Family Holdings #20 - Earnings season is in full swing for family holdings

This week's topics:

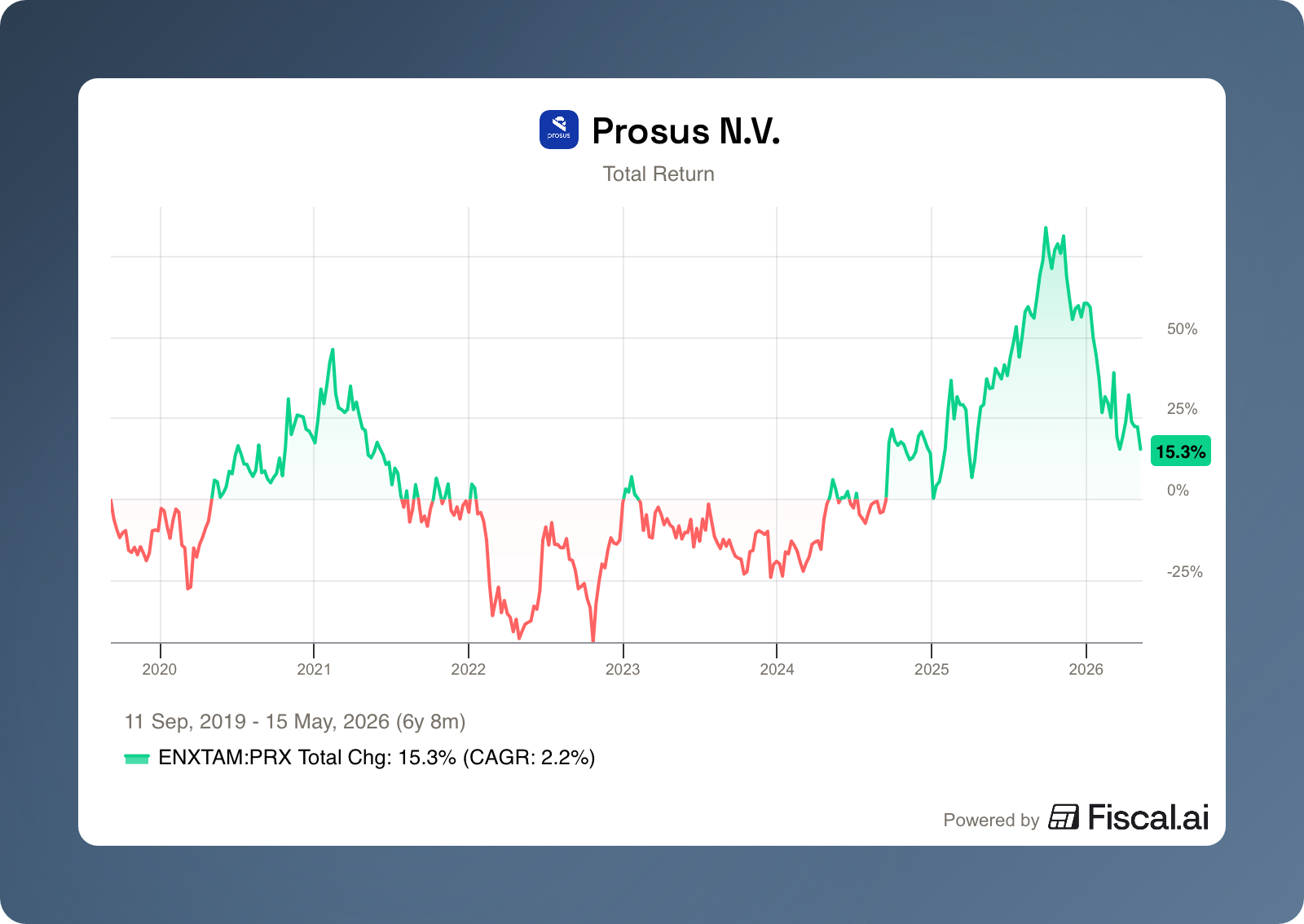

Prosus and Tencent presented updates this week that painted a mixed picture. The market reacted with disappointment to holding company Prosus, resulting in a sharp drop in its share price, despite all of its operational e-commerce units being profitable for the first time in history. The unease centers on the decision to make substantial additional investments in subsidiary iFood to fend off an offensive by competitors, and on a communication style that struck investors as reactive rather than confident. At the same time, crown jewel Tencent demonstrated its strength with a strong quarter, in which profitability grew faster than revenue and the first fruits of the AI strategy became tangible, particularly in the advertising division and through its proprietary language model Hunyuan 3.0. Furthermore, Tencent announced it would ramp up both its AI investments and its aggressive share buyback program by accelerating the sale of liquid positions from its investment portfolio, a development that works in Prosus shareholders’ favor.

