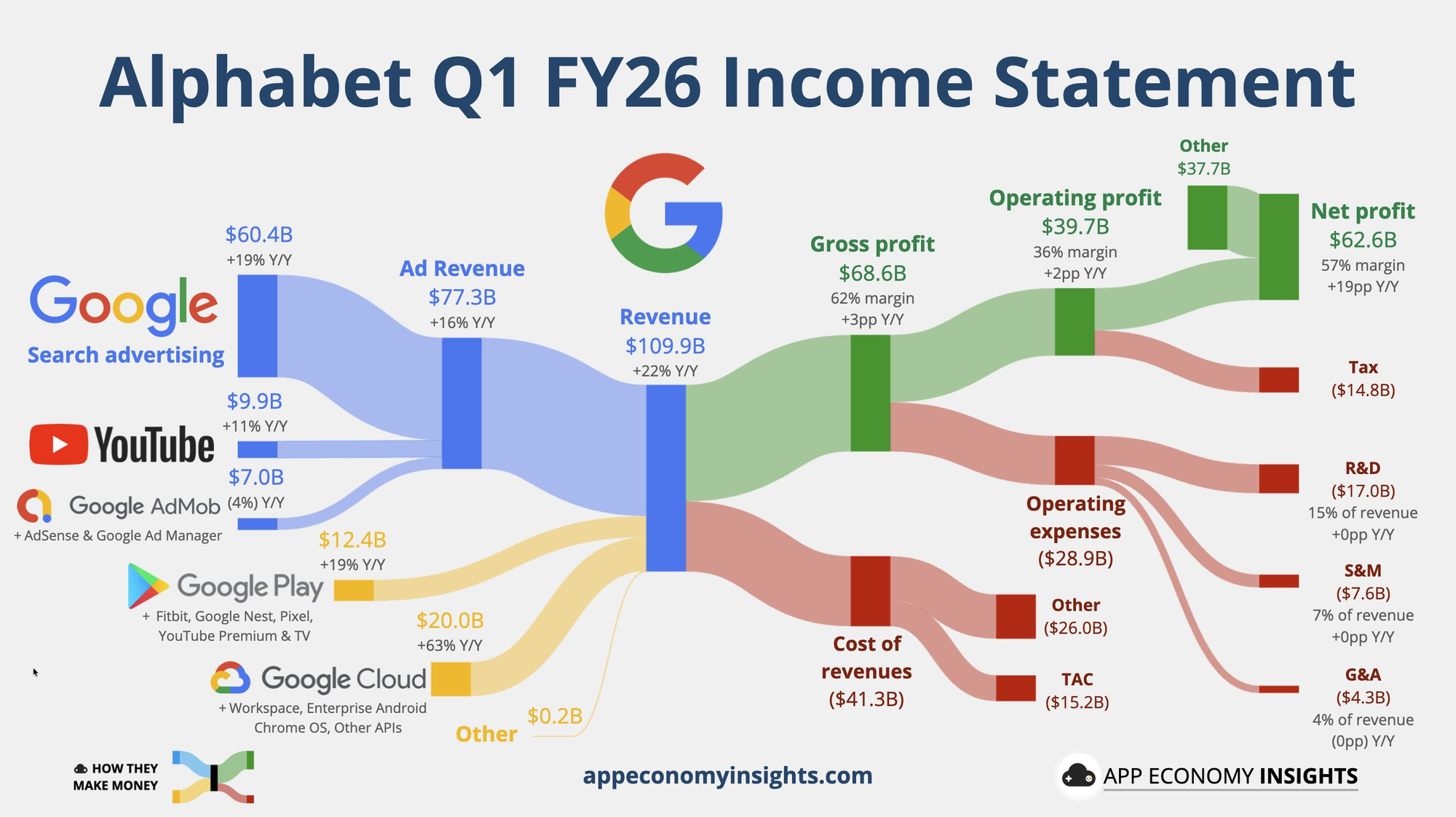

Let’s start with Alphabet’s cash flows. The image below clearly illustrates how the company performed this quarter:

The search engine, which just a year ago was predicted to be disrupted by Large Language Models (LLMs), has actually seen tremendous growth since then. Revenue from "Google Search & other" rose by 19% year-over-year to a whopping $60.4 billion. That means Search currently generates approximately $663 million in revenue per day (based on the quarterly total).

