Economy & Markets #19 - "Emerging Markets" Outperform Europe; Doomsday Scenarios Off the Table.

This week's topics:

Are the stock markets in a melt-up? Are there signs of overheating?

De Tijd argues that global stock markets may be in the midst of a “melt-up”: a phase in which stock prices rise rapidly due to euphoria and FOMO (Fear Of Missing Out), rather than fundamental valuation. Technology and semiconductor stocks, in particular, are being driven higher by optimism surrounding AI. Typical signs of such a melt-up include strong price momentum, massive inflows into popular themes, rising valuations, and investors increasingly willing to ignore risks.

It is often said that those who cannot handle sharp price declines should not invest. The idea that volatility is simply part of investing is often attributed to Warren Buffett. But the reverse question is just as relevant: how should investors deal with sharp price increases?

If you find it hard to stay optimistic during a bull market, maybe the stock market isn't for you.

— J.C. Parets (@JC_ParetsX) May 6, 2026

There is an important distinction here. Rising markets, just like sharp price corrections, are not automatically irrational. Sometimes the stock market anticipates real earnings growth, technological breakthroughs, or productivity improvements. Investors such as Larry Fink, Paul Tudor Jones, Stanley Druckenmiller, and George Soros would likely emphasize that powerful trends can persist longer than rational valuation models suggest. Momentum can reinforce itself, especially when capital flows, earnings expectations, and technological narratives feed off one another.

For investors, the key is not to view every sharp rise as a bubble right away, but to recognize when enthusiasm turns into euphoria. AI could be a structural growth wave, while some stock prices may be temporarily running ahead of the curve. The key question, therefore, is not whether AI will become important, but how much future earnings growth has already been priced in. Discipline remains crucial, especially during a melt-up: go with the trend, but don’t lose sight of valuation, cash flows, and risk management.

Yardeni Remains Optimistic About the U.S.

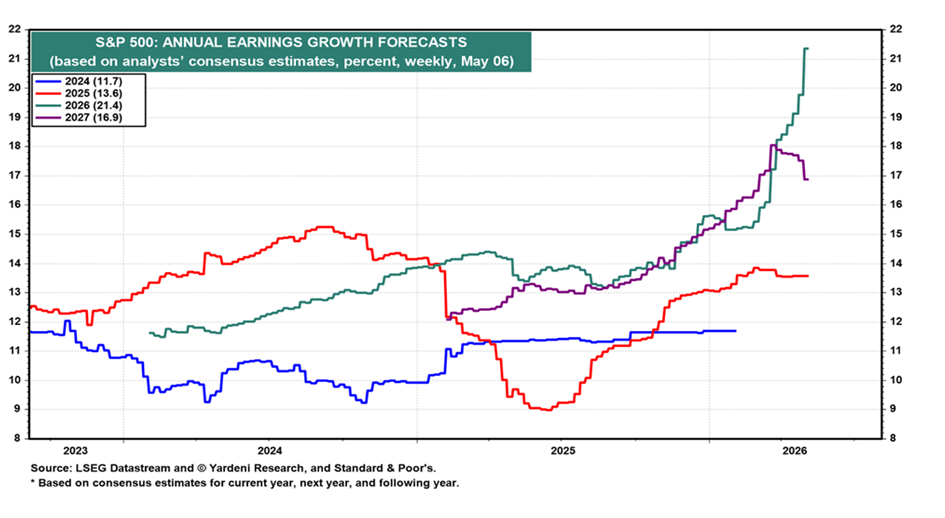

Ed Yardeni points out this week that the current rally in stock prices coincides with a sharp acceleration in earnings growth in the U.S. For this year, S&P 500 earnings are expected to grow by 21.4%, followed by 16.9% next year. Stock prices are indeed rising at an unprecedented rate, but so is earnings growth. That makes this rally fundamentally different from a purely speculative multiple expansion. In Yardeni’s charts, earnings growth tracks the Nasdaq almost one-to-one: the market is rising sharply, but underlying earnings are keeping pace almost as strongly. Incidentally, the majority of earnings growth is attributable to the Magnificent 7; excluding these names, earnings growth for S&P 500 stocks is still 14% year-over-year.