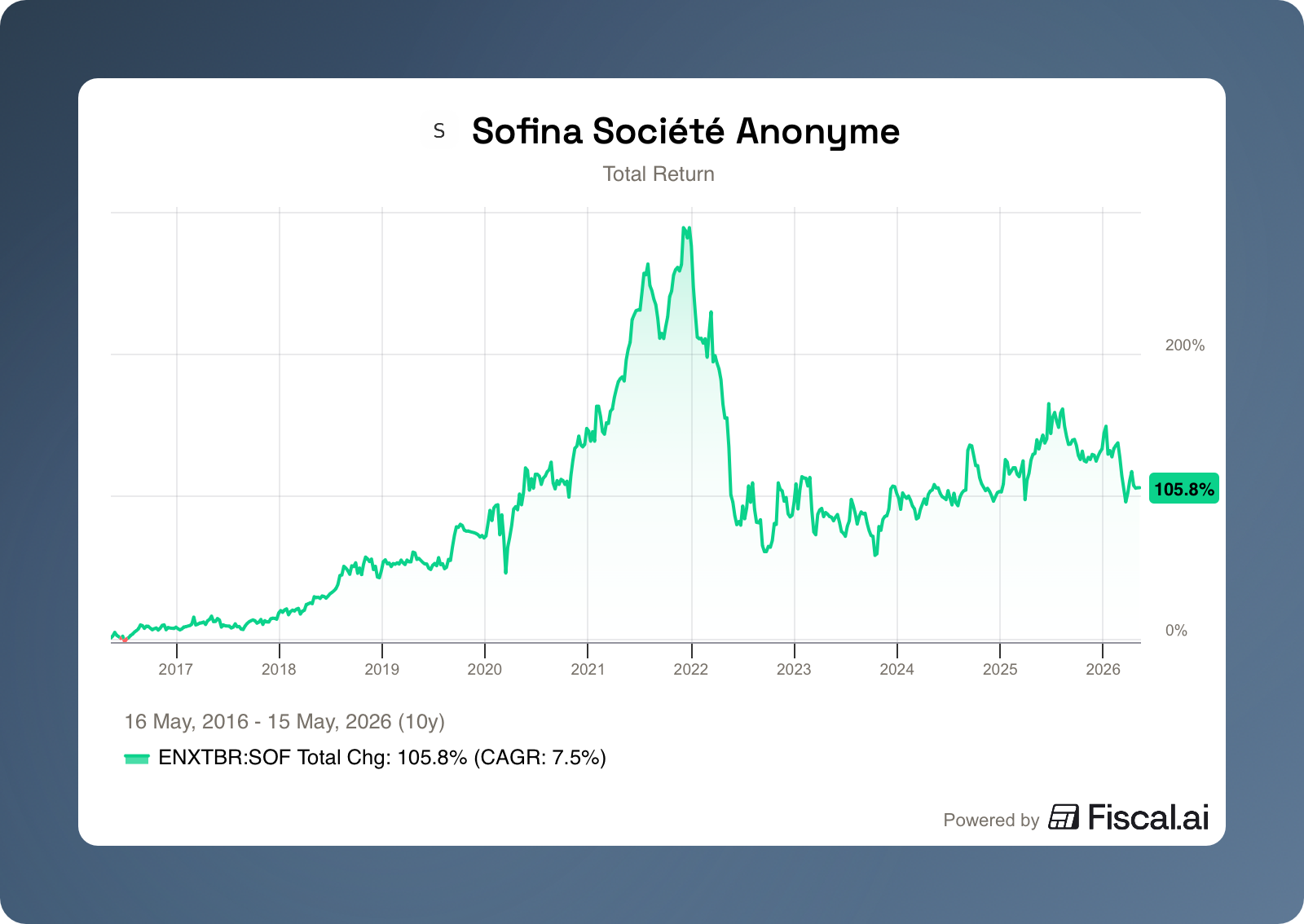

At the annual shareholders’ meeting, CEO Harold Boël painted a picture of a Sofina that, after a difficult period, has returned to calmer waters, with a normalization of investments and divestments. The net asset value per share remained virtually stable, while the stock still trades at a discount of over 30 percent. Boël emphasized that the venture capital landscape is strongly dominated by AI, with energy as a related theme, which Sofina is capitalizing on through investments in Xbow, OpenAI, and SpaceX, among others.

In Brief:

Constellation Software ( Toronto: CSU) has completed a number of acquisitions in recent weeks. Volaris, one of its operating groups, acquired two companies. Accent Technologies from Melbourne, Florida, a provider of enterprise sales enablement software for regulated sectors with clients such as DHL and Boeing, and Socoto from Trier, Germany, a marketing and campaign software company with clients such as BMW, Shell, and Husqvarna. In addition, subsidiary Vertus, part of the Jonas Group, completed an acquisition in Toronto. Magnusmode, a platform that builds accessibility tools for financial institutions and public transportation. Finally, Vela subsidiary Datamine made a strategic investment in Commit Works from Fortitude Valley (Australia), a software company that digitizes operational planning and execution for the mining industry.

Topicus ( Toronto: TOI) acquired Lighthouse Software effective May 1, 2026. The Ede-based software company is well known in the healthcare market for QuestManager, a platform that enables healthcare organizations to measure treatment outcomes and patient experience. With this acquisition, Topicus Healthcare further expands its healthcare IT portfolio.

Lifco (Stockholm: LIFCO-B) CEO Per Waldemarson purchased 15,000 shares in the company on May 12 at SEK 278.50 per share, for a total of SEK 4.2 million. This is the CEO’s second purchase of company shares in a short period of time. As of April 24, Waldemarson held 948,500 shares in Lifco.

Prosus ( Amsterdam: PRX) was active on both the buy and sell sides this week. The company led a USD 240 million investment in India’s Rapido, the country’s largest and most affordable mobility platform, which operates in more than 400 cities. The deal values Rapido at USD 3 billion. At the same time, Prosus sold a 5% stake in Delivery Hero to Aspex Management for approximately EUR 335 million, at a premium of about 22% to the 30-day average share price. That sale follows an earlier divestiture of a 4.5% stake in Uber in April and stems from commitments Prosus made to the European Commission as part of the approval for the acquisition of Just Eat Takeaway.

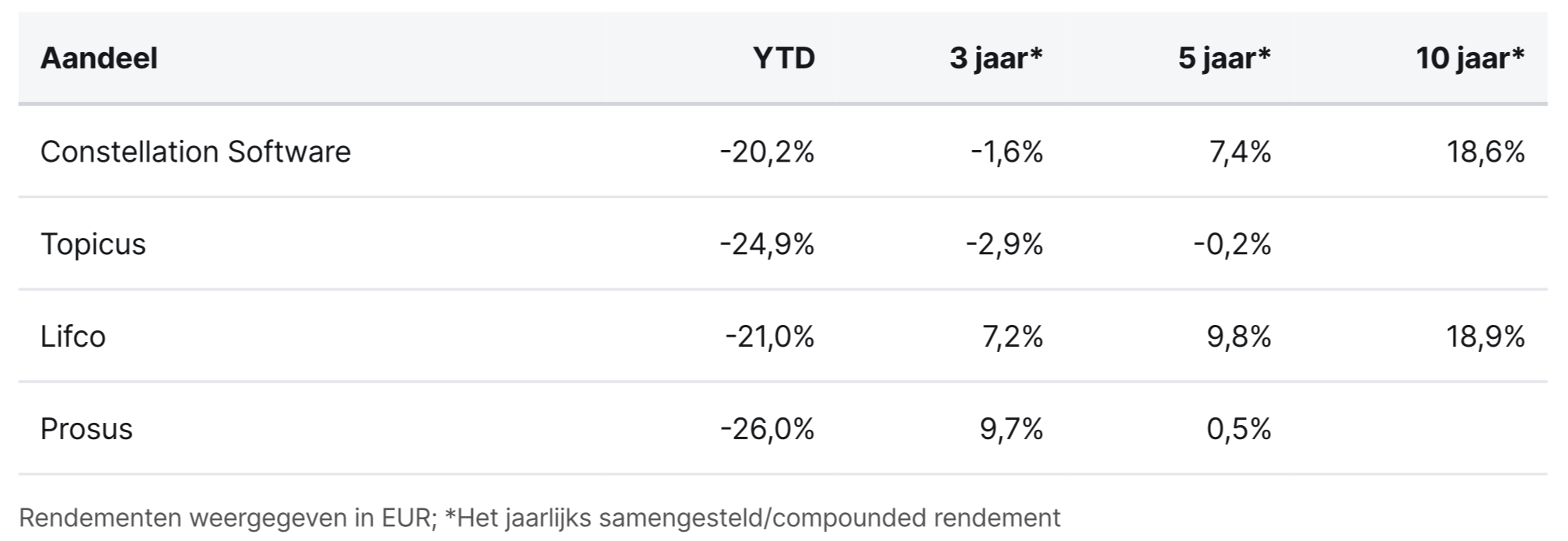

Constellation Software, Topicus, Lifco, and Prosus closed the trading week on the Toronto, Stockholm, and Amsterdam stock exchanges at prices of CAD 2.612.34, CAD 93.93, SEK 279.40, and EUR 39.10 per share, respectively.