According to management, this growth is partly due to the successful rollout of AI Overviews and the new "AI Mode." Sundar Pichai emphasized during the conference call that people are returning to Search more often thanks to these AI experiences, and noted that the cost of these AI responses has now fallen by more than 30% thanks to breakthroughs in hardware and engineering.

Google Cloud

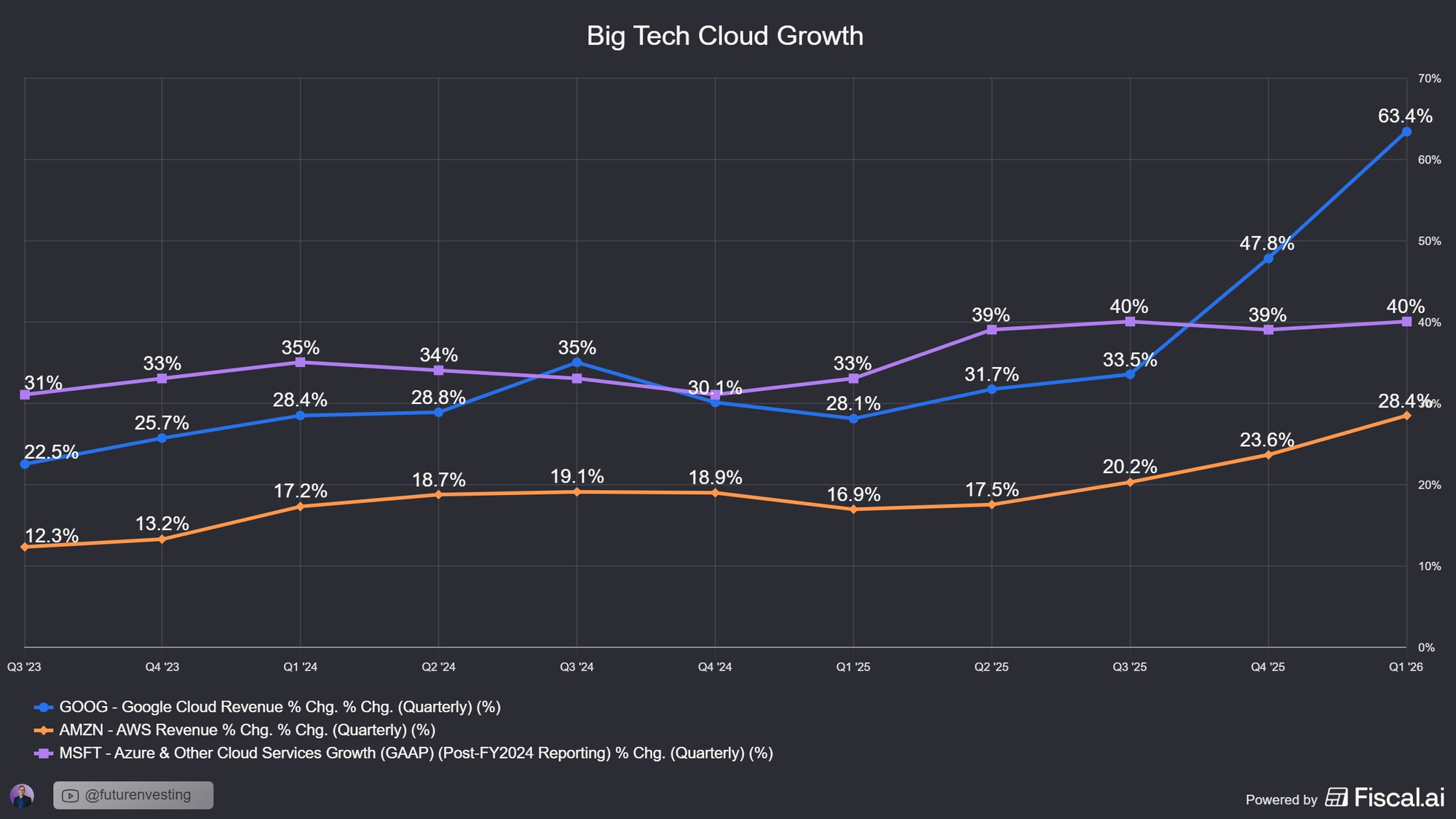

The segment that had everyone’s attention was Google Cloud. And although analysts had previously speculated that there was a 94% chance the figures would exceed expectations, Alphabet still managed to surprise the market. Cloud revenue surged by a whopping 63% to $20.0 billion in the first quarter of 2026. Although Microsoft and Amazon also posted strong figures, Alphabet is now recording the highest growth rate among the three major hyperscalers for the second quarter in a row.