Ed Yardeni is a well-known American economist and market strategist. He built his reputation as a Wall Street economist and became best known as one of the sharpest Fed watchers. He also coined the term “bond vigilantes” in the 1980s: bond investors who discipline governments through higher interest rates when fiscal policy becomes too loose. In recent years, however, Yardeni has been particularly positive about the U.S. He speaks of the “Roaring Twenties”: a decade in which technology, productivity growth, and a strong private sector would drive the U.S. economy.

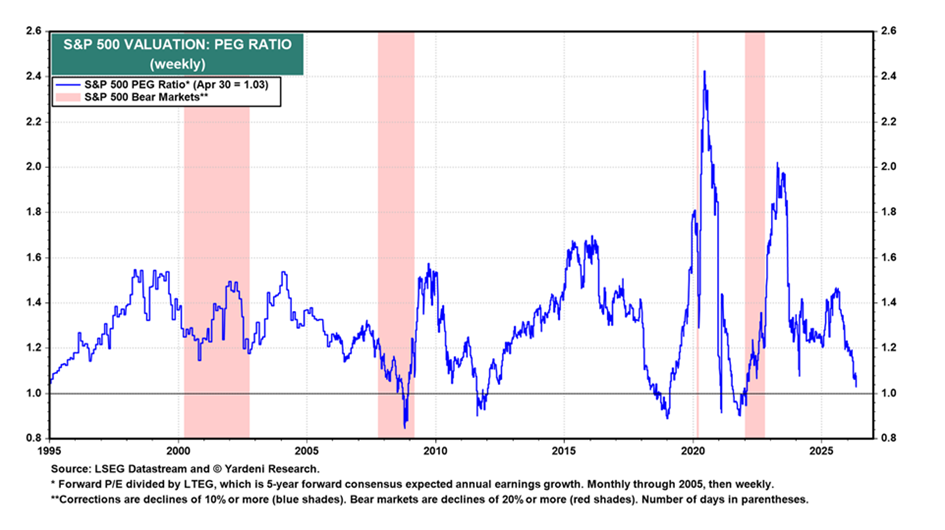

Yardeni also points out that the PEG ratio—that is, the price-to-earnings ratio divided by expected earnings growth over the next two years—is currently remarkably low, at 1.0. This stands in sharp contrast to the run-up to the dot-com crisis, when this ratio rose to 1.8.

The comparison with Europe is also relevant in this regard. At first glance, European stocks appear cheaper, as price-to-earnings ratios are generally lower than in the U.S. For example, the STOXX Europe 600 was trading at a forward P/E of approximately 15.9 in early 2026. However, this lower valuation must be weighed against significantly lower earnings growth.

Goldman Sachs forecasts 5% EPS growth for the STOXX Europe 600 in 2026 and 7% in 2027, or an average of approximately 6% per year. Yardeni, on the other hand, projects EPS growth of over 21% for the U.S. this year. When looking not only at the P/E ratio but also at expected earnings per share growth, a different picture emerges. Europe may then be less cheap than it appears, and on a PEG basis even more expensive than the US. Based on a forward P/E of 14.67 and an average expected earnings growth of approximately 6%, the indicative PEG ratio for Europe comes out at around 2.4.

In other words: while investors in Europe do pay less for each euro of current earnings, they also receive significantly less future earnings growth in return. As a result, Europe’s apparent valuation discount largely disappears once earnings growth is factored in.

The same report also notes that other sectors of the U.S. economy are running at full speed. The job market is recovering, despite fears that AI will lead to waves of layoffs, and inflation remains low. By way of comparison: the price of gasoline in the Netherlands is approximately €2.46 per liter, compared to about €1.02 per liter in the U.S. It is therefore not surprising that President Trump, as expected, is distancing himself from the Iran conflict. The U.S. economy is doing what it is supposed to do: keep running.

Korea and Taiwan demonstrate that “emerging markets” are no longer underdeveloped regions

South Korea and Taiwan demonstrate that the traditional distinction between developed and emerging markets is becoming increasingly blurred. Historically, emerging markets were primarily viewed as economies with lower incomes, greater reliance on raw materials or low-cost manufacturing, less developed capital markets, and higher political or currency risks. That description fits countries like South Korea and Taiwan less and less.