KKR posts strong quarterly results despite ongoing concerns about private credit

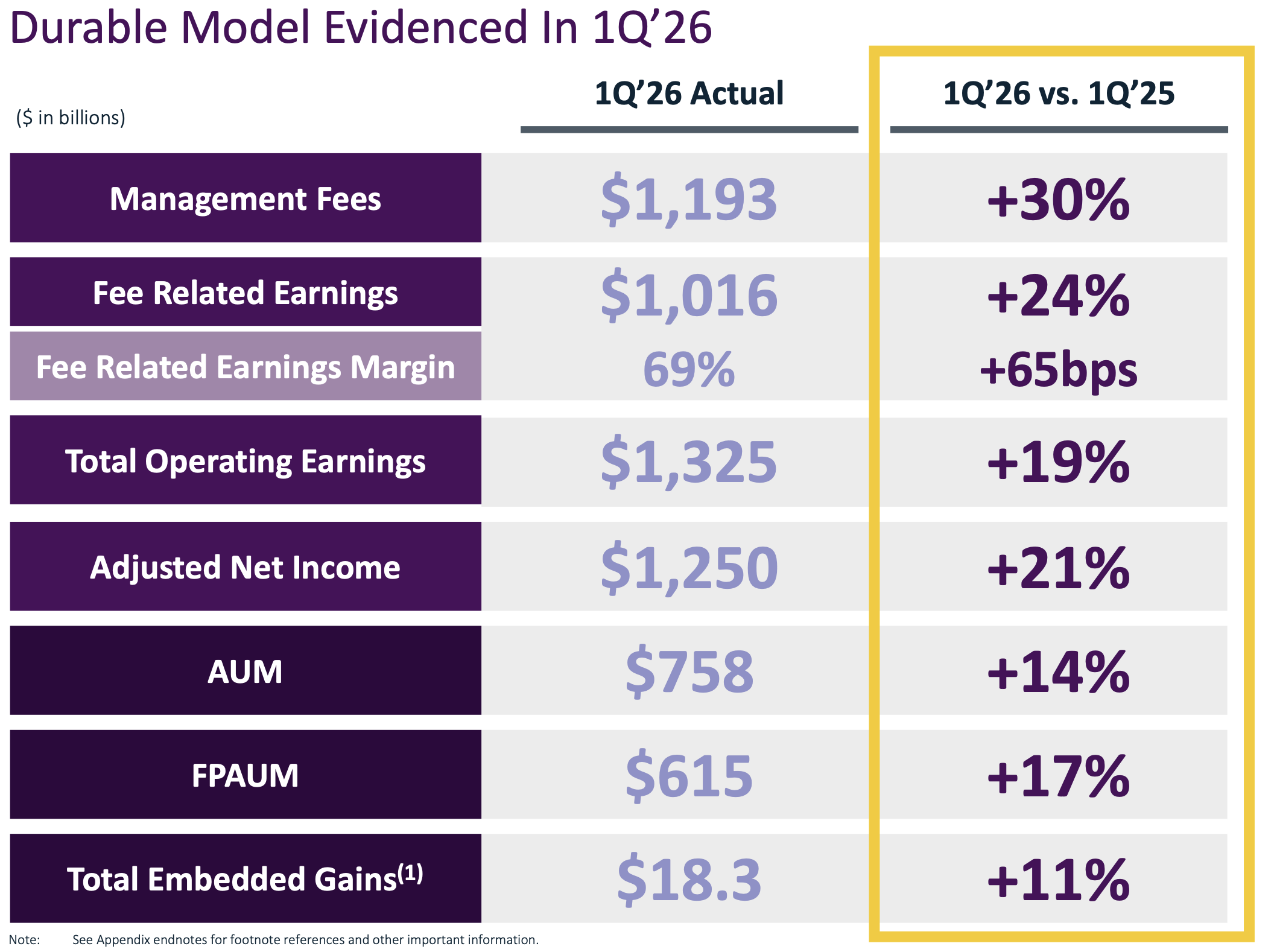

Last week, KKR (New York: KKR) reported its results for the first quarter of 2026, and at first glance, they look excellent. Fee-Related Earnings—the profit the company derives from fixed management fees, and thus the most stable and predictable component of its revenue model—came in at $1.13 per share, a 23% increase compared to last year. Total Operating Earnings of $1.47 per share rose by 18%, and Adjusted Net Income (profit adjusted for one-time items that management focuses on) came in at $1.39 per share, up 20% year-over-year. Each of these figures ranks among the highest KKR has ever reported.

Anyone reading just the headline might think that KKR has the wind fully at its back. And in many ways, that is true. But the reality is more nuanced. A significant portion of the windfall comes from so-called “catch-up fees”—a one-time retroactive fee that fund managers receive when a fund closes, allowing the manager to collect fees retroactively on all capital raised. This quarter, KKR closed its North America XIV fund at $23 billion (the largest vintage ever and larger than the $19 billion of the previous fund) and raised additional capital for Global Infrastructure V. Good news, but it’s important to realize that this type of fee doesn’t recur every quarter. When we remove the catch-up fees from both periods, there is still healthy growth of just over 20% in management fees.

A second nuance lies in Strategic Holdings, a relatively new segment through which KKR participates in its core private equity strategy using its own balance sheet. There, earnings of $48 million fell about 15% short of the consensus estimate. Management did, however, maintain its full-year 2026 forecast of at least $350 million in Strategic Holdings Operating Earnings, with the bulk of that amount expected in the second half of the year.