In part, that makes sense. Alphabet’s cloud division still has the lowest quarterly revenue of the three: Google Cloud reported $20 billion in revenue last quarter, compared to $38 billion for Amazon (AWS) and $55 billion for Microsoft. Alphabet simply has the most ground to make up. But the question is no longer whether they will close the gap with the competition, but how quickly. And if we look at the backlog, the answer is: frighteningly fast.

The total cloud backlog of the "Big 3" hyperscalers is currently approaching the astronomical figure of $1.5 trillion. These are contractually agreed-upon future revenues, and the shifts in these figures are historic:

| Hyperscaler | Cloud Backlog | Growth (YoY) |

|---|---|---|

| Azure (Microsoft) | $633 billion | +97% |

| Google Cloud (Alphabet) | $466 billion | +398% |

| AWS (Amazon) | $364 billion | +93% |

| Total combined: ~$1.46 trillion | ||

This is a massive milestone for Alphabet. Although AWS is currently nearly twice as large as Google Cloud in terms of current revenue, Google Cloud has now officially surpassed Amazon in terms of future orders (backlog). A whopping 398% year-over-year increase shows that customers overwhelmingly prefer Google Cloud for their long-term contracts. It is clear proof that companies see tremendous value and trust in Google’s AI infrastructure. CFO Anat Ashkenazi clarified that this massive increase does not stem solely from standard Google Cloud Platform (GCP) contracts.

For the first time, management provided details about the sale of their in-house TPUs (Tensor Processing Units). Alphabet is now signing major hardware deals for these proprietary AI chips.

"Although the majority of the backlog still consists of GCP contracts. Looking at the total backlog, slightly more than half of it will be converted into revenue over the next 24 months. As for TPU hardware sales, we expect a small percentage of those to be recognized as revenue later this year, with the vast majority coming in 2027."

This shift creates an entirely new revenue stream that is separate from traditional cloud subscriptions. The scale of this is significant; with an expected shipment of 4.3 million units in 2026 and a growth trajectory to over 35 million by 2028, the company is tapping into a massive market. According to Morgan Stanley, the math underscores the potential; every 500,000 units sold would already account for about $13 billion in additional revenue.

“Our cloud revenue would have been higher if we had more computing power.” - Sundar Pichai

Revaluations of SpaceX and Anthropic clearly visible

If we zoom out again to look at the overall cash flows, one line item immediately stands out in the upper right corner of the chart. The "Other Income" line item reported a profit of no less than $37.7 billion. This is the direct result of the revaluations of the stakes in SpaceX and Anthropic that we’ve written about before, and there’s still room for growth. Take Anthropic, for example. Although the last official funding round was still based on a valuation of around $380 billion—which likely still serves as the basis for a large portion of the current book value—concrete rumors leaked out last week that the company is now being valued at between $900 billion and $1 trillion.

Google just reported $62.6 BILLION in quarterly profit…

— shirish (@shiri_shh) April 30, 2026

but HALF came from a $37.7B 'paper gain' on private investments in companies like SpaceX and Anthropic.

The reason their VC funding team is top-tier https://t.co/dc6sXFqTpo pic.twitter.com/DT9pmYpGYp

This means that, following these massive paper gains of $37.7 billion, there is a good chance that the actual market value of these holdings is even higher than what currently appears on the books.

Conclusion

Despite the euphoria surrounding the growth figures, the fundamental question continues to hang over the market: to what extent do those astronomical investments actually translate one-to-one into additional growth? The initial signals from the hyperscalers are positive, but it remains impossible for now to precisely determine which portion of the revenue acceleration is directly attributable to the new AI infrastructure, and which portion is simply riding the wave of a favorable climate.

Meta was immediately punished with a 10% drop in its stock price when it increased its CAPEX by another $10 billion, and Alphabet also announced that it too would be implementing a significant increase in spending in 2027.