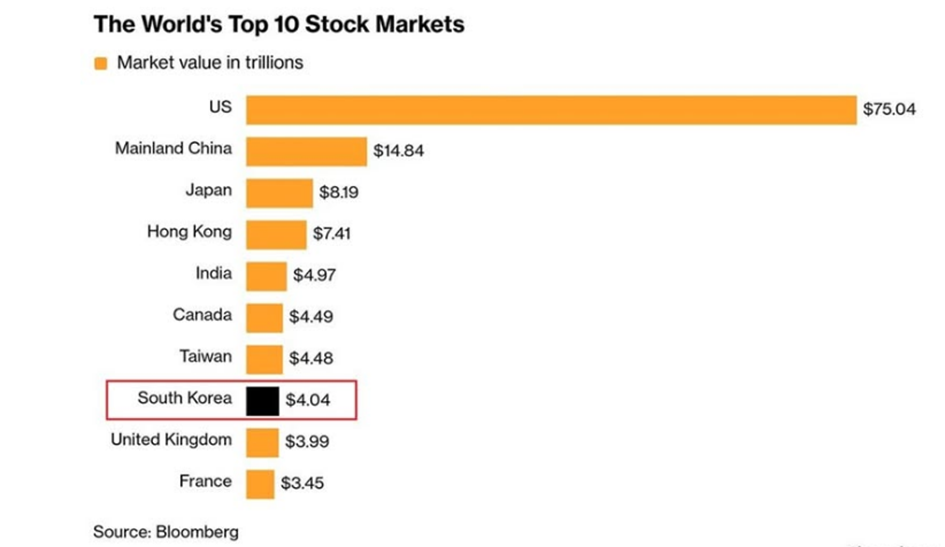

By the end of April 2026, South Korea had overtaken the United Kingdom to become the eighth-largest stock market in the world. The total market capitalization of Korean publicly traded companies rose by more than 45% this year to approximately US$4.04 trillion, while the British market grew by only about 3% to US$3.99 trillion. As recently as the end of 2024, the British stock market was roughly twice the size of South Korea’s.

This is a structural shift. South Korea and Taiwan are no longer traditional emerging markets that compete primarily on low wages, cheap production, or rapid industrialization. They are now at the heart of the world’s most strategic value chain: semiconductors, memory chips, high-bandwidth memory, and AI infrastructure. Samsung Electronics, SK Hynix, and TSMC are not regional champions, but key players in the global technology sector.

The driving force behind this shift is clear: artificial intelligence. Samsung Electronics and SK Hynix are benefiting significantly from the demand for memory chips and high-bandwidth memory for AI data centers. The KOSPI index rose by approximately 75% in 2026. Taiwan’s TAIEX index rose by about 42%, mainly thanks to TSMC and the broader AI chip supply chain.

As a result, South Korea and Taiwan are performing much better than traditional developed markets such as the United Kingdom, France, and Canada. By way of comparison, the FTSE 100 was up only about 4% to 5% year-to-date as of early May 2026, while the French CAC 40 remained largely flat to slightly positive. The Canadian S&P/TSX Composite did perform strongly on a year-to-date basis, with a rise of approximately 35%, but clearly lagged behind South Korea and Taiwan in terms of AI-driven momentum.

That is precisely why the label “emerging market” is problematic. South Korea and Taiwan are still classified as emerging markets by MSCI, even though they have long been at the forefront in economic, technological, and stock market terms. Traditional market labels are lagging behind reality in this regard. These are no longer countries that are primarily “emerging”; they are an essential part of the global AI infrastructure.

FTSE Russell has already gone a step further and classifies South Korea as a developed market. Taiwan is still considered an advanced emerging market. The difference lies mainly in market accessibility: currency, settlement, foreign registration, short selling, and other operational frictions for international investors. In other words, the discussion is increasingly less about the quality of the economy or technology, and more about how easily foreign investors can access the market.

SK Hynix is also moving in that direction. The company has initiated the process for an ADR listing in the U.S. An ADR, or American Depositary Receipt, makes it easier for international investors to invest in a foreign company through the U.S. market. This would further increase SK Hynix’s accessibility and enhance its visibility among global investors.

Falling token costs are good news for hyperscalers

In *Decoding the Agentic Economy – The Coming Inflection in AI Usage and Margins*, Goldman Sachs argues that the next phase of AI will revolve primarily around agentic AI: systems that not only provide answers, but also independently plan, execute, and adjust tasks. Think of assistants that book travel, monitor emails, write software code, or handle business processes.