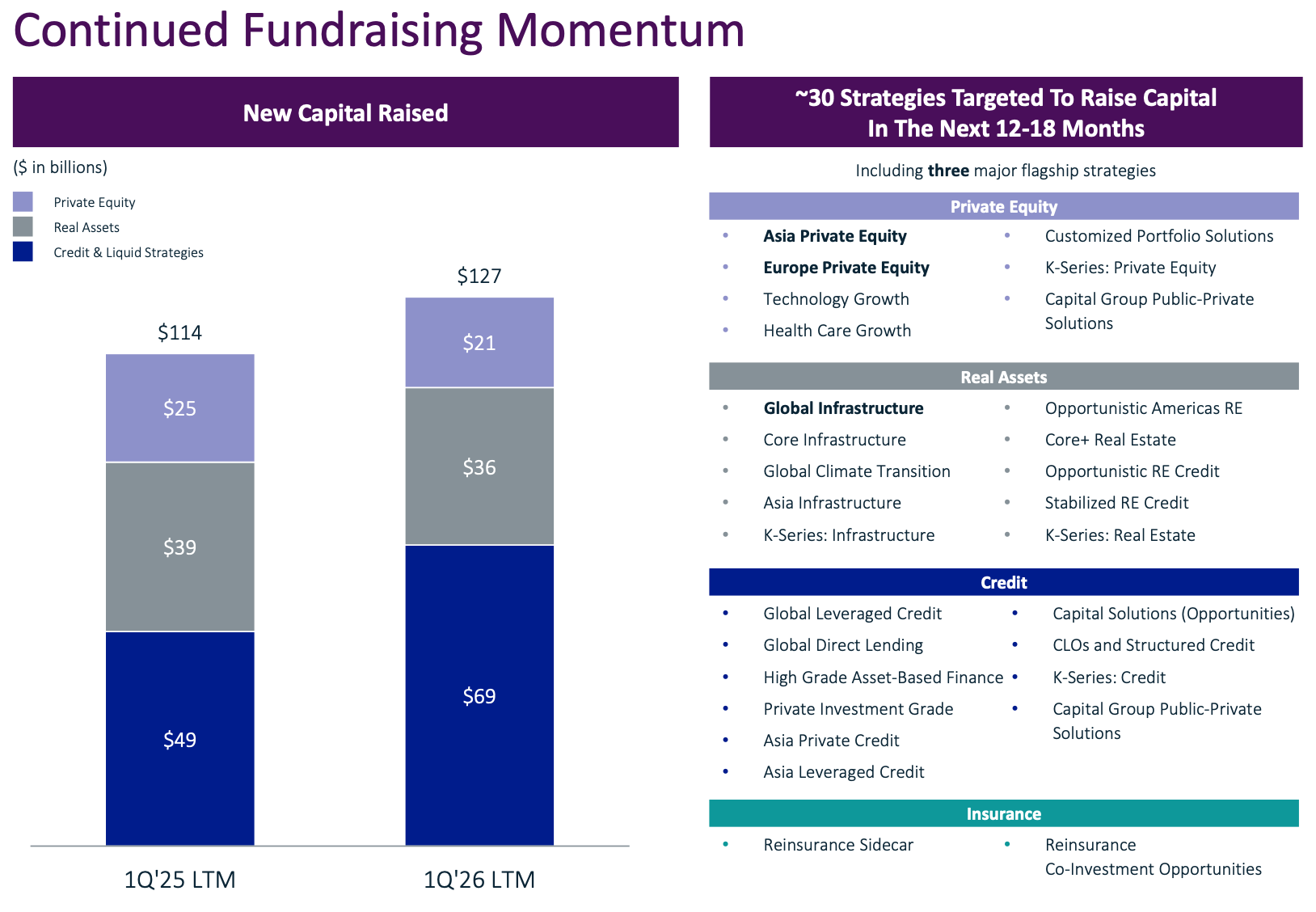

However, a healthy private equity firm isn’t primarily judged by its quarterly earnings, but also by how much new capital it raises (fundraising). KKR raised $28 billion in new capital in the first quarter, comparable to the previous quarter. Over the past twelve months, that amounts to $127 billion, a record, and it shows that the engine continues to run despite the macroeconomic turmoil of recent quarters. The largest contribution this quarter came from Credit & Liquid Strategies with $15 billion, followed by Real Assets with $7.8 billion and Private Equity with $4.7 billion. KKR identifies approximately thirty strategies that will be actively seeking new capital in the market over the next 12 to 18 months. The slide above underscores how broadly diversified fundraising has become; flagship funds accounted for only 15% of the capital raised this quarter, compared to a much higher reliance five years ago.

Co-CEO Scott Nuttall added an interesting observation about what he sees in the market.

"Fundraising is going really well. We have momentum on several fronts, globally, including in the Middle East, as well as among pension funds, sovereign wealth funds, insurers, and high-net-worth clients."

He then pointed to an underlying trend that he believes works in KKR’s favor: institutional investors increasingly want to concentrate their capital with fewer but larger partners. That pattern is becoming even more pronounced right now, as performance within the private markets sector continues to diverge. Nuttall called this a “K-shaped industry”: a reference to the picture of a small group of large, high-performing managers pulling further ahead, while the middle of the pack lags behind. In his words: “We believe that is where the opportunity lies for us to continue gaining market share.”

’s Concerns Despite the positive underlying story, there are two clear downsides about which KKR has been transparent. The first concerns the annual forecast.

Management acknowledged for the first time that the goal of exceeding $7 in adjusted net income per share by 2026—representing year-over-year growth of approximately 45%—has become less likely. CFO Robert Lewin put it this way during the earnings call: “If you were to estimate right now whether we’ll reach $7 per share, we think we’re more likely to fall short of that level.” According to him, the cause lies not with the portfolio itself, but with market timing. In a turbulent macroeconomic climate marked by geopolitical uncertainty, KKR prefers to postpone a number of planned divestments rather than sell a strong portfolio company below market value.

Co-CEO Scott Nuttall summed it up succinctly:"This is about timing, not scale."Deferred monetizations are shifting to 2027 and beyond, so the value isn’t lost—it’s still in the portfolio. Another figure underscores this: total embedded gains (realized but not yet distributed increases in value on the balance sheet and in carried interest) stand at $18.3 billion, 11% higher than a year ago and close to an all-time high.