Although cash flows allow for it, the current AI race is not being financed solely with internal reserves. At Alphabet, we see that the drive to invest currently outweighs the need for immediate cost control. A significant portion of these investments is covered by debt, which is clearly visible on the balance sheet. Long-term debt has skyrocketed from $46.5 billion to $77.5 billion, an increase of no less than 66.5%.

Alphabet may currently be the top-performing player in the AI sector, but the pressure to turn these debts and expenses into sustainable profitability is greater than ever.

Alphabet is currently trading on the New York Stock Exchange at a price of USD 384.96 per Class A share.

Receive weekly insights in your inbox

Exclusive analyses and updates on family holdings and global market developments.

Markel's quarter wasn't a walk in the park

Markel Group (NYSE: MKL) reported its first-quarter 2026 results this week. The stock fell by more than 7% in the days that followed. At first glance, that seems like a harsh reaction to a quarter in which the combined ratio actually improved. But if you look beyond that single figure, you can see what is worrying the market: premium income is falling sharply, rates in key market segments are under pressure, and growth must come primarily from the international division—a division about which management itself has stated that current growth is unsustainable.

On top of that, news broke this week that activist investor Jana Partners has reignited its campaign against Markel, calling for the spin-off of Markel Ventures and a $2 billion share buyback.

Insurance The 21% drop in premium income sounds alarming, but there is a simple explanation. Last year, Markel made two major decisions that are now reflected in the figures. First, the company completely phased out its reinsurance division—a division that underwrote risks for other insurers and had been operating at a loss for years. Second, the partnership with Hagerty (an insurer for classic cars) has been restructured: whereas Markel used to bear the risk itself, it now only makes its license available for a fee and transfers the risk. Together, these two decisions account for $774 million of this quarter’s premium income.

Adjusting for that, premium income grows by 10%. That is still more moderate than in previous quarters, and it has everything to do with the state of the insurance market.

An insurance cycle works as follows: when there have been few major claims, new capital flows into the market, insurers compete more fiercely for policies, and rates fall. That is exactly what is happening now, particularly in property insurance. CFO Brian Costanzo noted that the actual figures for property insurance show that rates are currently falling by about 8%–9%. In liability insurance (where the insurance covers losses suffered by a customer or third party), rate increases are still occurring, but they are becoming smaller, while the cost of claims continues to rise just as rapidly.

Insurance CEO Simon Wilson was candid about this during the earnings call. He sees new, smaller insurers entering the market with private capital and aggressively competing on price in segments that have led to significant losses in the past.

"I'll say this, and I can't tell you how much I mean it: we will not follow a falling market, and we will not lose our discipline in that regard."

In practice, this means that Markel lets go of clients and policies if the price it receives is not right. This reduces premium income but protects profitability. For example, in the U.S. liability market, Markel has reduced the average insured amounts per policy by more than 20%, and has reduced its exposure to the construction sector from nearly half to less than 20% of that portfolio.

| Division | Premium Q1 2026 | Change | Combined Ratio |

|---|---|---|---|

| International | $861 million | +28% | 90% |

| Wholesale & Specialty | $673 million | -9% | 93% |

| Programs & Solutions | $656 million | -19%* | 91% |

| * Programs & Solutions grew by 12% on an adjusted basis, excluding the Hagerty transition. | |||

Markel reported a combined ratio of 93% for this quarter. That represents an improvement of three full percentage points compared to the 96% recorded a year ago. And this despite the following headwinds:

- The conflict in the Middle East resulted in $35 million in claims, accounting for a 2 percentage point increase in the combined ratio.

- The reinsurance segment, which is being phased out as part of a deliberate strategy, pushed the combined ratio down by another 2 percentage points, with a standalone ratio of 114%.

If you exclude those two one-time effects, you end up with an underlying combined ratio of approximately 89%. That is a strong result, and it shows that the strategic shift Markel implemented over the past year is starting to pay off. Wilson summed it up with an old industry saying: "Top line is vanity, bottom line is sanity." Loosely translated: high premium income looks good on paper, but the true health of an insurer is reflected in its profit margin.