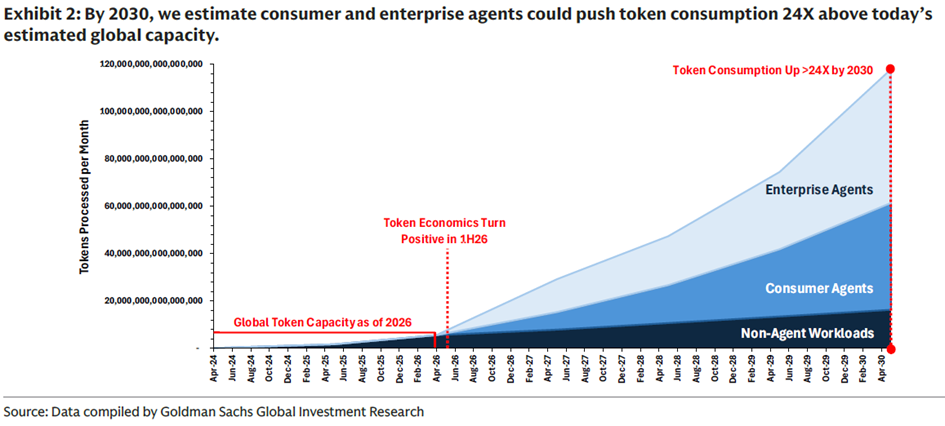

The focus is on the expected surge in token consumption. The more complex and autonomous AI tasks become, the more tokens are required. According to Goldman Sachs, global token consumption could be approximately 24 times higher by 2030 than it is today. In particular, “always-on” consumer agents and enterprise agents can drive this demand significantly, as they continuously retrieve context, validate decisions, and control multiple systems simultaneously.

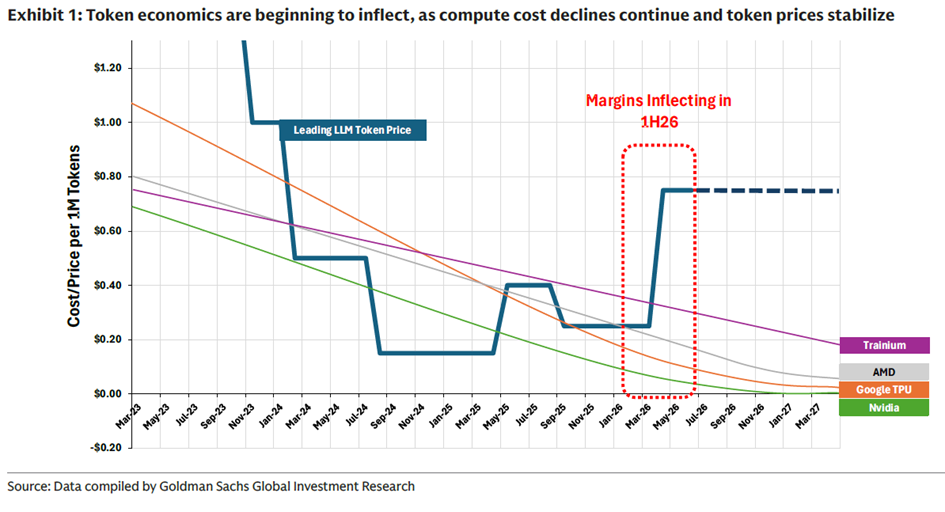

Goldman Sachs sees not only strong growth in AI adoption but also improvements in the economic aspects of AI. Costs per token are falling rapidly due to more efficient chips, better models, and higher infrastructure utilization, while token prices appear to be stabilizing. As a result, increased AI adoption can lead not only to higher revenue but also to higher margins.

For hyperscalers such as Amazon, Alphabet/Google, and Meta, this could mark a significant turning point. In the early stages of AI, increased usage was primarily viewed as a cost: more inference, more chips, more power, and higher investments in data centers. Now, that perception is beginning to shift. As token volumes rise sharply and the cost per token continues to fall, major AI investments become more economically justifiable.

In addition, AI agents can make more intensive use of existing and new infrastructure. Higher utilization rates reduce the effective cost per token and make more complex AI services more cost-effective, such as agents that run continuously in the background, automate business processes, or control multiple systems simultaneously.