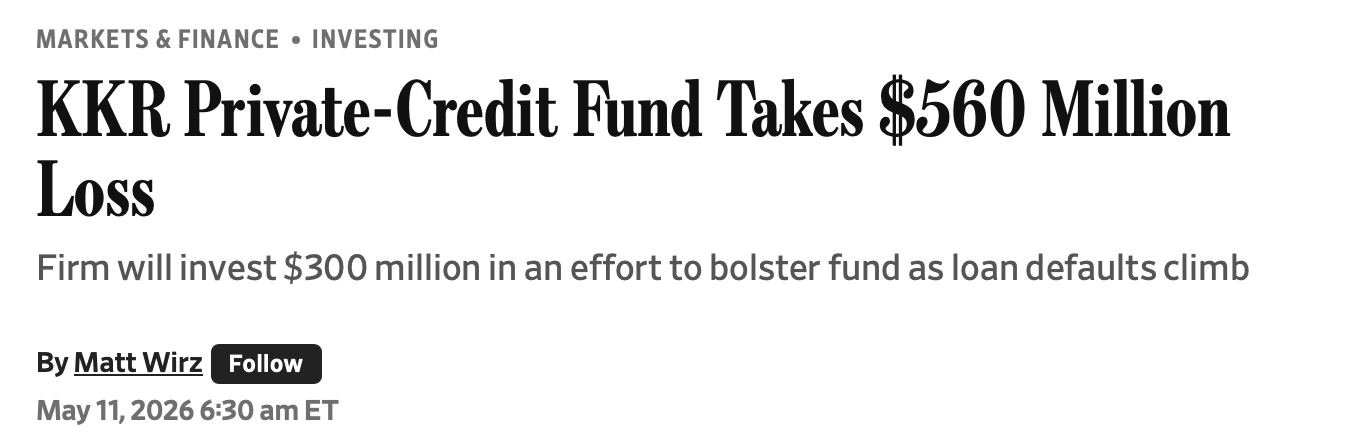

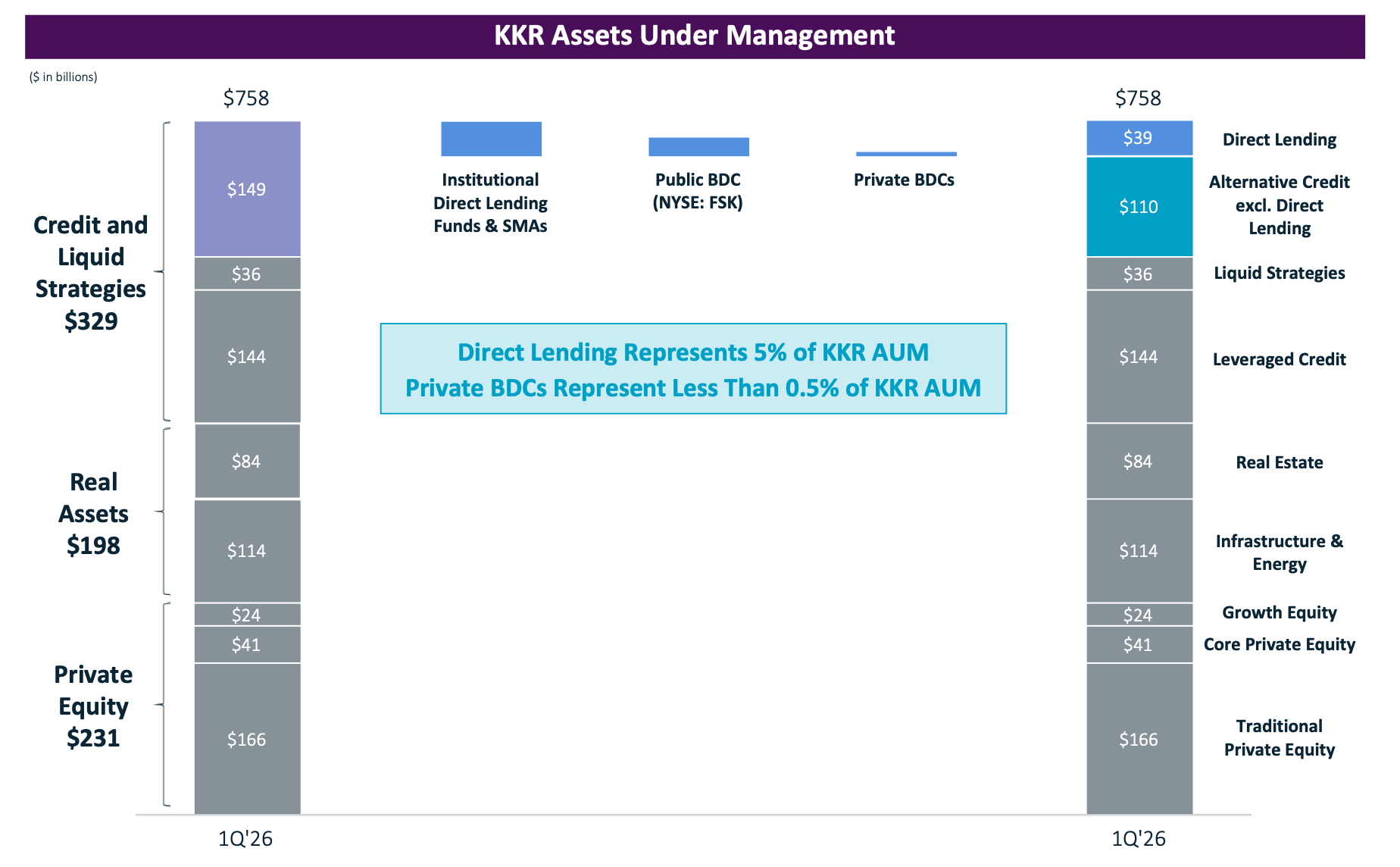

The second concern is more substantive and received widespread media attention last week following an article in the Wall Street Journal. FS KKR Capital, or FSK for short, is KKR’s largest publicly traded Business Development Company (BDC), a vehicle that provides loans to mid-sized U.S. companies and is held primarily by retail investors. In the first quarter, FSK posted a loss of $560 million, approximately 10% of its net asset value. The fund’s default rate (the percentage of loans in default) jumped from 5.5% in December to 8.1% in March. Two rating agencies have since downgraded FSK’s bonds to junk status, and the stock price has nearly halved over the past year.

KKR is digging deep into its pockets with a $150 million package of new convertible preferred shares, a $150 million tender offer for common shares at $11 per share, and the purchase of an additional $300 million in treasury shares by the fund itself. As if that weren’t enough, KKR is also forgoing half of its quarterly bonus fees for the coming year, which amounts to approximately $50 million at current levels.

Behind these generous gestures lies a harsh reality. The loss is real, and the pattern of past problems at FSK continues to repeat itself. Following the earlier write-down on the largest investment, defaults are now occurring at software company Medallia and dental chain Affordable Care. This points to ongoing vulnerability in specific parts of the portfolio, proving that broader concerns about private credit to individuals are by no means unfounded.

However, if you take a step back, the picture looks different. The slide above shows that direct lending accounts for only 5% of the total $758 billion in AUM, private BDCs for less than 0.5%, and FSK itself for just under 2%. The problem, therefore, lies in a small corner of the organization.

A Reuters analysis from last week highlights that recent 13F filings show institutional investors actually increased their exposure to publicly traded private credit funds in Q1. Of the more than 6,000 investors, 11.5% bought more, compared to just 3.2% who sold. Scott Nuttall confirmed that pattern:"Institutional investors are returning to direct lending. They see the headlines about high-net-worth individuals and conclude that the risk-reward ratio on new deals is actually improving."

’s Conclusion Anyone who puts the figures into the proper context can see that KKR has become a highly diversified company. These are objectively strong quarterly results, with one clear area of concern that deserves to be taken seriously, but which must be viewed in perspective. KKR’s main engine—raising capital, investing disciplinedly across all asset classes, and creating value over time for both clients and shareholders—continues to run at full speed.

KKR closed the trading week on the New York Stock Exchange at a price of USD 96.97 per share.

Receive weekly insights in your inbox

Exclusive analyses and updates on family holdings and global market developments.

Tencent is performing strongly, but Prosus could use a lesson in communication

The market reaction to the recent updates from Prosus and Tencent tells a story of two different worlds: that of the holding company, where uncertainty about new investments prevails, and that of its crown jewel, Tencent, which is proving with rock-solid figures that its fundamentals are more stable than ever. Although Prosus consists of 80% Tencent, the remaining 20% caused a significant ripple in the share price this week.

CEO Bloisi’s letter

Let’s start with the letter to shareholders in which CEO Fabricio Bloisi provided the following update:

Although the official annual results will not be released until June, it is already clear that the company has more than met its ambitious targets. With total revenue of $7.3 billion and adjusted e-commerce EBITDA of $1.1 billion (excluding JET and La Centrale). For the first time in the group’s history, all operational e-commerce divisions are profitable, and free cash flow continues to grow steadily, even without Tencent’s contribution.

This all sounds great, but investors were still not satisfied with the update, and the stock closed 7% lower on the Amsterdam Stock Exchange that day. It seems there are two reasons for this: (1) the additional investments that will be needed next year and (2) the way the company communicates.