The international division was the standout performer of the quarter, with an impressive combined ratio of 90% and a 28% increase in premium income. These strong results were driven by expansion into new markets such as Italy, the acquisition of a specialized insurance broker, and the introduction of new policy types in the London market.

However, Wilson immediately tempered expectations by pointing out the one-time impact of projects that were launched in mid-2025 and are only now fully reflected in the financial statements. For the remainder of 2026, he anticipates growth will normalize to between 13% and 15%.

’s investment portfolio Markel invests a large portion of its assets in publicly traded stocks, a strategy similar to that of Berkshire Hathaway. The two largest holdings in the portfolio are Berkshire Hathaway itself and Brookfield, with the latter in particular weighing heavily on the portfolio following a decline of approximately 17%. Consequently, in the first quarter, the entire portfolio fell by 5.2%, slightly more than the broader stock market, which lost 4.4%. This resulted in $728 million in paper losses, which explains the reported operating loss of $273 million.

It is important to understand that these are unrealized losses. Markel has not made any significant changes. The positions are still in place, and now that the stock market has rebounded sharply in the second quarter, the portfolio is already looking much better. Tom Gayner, who as CEO also oversees investments, responded laconically to questions about this, noting that this is normal market volatility, which Markel has been dealing with for decades.

Activism as an Additional Pressure Point

Along with the release of its quarterly results, activist investor Jana Partners sent an urgent letter to the Markel Group’s board this week. In the letter, Jana reiterates its earlier call for Markel to fully divest Markel Ventures, the division that invests in private companies across various sectors such as construction and healthcare. According to the investor, the current combination of insurance activities and private investments does not deliver unique value, and as a result, the stock structurally underperforms that of competitors.

In addition to demanding a spin-off, Jana is urging the insurer to repurchase $2 billion worth of its own shares. This should be done through a large-scale buyback program that runs parallel to the requested divestiture of the ventures division. Although Jana acknowledges that the insurance division’s results have improved significantly under the new management, they argue that the persistently weak stock price is no longer attributable to that division. The stock fell by more than 4% over the past year, and Jana contends that the market has simply rejected the current hybrid business model.

During the annual Gabelli Value Investor Conference in Omaha, Tom Gayner responded directly to pressure from activist shareholder Jana Partners. In response to a question from Michael Gielkens (Tresor Capital), Gayner indicated that he is certainly willing to undertake a $2 billion share buyback if the stock price is favorable, but he drew a clear line when it came to splitting up the company. Although he acknowledged that the insurance division has underperformed in the past, he emphasized that decisive action has since been taken. Under new management, the quality of the insurance portfolio has improved significantly, laying the foundation for recovery.

The fundamental difference with Jana Partners lies in their view of Markel Ventures. While Jana regards this division as a distraction, Gayner sees it as a crucial form of diversification that generates additional cash flow to offset downturns in the company’s other business pillars. According to Gayner, Jana simply has a different investment horizon and views the situation from a perspective that is less aligned with Markel’s culture. He emphasized that entrepreneurs and families sell their businesses to Markel precisely because of the intended long-term partnership; after all, you don’t sell a family business to the first bidder who comes along. Markel therefore consciously chooses to continuously strengthen the underlying companies as an active partner rather than divesting them.

Markel Group is currently trading on the New York Stock Exchange at a price of USD 1,792.76 per share.

Receive weekly insights in your inbox

Exclusive analyses and updates on family holdings and global market developments.

Would you like more information about our services?

Contact usDisclaimer:

No rights can be derived from this publication. This is a publication by Tresor Capital. Reproduction of this document, or parts thereof, by third parties is only permitted with written permission and with reference to the source, Tresor Capital.

This publication has been compiled with the utmost care by Tresor Capital. The information is intended in a general sense and is not tailored to your individual situation. The information should therefore expressly not be regarded as advice, an offer or a proposal to purchase or trade investment products and/or purchase investment services, nor as investment advice. The authors, Tresor Capital and/or its employees may hold positions in the securities discussed, either for their own account or for their clients.

You should carefully consider the risks before you start investing. The value of your investments may fluctuate. Past performance is no guarantee of future results. You may lose (part of) your investment. Tresor Capital accepts no liability for any inaccuracies or omissions. This information is for indicative purposes only and is subject to change.

Read the full disclaimer at tresorcapitalnieuws.nl/disclaimer .