Finally, scale and proprietary chips strengthen the competitive position of hyperscalers. Companies with their own infrastructure and chips—such as Google TPUs, Amazon Trainium, and Graviton—can reduce token costs more quickly than players that rely entirely on external computing power. That economies of scale can make the AI economy structurally more profitable.

Climate Scenarios: From Doomsday Scenarios to More Realistic Policies and More Efficient Capital Markets?

For years, the IPCC climate report’s RCP8.5 or SSP5-8.5 scenario played a major role in climate reports, policy, legal proceedings, and investment documentation. This scenario assumed sustained, very high fossil fuel consumption—particularly coal—and a temperature rise of approximately 4 to 6 degrees Celsius by the end of this century. For Shell, which was then a Dutch-British company, this extreme scenario meant that the court sought to impose a specific reduction target, such as a 45% reduction in CO₂ emissions by 2030.

Just this week, it was announced that this temperature trajectory should no longer be presented as a realistic “business-as-usual” projection. This clarification is important for the broader climate debate and policy. As early as 2020, climate researchers Zeke Hausfather and Glen Peters warned in *Nature* that it can be misleading to present the highest emissions scenario as the most likely outcome.

This is also relevant for investors. Many institutional portfolios, climate models, and ESG products are partly structured around this extreme climate scenario, which, in hindsight, may have been applied too extremly or too simplistically. In theory, markets should constantly reassess such assumptions. In practice, however, investors, regulators, consultants, and policymakers often follow the same dominant narratives. And they appear less inclined to revise a course once (incorrectly) set. As a result, there is a risk that climate risks are priced not only economically, but also in terms of policy or emotion.

Dutch pension funds have won numerous sustainability awards in recent years, but in recent months there has been growing criticism of their underperforming returns. For example, the ABP pension fund posted a negative investment return of -1.6% for 2025. This pales in comparison to broad market benchmarks: the MSCI World Index in euros achieved a return of +7.21% on a gross return basis in 2025, while the Bloomberg Global Aggregate Bond Index EUR Hedged came in at +2.68%. Admittedly, interest rate hedging is likely the most important factor driving returns in an environment of rising interest rates. However, active management—which includes excluding companies on sustainability grounds—has also contributed to these disappointing results.

The discussion on sustainable pension investing is thus shifting from intent to outcome. At ABP, for example, critics point out that the rapid divestment from fossil fuel investments ultimately cost returns, as oil and gas stocks actually performed strongly after the divestment decisions were made. Some commentators even speak of billions in lost returns. A similar debate is taking place regarding the exclusion of defense companies based on ESG criteria, precisely at a time when geopolitical risks and defense spending have risen sharply.

Legally, this shift could also have consequences. For governments and businesses, the diminishing weight of extreme climate scenarios provides an opportunity to scrutinize damage projections more critically. Claims that rely heavily on a 4- to 6-degree rise in temperature will need to provide stronger justification for why such a scenario remains relevant today.

This brings the key question into sharper focus: what has the use of these extreme scenarios ultimately achieved? If climate policy, ESG regulations, and investment decisions are partly based on assumptions that seem increasingly unlikely, then a reassessment is necessary. Not to downplay climate risks, but to manage them in a more realistic, economical, and effective manner. Simply shifting industrial production from Europe to China benefits no one.

Receive weekly insights in your inbox

Exclusive analyses and updates on family holdings and global market developments.

Would you like more information about our services?

Contact usDisclaimer:

No rights can be derived from this publication. This is a publication by Tresor Capital. Reproduction of this document, or parts thereof, by third parties is only permitted with written permission and with reference to the source, Tresor Capital.

This publication has been compiled with the utmost care by Tresor Capital. The information is intended in a general sense and is not tailored to your individual situation. The information should therefore expressly not be regarded as advice, an offer or a proposal to purchase or trade investment products and/or purchase investment services, nor as investment advice. The authors, Tresor Capital and/or its employees may hold positions in the securities discussed, either for their own account or for their clients.

You should carefully consider the risks before you start investing. The value of your investments may fluctuate. Past performance is no guarantee of future results. You may lose (part of) your investment. Tresor Capital accepts no liability for any inaccuracies or omissions. This information is for indicative purposes only and is subject to change.

Read the full disclaimer at tresorcapitalnieuws.nl/disclaimer .