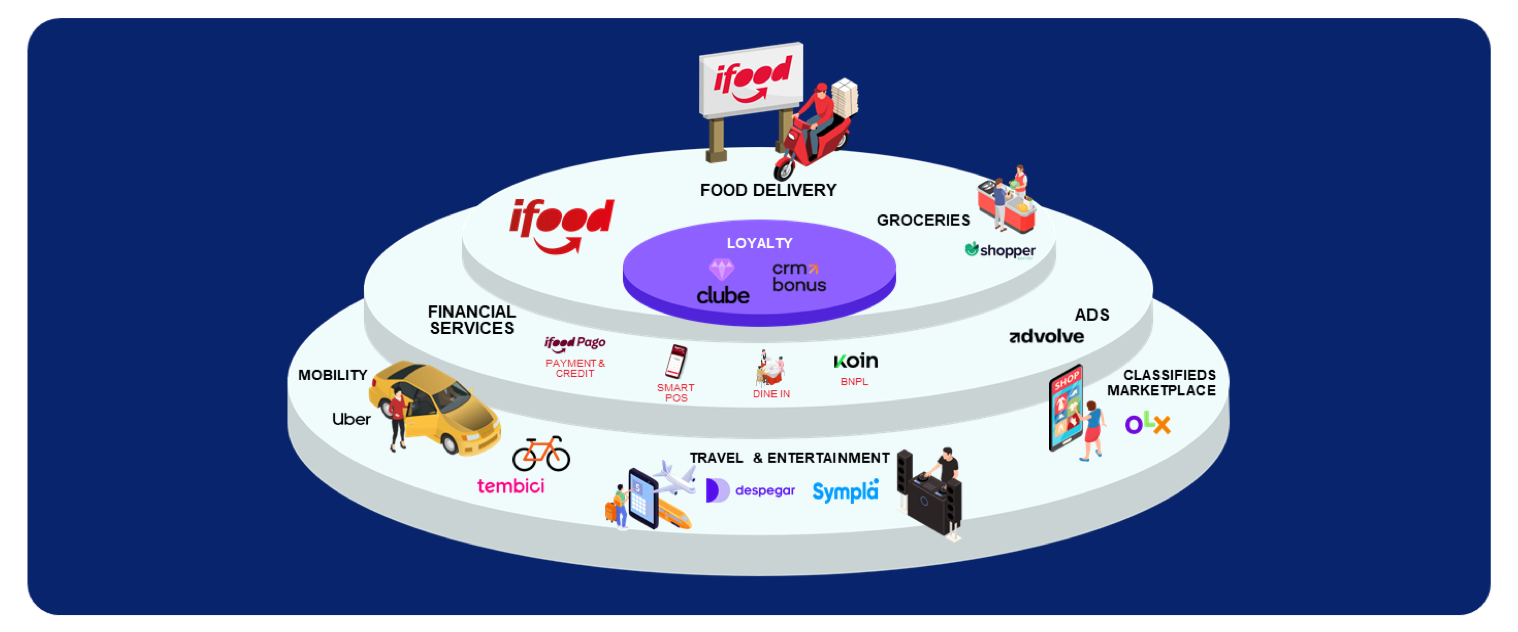

The source of the turmoil lies with iFood, where Prosus has decided to go on the offensive from a position of strength. Although the Brazilian market leader is currently performing strongly, competitors have pledged to spend more than $1.5 billion this year to gain market share. Prosus management believes this level of spending is unsustainable, but at the same time says that this is precisely why it is necessary to invest more itself. A rather unusual way of communicating.

However, this aggressive strategy is having an immediate impact in the short term. The expected adjusted EBITDA for iFood in FY27 has been sharply revised downward to a range of $100 million to $150 million. For investors who hold Prosus primarily as an indirect stake in Tencent (and there are many), this feels like a bitter pill to swallow. These investors would prefer to see every euro available for investment allocated to share buybacks. Nevertheless, investments in AI within Prosus’ ecosystems do appear to be paying off.

A key tool in these investments is the Large Commerce Model (LCM), which has been trained on billions of transactions and is already delivering significant results at iFood. There, conversion rates on notifications rose by 75%, while customer acquisition costs fell significantly and conversion rates on personalized offers increased substantially. This technology is now being scaled up to other markets, including PayU in India and platforms such as OLX, Just Eat Takeaway, and eMAG in Europe. The impact of agent technology is also significant on the operational level; every day, 5,000 AI agents within the company’s own ecosystem complete approximately 4 million tasks per month. According to management, this delivers an efficiency gain equivalent to the impact of more than 1,000 full-time jobs. Initial tests of these applications have already led to a 22% increase in car sales at OLX, a 30% rise in leads at Just Eat Takeaway, and a 32% higher retention rate among restaurants at iFood.

Although one might give management the benefit of the doubt based on its strong innovation figures, investors are taken aback by the way this strategy is being communicated. Prosus argues that the competition’s billion-dollar spending is unsustainable, yet still feels the need to significantly scale up its own investments now. The market interprets this statement not as a deliberate choice made from a position of strength, but rather as a reactive stance: “if the competition is doing it, we have to follow suit.”

In addition, the information provided regarding Just Eat Takeaway (JET), which was acquired last year, was extremely limited and vague. Management reported a 7% decline in the number of orders, but attempted to qualify this by pointing to “selected cities” that grew by 25% following successful experiments. Because concrete details—such as which cities were involved, what their share of total revenue was, and exactly what these experiments entailed—were completely absent, this did not sit well with investors.

Bloisi concludes the letter with:

We believe we are building something special, with results that will compound over many years to create a bright future for Prosus. I am investing alongside you, and so is Prosus. We continue to repurchase shares at an annual run rate of approximately $5 billion, which will bring the total amount returned to you to approximately $50 billion across Prosus and Naspers over the next four years.

Tencent, the Crown Jewel

While the holding company Prosus struggles with its own communications, its crown jewel , Tencent, demonstrates with its first-quarter 2026 results why it remains the group’s undisputed driving force. Tencent was rewarded for a quarter in which its operational strength and the initial successes of its AI transformation became clearly evident.

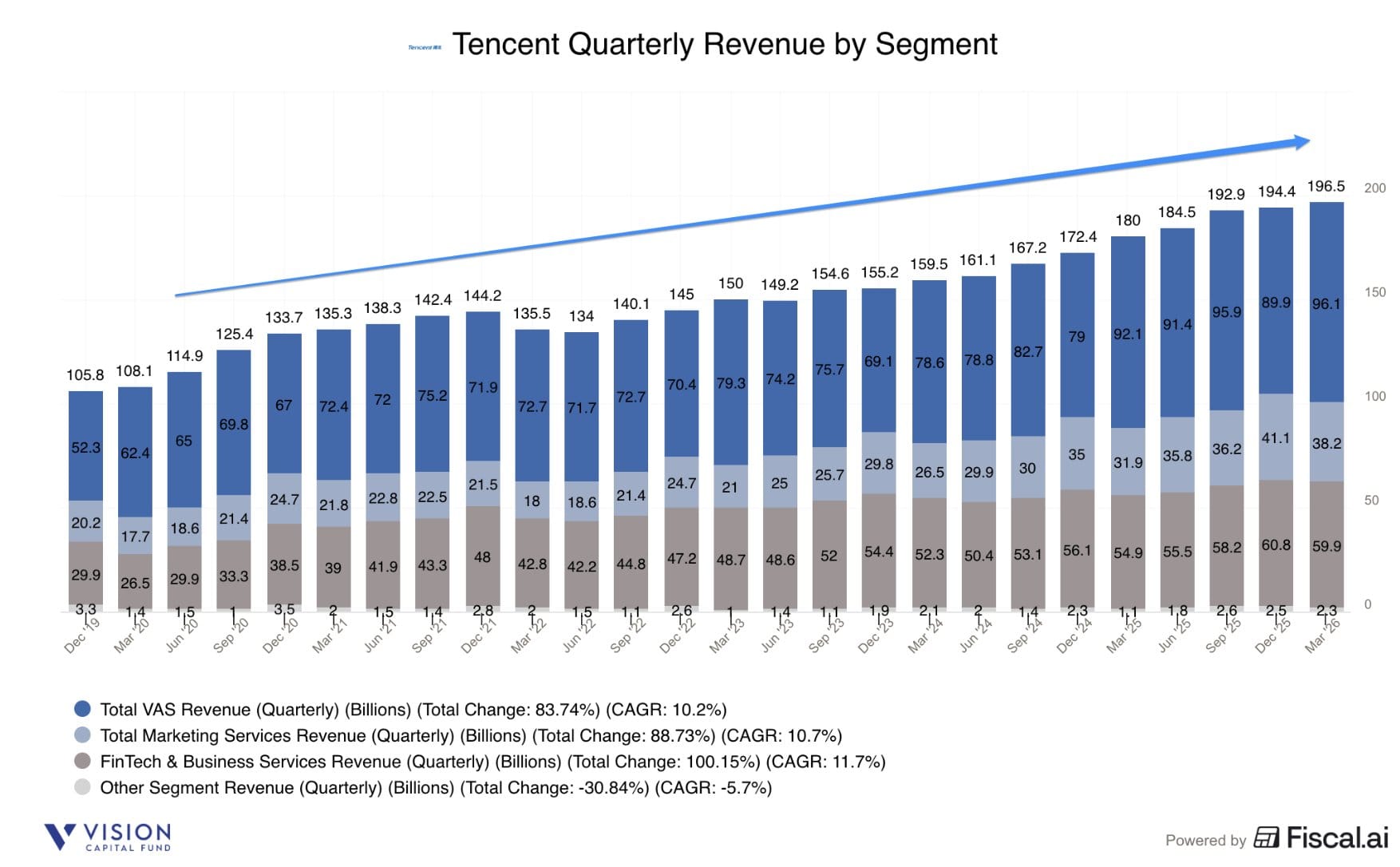

Tencent’s financial fundamentals remain as strong as ever, as is immediately evident from the key figures reported for the first quarter of 2026. Total revenue rose by 9% to RMB 196.5 billion. Although 9% growth may seem modest at first glance, management noted that this figure was impacted by the unfavorable timing of the Chinese New Year. Adjusted for this calendar effect, revenue growth would have been a more solid 11%.

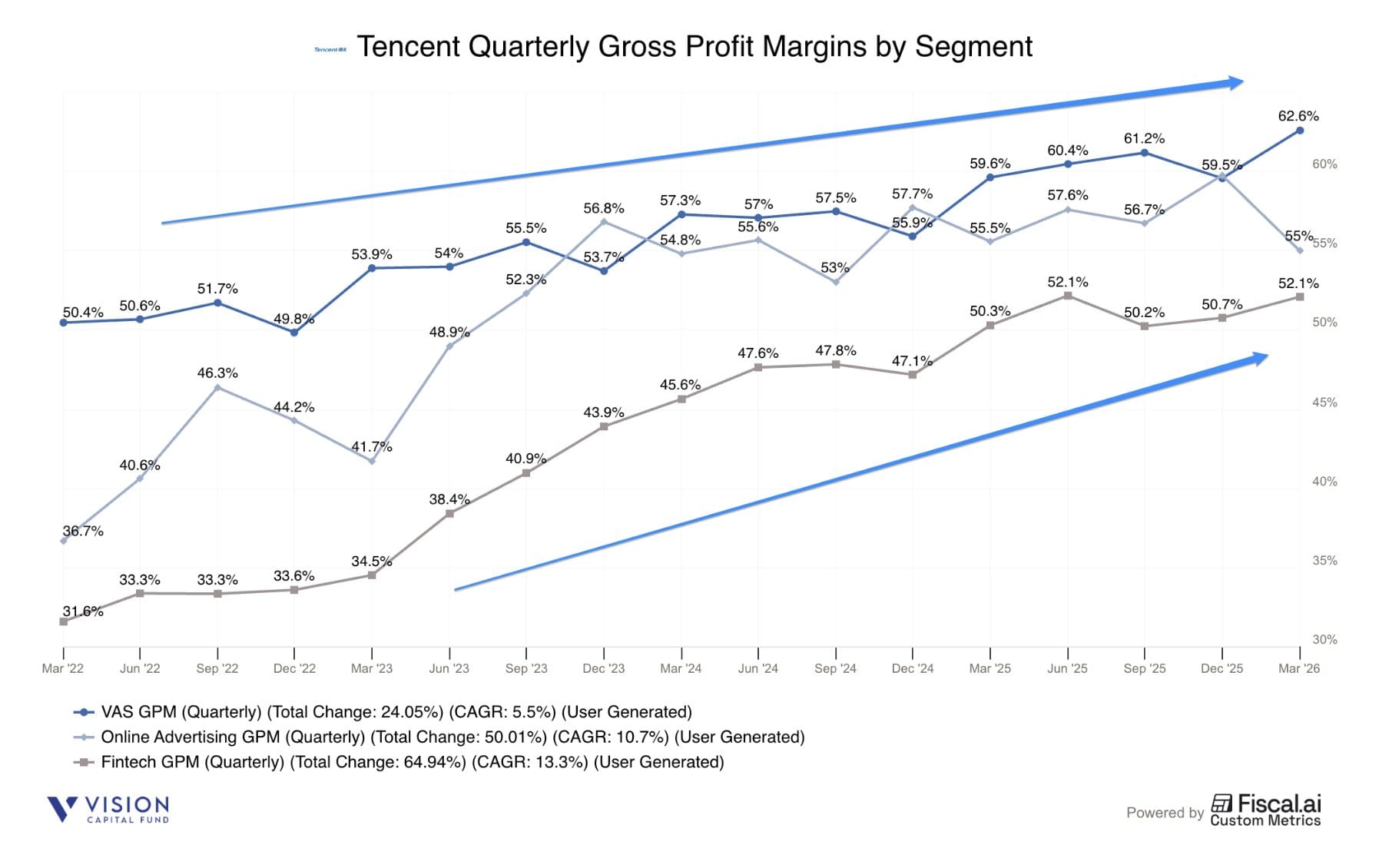

Another notable point was that profitability grew faster than revenue. Gross profit rose by 11% to RMB 111.3 billion, with the gross margin increasing to 56.6%. This operational leverage is clearly visible in net profit (Non-IFRS), which rose by 11% to RMB 67.9 billion. Without the massive investments in new AI products, operating profit would have increased by as much as 17%, underscoring the enormous underlying strength of the core business.

As shown in the charts above, there is a clear upward trend across all major divisions. The segments performed as follows:

- Gaming (VAS):This segment remains the company’s primary growth driver. Revenue from domestic games grew by 6%, while international games rose by 13%. Titles such asPeacekeeper Eliteset records with as many as 90 million daily players at peak times. The gross margin in the broader VAS division rose to 62.5%, partly due to a shift toward internally developed games with higher margins.

- Marketing Services (Advertising):The standout performer, with growth accelerating to 20% (RMB 38.2 billion). This growth is driven by improved AI algorithms for ad recommendations and increasing demand forVideo Accounts. Notably, the "ad load" (the number of ads users see) on these Video Accounts remains extremely low at just 4% to 5% compared to Western competitors like Instagram, indicating enormous untapped potential for future monetization.

- FinTech & Business Services:This segment grew by 9% to RMB 59.9 billion. Although margins here were historically lower, the chart shows a sharp rise toward 52.1%, an increase of 200 basis points compared to last year. Growth here was primarily driven by commercial payments and rising demand for cloud services, including AI-related infrastructure.

With a record free cash flow of RMB 56.7 billion (+20% YoY) and a net cash position of $18. , Tencent has a rock-solid balance sheet. However, this appears not yet to be enough to continue driving both AI investments and the share buyback program. Management previously stated that they would prioritize AI at the expense of a somewhat slower share buyback program, but they are now backtracking on that.

James Mitchell (CSO) emphasized that Tencent is accelerating the sale of liquid positions in its massive investment portfolio, currently valued at between $130 billion and $140 billion. By monetizing these holdings, the company is creating the necessary room to both finance the growing demand for AI infrastructure and continue its aggressive share buyback program. Management views the current share price as “dislocated” (out of line with actual value), which makes share buybacks a priority right now. This is therefore a positive development for Prosus shareholders.

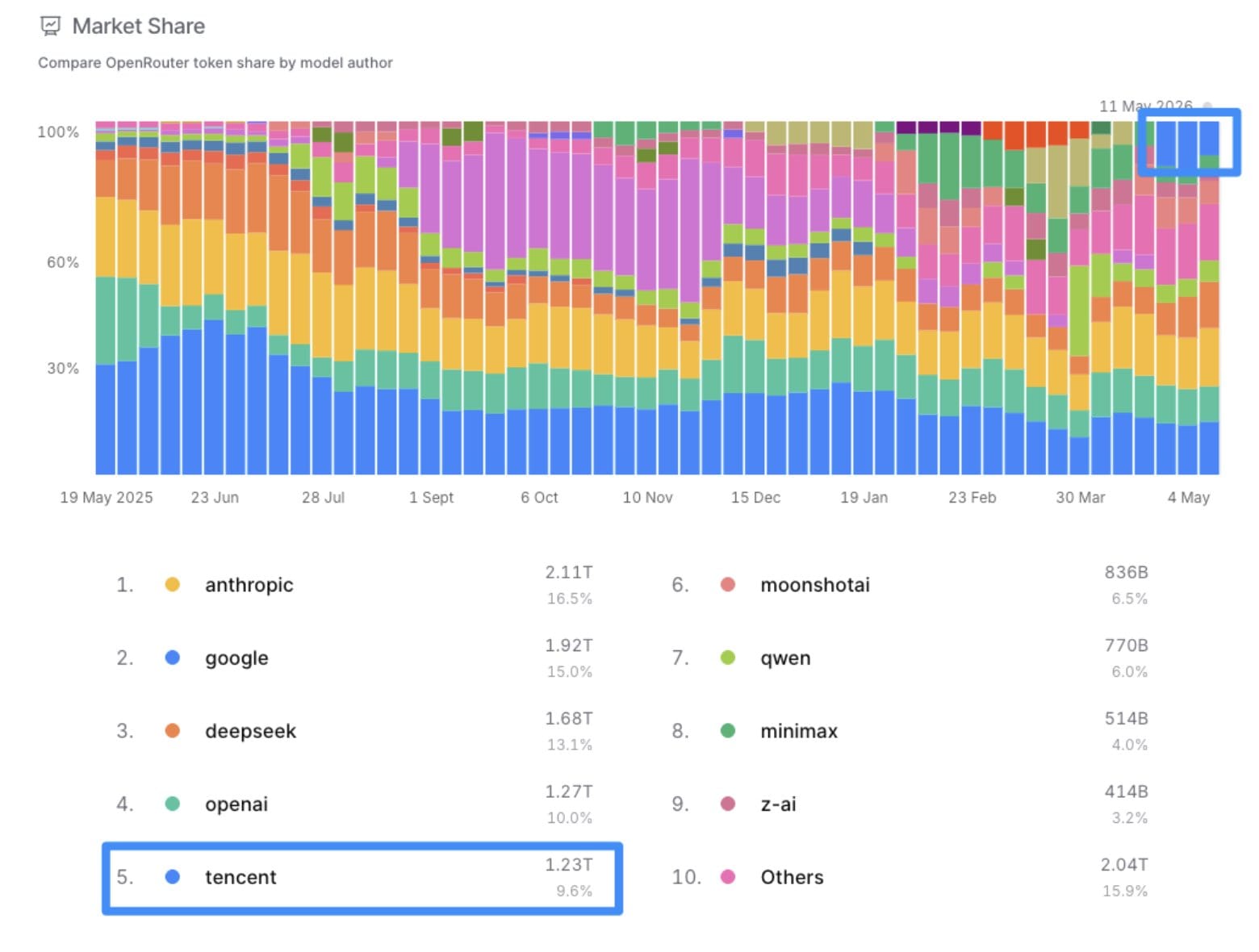

This strategic focus on AI is also beginning to yield tangible results with the introduction of the Hunyuan 3.0 (Hy3) preview. Hunyuan is Tencent’s proprietary “Large Language Model” (LLM), built entirely from the ground up by a revamped team of elite AI researchers. Unlike previous versions, Hy3 is specifically designed for cost-efficiency and practical real-world applicability, with management deliberately shifting the focus from chasing theoretical public benchmarks to superior performance in logical reasoning and coding.

The impact of this is immediately apparent: on the OpenRouter platform, the model has quickly risen to a top position based on token usage, even coming close to established Western models. Within its own ecosystem, the model has now been integrated into 131 internal products, including QQ and Yuanbao, creating a “virtuous feedback loop” in which user data continuously improves the model. In particular, the productivity assistant WorkBuddy has gotten off to a flying start; this AI agent helps users with daily tasks and is now the most widely used business AI service in China based on daily active users.

Prosus closed the trading week on the Amsterdam Stock Exchange at a price of EUR 39.10 per share.

Receive weekly insights in your inbox

Exclusive analyses and updates on family holdings and global market developments.

Sofina Shareholders' Meeting

At the annual shareholders’ meeting of Sofina (Brussels: SOF), CEO Harold Boël painted a picture of a holding company that, after a difficult period from 2022 to 2024, has returned to calmer waters. “In a sense, 2025 was a normal year again,” said Boël, referring to the fact that investments and divestments in previous years had been 40 to 60 percent below the historical average. Last year, the group was once again able to capitalize on a normal number of opportunities and reduce some of its holdings.

Equity per share was estimated at EUR 304.86 as of March 31, 2026, virtually unchanged from the end of December 2025 (-0.30%). This stability is not surprising, as the NAV calculation currently only takes into account exchange rate effects and movements in listed positions, not revaluations of the private portfolio. The figures therefore still reflect the old valuations from Sofina’s private funds. Meanwhile, the share is trading at a discount of more than 30 percent relative to its net asset value, partly due to the weak dollar, which lost about 12 percent against the euro in 2025.

At the shareholders’ meeting, a question was raised about what the venture capital market looks like outside of AI. Boël was clear on this point. A very large portion of current VC investments is focused on AI or AI-related themes. It is the most transformative technology the sector has seen in a long time and requires enormous capital inflows. Beyond AI, life sciences and, to a lesser extent, consumer sectors remain relevant. But what stands out is the renewed interest in energy-related themes. The AI revolution is driving up energy consumption and computing power significantly, making energy a strategic investment theme once again. Sofina is capitalizing on AI through an investment in Xbow, a cybersecurity firm that deploys AI agents as ethical hackers, and through exposure to major companies such as OpenAI, Anthropic, and SpaceX via the fund portfolio.

Finally, after six years, Chairman Dominique Lancksweert handed over the chairmanship to Charlotte Strömberg of Sweden. Lancksweert, who has reached the statutory maximum age, has been a director of the holding company since 1997.

Sofina closed the trading week on the Brussels Stock Exchange at a price of EUR 217.60 per share.

Receive weekly insights in your inbox

Exclusive analyses and updates on family holdings and global market developments.

Would you like more information about our services?

Contact usDisclaimer:

No rights can be derived from this publication. This is a publication by Tresor Capital. Reproduction of this document, or parts thereof, by third parties is only permitted with written permission and with reference to the source, Tresor Capital.

This publication has been compiled with the utmost care by Tresor Capital. The information is intended in a general sense and is not tailored to your individual situation. The information should therefore expressly not be regarded as advice, an offer or a proposal to purchase or trade investment products and/or purchase investment services, nor as investment advice. The authors, Tresor Capital and/or its employees may hold positions in the securities discussed, either for their own account or for their clients.

You should carefully consider the risks before you start investing. The value of your investments may fluctuate. Past performance is no guarantee of future results. You may lose (part of) your investment. Tresor Capital accepts no liability for any inaccuracies or omissions. This information is for indicative purposes only and is subject to change.

Read the full disclaimer at tresorcapitalnieuws.nl/disclaimer .